UBS - Emerging markets_watermark

.pdfvk.com/id446425943

Equities

Stay invested

Emerging market (EM) equities were positive in April, but the abrupt escalation of Sino-US trade tensions has negatively impacted the asset class this month. With the 12-month trailing P/E ratio at 12.3x, valuations look undemanding and offer a 25% discount to developed market (DM) counterparts. At the time of writing, about 50% of EM companies have reported 1Q19 earnings. Overall results have shown improvement, with the weighted average earnings beat standing above 2.5%. However, consensus earnings growth for the full year was downgraded to 4.9. Our baseline scenario calls for a de-escalation of US-China tensions within our tactical six-month investment horizon. De-escalation would eventually bring with it better earnings momentum within emerging markets and more positive data releases. Hence, while uncertainty about trade is likely to weigh on sentiment and growth in the near term, EM equities offer a good upside in our base case given the market is levered to an improving global cycle and its valuation is relatively attractive.

Elections results supportive; keep an eye on idiosyncratic factors

The outcome of recent elections in key emerging countries appears to favor their outlook. In India, Prime Minister Narendra Modi’s BJP and its coalition partners will lead a new government again. In South Africa, the ruling ANC has just won the general election and is set to lead the country beginning with a series of structural reforms. In Indonesia, the official tally confirmed President Joko Widodo’s reelection. Overall, a number of risks to emerging market assets remain in the horizon, including potential new sanctions against Russia, and political uncertainties in several Latin American countries.

Country and sector positioning

In our intra-EM equity strategy, we stay overweight China but have opened a new underweight on Hong Kong in order to hedge downside risks. We upgraded Malaysia to overweight because this defensive market should perform relatively well in an environment of high uncertainty and volatility. We remain underweight Thailand due to its sluggish macro outlook and the residual effect of the general election in March. We find no evident tactical opportunities in EMEA and Latin America at the moment.

At the sector level, within Asia ex-Japan, we like financial and select technology stocks to maximize the diversification benefits between value and growth; we also prefer stocks with sustainable cash flow generation and high dividend yield, which should hold up relatively well during volatile markets. In Mexico, we prefer defensive names with non-Mexican exposure to protect against foreign exchange volatility, slowing domestic growth, and higher political risk (consumer staples, utilities). We also favor interest-rate-sensitive stocks with high dividend yields. In Brazil, we favor high-quality domestic cyclical names (financials, consumer discretionary, industrials) that should benefit from a pickup in economic growth as well as cheap domestic defensives that offer about 5% dividend yield and protection in a potential market correction.

Xingchen Yu |

Gabriela Soni, CFA |

Strategist |

Strategist |

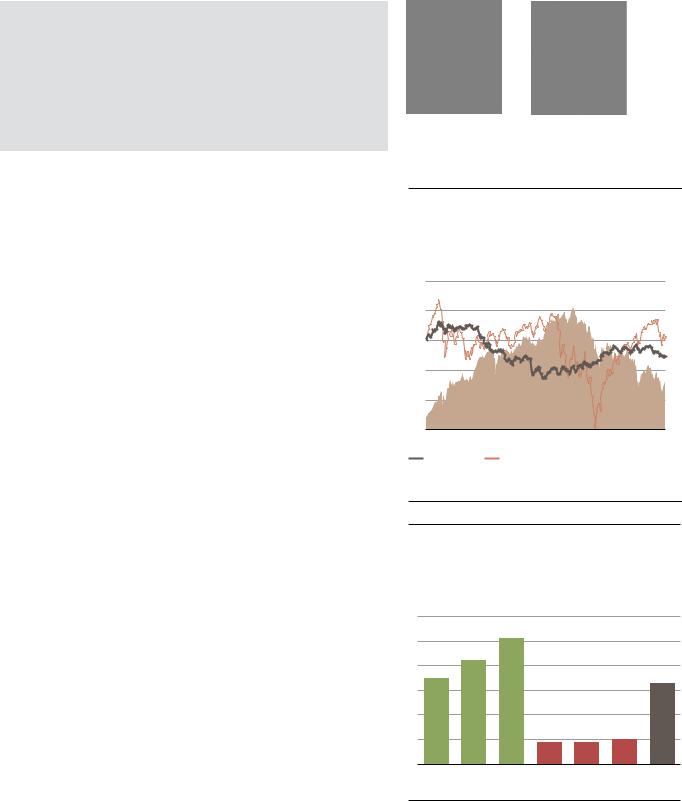

Figure 1

MSCI EM P/E ratio is falling towards its 10 year average

12-month forward P/E ratio

13

12

11

10

May-14 May-15 May-16 May-17 May-18 May-18 May-19

12M forward P/E

10Y Average

Source: Bloomberg, IBES, UBS, as of 21 May 2019

Figure 2

Emerging markets country equity preferences

|

China |

|

|

|

|

|

India |

|

|

|

|

|

|

|

|

|

|

|

Indonesia |

|

|

|

|

Asia |

South Korea |

|

|

|

|

|

Malaysia |

|

|

|

|

|

Philippines |

|

|

|

|

|

Taiwan |

|

|

|

|

|

Thailand |

|

|

|

|

|

Hong Kong* |

|

|

|

|

|

|

|

|

|

|

LatAm |

Brazil |

|

|

|

|

Chile |

|

|

|

|

|

|

|

|

|

|

|

|

Colombia |

|

|

|

|

|

Mexico |

|

|

|

|

|

Peru |

|

|

|

|

|

|

|

|

|

|

|

Czech Republic |

|

|

|

|

EMEA |

Hungary |

|

|

|

|

Poland |

|

|

|

|

|

|

|

|

|

|

|

|

Russia |

|

|

|

|

|

South Africa |

|

|

|

|

|

Turkey |

|

|

|

|

|

|

|

|

|

|

underweight |

neutral |

overweight |

New  Old

Old

*Hong Kong is not a constituent of MSCI EM. Note: All positions are relative to MSCI EM. Source: UBS CIO, as of May 2019.

UBS CIO GWM June 2019 11

vk.com/id446425943

USD bonds strategy

Trade war back in focus

The rally in emerging market (EM) USD-denominated bonds has shown signs of abating amid escalating US-China trade tensions. The asset class (JP Morgan EMBIG Diversified and CEMBI Diversified indexes) has posted a cumulative return of 6.5-7.5% year-to-date, but returns have been broadly flat since early April. Overall, declining US Treasury yields have helped mitigate the impact of widening credit spreads. That said, the high yield segment underperformed its investment grade peer, particularly in countries facing idiosyncratic issues such as Venezuela, Argentina, Sri Lanka, Lebanon, and Turkey. This reflects deterioration in global investor sentiment. Outperformers are lower-beta oil exporters outside of the Middle East (e.g., Kazakhstan, Malaysia), as well as Central Eastern Europe, which is seen as a relatively safe place.

Escalating trade tensions

US-China trade talks have taken a negative turn. The US raised tariffs on USD 200bn of Chinese imports. In return, China increased tariffs of up to 25% on USD 60bn of US imports, and accused the US of “unilateralism and trade protectionism.” Also, US officials said preparations were being made to apply new tariffs on the remaining USD 325bn of Chinese imports not yet covered by levies.

We continue to believe that a shared desire to avoid a global slowdown will eventually push the US and China toward a compromise. As of now, it seems likely that Presidents Donald Trump and Xi Jinping will meet at the next G20 summit in late June. Uncertainty has increased, however, and new tariffs may delay the recovery in global growth. More stimulus out of China and potentially a more dovish Federal Reserve are mitigating factors, but they may not fully offset the impact on growth of a full-blown trade war.

Credit views

Our base case remains for a recovery in global growth in the second half of the year, conditional to a de-escalation in trade tensions. Despite our more cautious view on EM credit, we expect credit spreads to remain range-bound over the next six months, implying 1–2% total returns. Trade uncertainties will keep volatility elevated, but the external backdrop for the asset class remains fairly supportive thanks to accommodative global central banks, higher commodity prices, very low default rates in EM high yield corporate credit (0.3% as of April), decent valuations, and favorable technicals. Against this backdrop, we keep a slight risk-on but selective stance in our allocation together with a short position on duration after the rally in US Treasuries.

What are we looking for next?

Key to monitor in the coming weeks are developments related to trade talks, particularly: whether trade negotiations continue or break down completely; how swiftly the US follows through on the president’s threat to impose duties on an additional USD 325bn of Chinese goods; whether China retaliates beyond the tariffs announced on 13 May; whether the US goes on to raise tariffs on auto imports; the monetary and fiscal policy response; and the spillover, if any, for global economic growth.

Jérôme Audran, |

Michael Bolliger |

CFA, FRM, Analyst |

Head of EM Asset |

|

Allocation |

UBS CIO GWM June 2019 12

vk.com/id446425943

Currencies

Collect carry in a measured way

US-China tensions over trade and technology hit global risk sentiment and affected emerging market currencies, though losses have been moderate so far. A sustainable uptick in emerging economies now looks likely to be delayed as we await more clarity on trade and potential policy responses. For now, our neutral outlook for global monetary policy benefits emerging market currencies, and we expect them to continue to trade broadly sideways. We think current and expected conditions for the coming quarters favor a selective exposure to high-yielding emerging market currencies.

After trending broadly sideways for most of the year, emerging market currencies have felt the weight of the escalating trade tensions between the US and China since the beginning of May and weakened moderately. We expect a trade deal, or at least a truce, at some point later this year, which should then limit the trade-related depreciation pressure on emerging market currencies. Until an agreement is reached, renewed spikes in market volatility are likely and these currencies may suffer temporarily.

Until the US-China tensions escalated, conditions for emerging markets were stabilizing. The neutral outlook for the Federal Reserve’s monetary policy (as well as other global central banks’) provided a more favorable backdrop compared to last year. And after a weak first quarter, emerging economies were showing signs of a growth turnaround. For their currencies to appreciate sustainably, their domestic growth outlook should improve. This will likely be delayed now as uncertainty reigns again.

In this situation of an expected benign global monetary policy backdrop, moderate but stable growth, and somewhat weaker emerging market currencies, we have added to our FX strategy a new diversified position consisting of a long basket of select high-yielding emerging market currencies (Indonesian rupiah, Indian rupee, South African rand), funded with low-yield- ing, high-beta currencies (Australian, New Zealand, and Taiwan dollar) to lower the sensitivity to global headwinds, in particular trade tensions. Please see “Opportunities in a low-volatility FX land,” published 23 May, for details.

This new position incorporates the favorable view we have had on the South African rand since April. We continue to expect President Cyril Ramaphosa to move the focus back on structural reforms after May’s general election, which should support the rand in the coming months, assuming manageable global headwinds.

Aside from the always-present idiosyncratic risks around domestic politics and policies, emerging market currencies will remain exposed to global growth and trade dynamics, benchmark yields, geopolitics, and oil prices, as well as related investor sentiment.

Tilmann Kolb, CFA |

Jonas David, CFA |

Analyst Analyst

Figure 1

EM currencies only reacted moderately to additional trade tensions so far

ELMI+ and MSCI World, indexed to 100 on 1 January 2018 (lhs); 2-year US Treasury yield, in % (rhs)

110 |

|

|

|

|

3.2 |

105 |

|

|

|

|

3.0 |

|

|

|

|

|

|

|

|

|

|

|

2.8 |

100 |

|

|

|

|

2.6 |

|

|

|

|

|

|

95 |

|

|

|

|

2.4 |

|

|

|

|

|

|

|

|

|

|

|

2.2 |

90 |

|

|

|

|

2.0 |

|

|

|

|

|

|

85 |

|

|

|

|

1.8 |

Jan-18 |

Apr-18 |

Jul-18 |

Oct-18 |

Jan-19 |

Apr-19 |

ELMI+ |

|

MSCI World |

|

|

|

UST 2yr (rhs)

UST 2yr (rhs)

Source: Bloomberg, UBS, as of 23 May 2019.

Figure 2

Choosing long and short currencies wisely unlocks carry with diminished risks

Interest rate carry for basket currencies over a six-month horizon, in %

6 |

|

|

|

|

|

|

5 |

|

|

|

|

|

|

4 |

|

|

|

|

|

|

3 |

|

|

|

|

|

|

2 |

|

|

|

|

|

|

1 |

|

|

|

|

|

|

0 |

|

|

|

|

|

|

ZAR |

INR |

IDR |

AUD |

NZD |

TWD |

Basket |

Source: Bloomberg, UBS, as of 23 May 2019. |

|

|

carry return |

|||

|

|

|

||||

UBS CIO GWM June 2019 13

14 2019 June GWM CIO UBS

What’s at stake? |

Economic & policy backdrop |

Candidates & key trends |

Scenarios & implications |

Throughout 2019, voters will elect the president, half of the representatives in the lower house, one-third of the senate, governors of 22 out of the country's 23 provinces, and the mayor of the City of Buenos Aires. Markets will focus on the outlook for the October presidential race.

Date |

Election type |

Province / |

|

National |

|||

|

|

||

2-Jun-19 |

Gubernatorial - General |

San Juan |

|

|

|

|

|

|

Gubernatorial - General |

Misiones |

|

|

|

|

|

9-Jun-19 |

Gubernatorial - General |

Entre Ríos |

|

|

|

|

|

|

Gubernatorial - General |

Tucumán |

|

|

|

|

|

|

Gubernatorial - General |

Chubut |

|

|

|

|

|

|

Gubernatorial - General |

Jujuy |

|

12-Jun-19 |

Deadline - Electoral |

National |

|

|

alliances |

|||

|

|

|

||

|

|

|

|

|

|

16-Jun-19 |

Gubernatorial - General |

Santa Fe |

|

|

|

|

|

|

|

|

Gubernatorial - General |

San Luis |

|

|

|

|

|

|

|

|

Gubernatorial - General |

Formosa |

|

|

|

|

|

|

|

|

Gubernatorial - General |

Tierra del Fuego |

|

|

|

|

|

|

|

22-Jun-19 |

Deadline - Presidential |

National |

|

Argentina |

candidates |

|||

|

|

|||

|

|

|

||

11-Aug-19 |

Presidential - Primary |

National |

||

|

|

|

|

|

|

|

Legislative - Primary |

National |

|

|

|

|

|

|

|

29-Sep-19 |

Gubernatorial - General |

Mendoza |

|

|

|

|

|

|

|

13-Oct-19 |

First debate |

National |

|

|

|

|

|

|

|

20-Oct-19 |

Second debate |

National |

|

|

|

|

|

|

|

27-Oct-19 |

Presidential - General |

National |

|

|

|

|

|

|

|

|

Legislative - General |

National |

|

|

|

|

|

|

|

|

Gubernatorial - General |

Buenos Aires |

|

|

|

|

|

|

|

|

Gubernatorial - General |

Catamarca |

|

|

|

|

|

|

|

|

Gubernatorial - General |

Santa Cruz |

|

|

|

|

|

|

|

|

Gubernatorial - General |

Caba |

|

|

|

|

|

|

|

10-Nov-19 |

Gubernatorial - General |

Salta |

|

|

|

|

|

|

|

24-Nov-19 |

Presidential - Runoff |

National |

|

|

|

|

|

|

|

TBD |

Gubernatorial - General |

Chaco |

|

|

|

|

|

|

|

TBD |

Gubernatorial - General |

La Rioja |

|

|

|

|

|

|

|

|

C. Kirchner's corruption |

|

Ongoing |

trials |

|

|

2.8 |

1.8 |

|

GDP |

|

|

|

-2.3 |

-2.0 |

||

(y/y in %) |

|||

|

|

|

|

47 |

|

|

25 |

27 |

18 |

Inflation |

|

|

|

|

|

|

|

(year end in %) |

|

|

|

|

|

|

|

Current account |

|

|

-1.7 |

-2.2 |

(% of GDP) |

-4.9 |

-4.0 |

||

|

|

|

||

Budget balance |

|

|

-3.1 |

-2.2 |

|

-5.6 |

|

||

(% of GDP) |

-6.1 |

|

|

|

|

'17 |

'18E |

'19E |

'20E |

Recent adjustments to the foreign-exchange intervention program have brought down currency volatility. We think the country's strict money base targets and foreign-exchange bands will eventually lead to better behaved inflation. Fiscally, the government delivered its target primary deficit of 2.7% of GDP in 2018, and aims to achieve additional savings in 2019. We believe it will gradually approach, but remain short of, a primary fiscal balance this year. Amid tight monetary and fiscal policy, economic activity will remain muted. The primary sector is one that will likely support overall activity as production stages a meaningful recovery from the depressed levels of 2018 due to drought conditions.

Mauricio Macri: Current president and member of Cambiemos party. His voter support levels have been suffering since the mid-2018 currency crisis, but seem to be bottoming out.

Maria Eugenia Vidal: Current governor of the Province of Buenos Aires. Were Macri’s polling numbers to worsen, she might step in as presidential candidate as she is among the most popular politicians in the country.

Macri's numbers would have to worsen materially from current levels for this to happen, though.

Cristina Fernandez de Kirchner: Former president and current senator for Buenos Aires Province. Despite widespread corruption allegations against her, she retains around 30% of voting intentions. She announced in May that she will participate in the August primary elections, running as vice president to presidential candidate Alberto Fernandez.

Alberto Fernandez: A political negotiator, his only election experience was in 2000 when he ran for the local congress of the city of Buenos Aires. His ticket lost and he came in second, though he still secured a legislature seat. Fernandez was chief-of-staff for Nestor Kirchner and Cristina Kirchner. He quit the role over disagreements with Cristina Kirchner. He was a critic of her second mandate, particularly relating to her more extreme policies. Fernandez maintains good relations with many Peronist leaders and segments of the private sector and the media. He led Massa’s presidential campaign in 2015.

Peronist candidates not aligned with Cristina Kirchner. Roberto Lavagna, former economy minister under Duhalde’s administration; Juan Manuel Urtubery, current governor of Salta Province; Miguel Ángel Pichetto, senator for Río Negro province and leader of the Senate majority; Juan Schiaretti, governor of Córdoba. Despite clear differences among them, they all represent macroeconomic policy continuity.

Sergio Massa: Former chief-of-staff of Cristina Kirchner, former presidential candidate, and current congressman for Buenos Aires Province. He ran in the 2015 presidential race and came in third with 23% of the votes. He is ideologically ambiguous. We think he is closer in thinking to Kirchner than to the non-Kirchnerist Peronist candidates.

With five months to go, the presidential race remains wide open. In our baseline scenario, however, we expect a number of the policies of incumbent President Mauricio Macri to remain in place under his successor, and of course if he is reelected. These include fiscal consolidation efforts toward a primary surplus, tight monetary policy to rein in inflation, and a cooperative relationship with the IMF, as well as "willingness" to remain current on debt obligations.

Kirchner's ticket does not represent continuity, in our view. We see her odds of winning arouond 35% given that she is facing severe corruption allegations; Argentine economic numbers are set to look less dire in the coming months; the global macro and political backdrop is supportive, with key partners the US, Brazil, and Chile all backing policy continuity; and the fact that incumbent presidents in Latin America have historically had a distinct advantage in winning reelections.

In our view, current Argentine asset prices overestimate the likelihood of a return to populism in the upcoming elections. We maintain our favorable view of a number of Argentine US dollar-denominated bonds, though we warn against making too large of an allocation to the country. Our favorable view on its electoral outlook is far from guaranteed, and Argentina's still-large twin deficits leave its assets vulnerable to sharp changes in the external financial environment in the near term. Longer term, the country will continue to face economic and political challenges.

Libertarian economists: A number of libertarian economists intend to run, with Jose Luis Espert leading the pack. They enjoy limited voter support currently.

Google search trends

100%

80%

60%

40%

20%

0% |

|

|

|

|

|

|

|

|

|

|

|

|

|

Apr-2018 |

Jul-2018 |

Oct-2018 |

Jan-2019 |

Apr-2019 |

||

Mauricio Macri |

Cristina Kirchner |

Alberto Fernandez |

||||

María Eugenia Vidal |

Sergio Massa |

|

|

|

||

Polling trends:

A note on published polls: The majority of survey results published in the local press and influencing the market lately are of questionable quality. Most are based on landline phone interviews, often carried out by robots. In-person surveys are generally considered more trustworthy, but they are costly to execute, and the few agencies running them don’t usually make the results publicly available, selling them privately instead. The small print is key to assessing the believability of the surveys.

Social media following |

|

||

|

|||

|

likes |

followers |

|

|

|

|

|

Mauricio Macri |

4.4m |

4.8m |

|

Cristina Fernandez |

2.4m |

5.4m |

|

de Kirchner |

|||

|

|

||

Alberto Fernandez |

23k |

145k |

|

María Eugenia Vidal |

1.6m |

1.5m |

|

Sergio Massa |

951k |

1m |

|

Roberto Lavagna |

5.5k |

148k |

|

|

|

|

|

Source: Ministerio del Interior, Obras Publicas y Vivienda, La Nacion, UBS, as of May 2019

market Emerging |

com/id446425943.vk |

monitor electoral |

|

What’s at stake? |

Economic & policy backdrop |

Candidates & key trends |

Scenarios & implications |

October/November – Parliamentary elections |

|

4.9 |

5.1 |

4.4 |

3.8 |

460 members of the Sejm (lower house) and 100 members |

|

|

|||

|

|

|

|

||

|

|

|

|

|

|

of the Senate (upper house); proportional representation |

GDP |

|

|

|

|

with 5% single party threshold (Sejm) |

(y/y in %) |

|

|

|

|

|

Inflation |

2.1 |

1.1 |

2.3 |

2.6 |

|

|

|

|

(year end in %)

Sejm current composition:

Poland

Senate current composition:

Current account |

0.1 |

|

|

|

(% of GDP) |

|

|

|

|

|

|

-0.7 |

-1.0 |

-1.3 |

Budget balance |

|

-0.4 |

|

|

(% of GDP) |

|

|

|

|

|

-1.5 |

|

-1.6 |

-1.6 |

|

'17 |

'18E |

'19E |

'20E |

Poland benefited from an impressive growth spurt in recent years, allowing the government to boost fiscal spending while keeping the budget deficit contained. GDP growth should remain sound (2019: 4.4% y/y), thanks to solid private consumption; fiscal easing later this year supports this view. Still, high-frequency economic data remains mixed, and additional Eurozone weakness would muddy the Polish outlook as well. Risks persist also with regards to global trade and European politics.

Law and Justice (PiS): PiS is the main nationalistconservative party in Poland. It won an absolute majority in 2015, and incumbent Prime Minister Mateusz Morawiecki leads the party into this year's election. Its fiscal spending programs over the past years were well received by large parts of the Polish population.

Civic Platform (PO): PO is the main opposition party, headed by Grzegorz Schetyna. Given its liberalconservative focus, it is perceived as more businessoriented than PiS. PO has a pro-European focus; the current president of the European Council, Donald Tusk, is a cofounder of PO and served as prime minister of the earlier PO-led government.

Wiosna: Formed only in early 2019 by Robert Biedroń, the social-democratic Wiosna already comes in third place in polls for the parliamentary election. Its platform is based on increases in social spending, better environmental protection, as well as pro-European and socially liberal values.

Kukiz'15: The right-wing political movement, led by Paweł Kukiz, received more than 8% in the last general election, but saw some members of parliament switch to other political groupings over the past years. It enjoys strong support from the younger populations.

Polling trends (below):

Law and Justice consistently polls as the strongest party, with Civic Platform in the second place. A number of parties do not currently surpass the electoral threshold of 5%, which may decide over Law and Justice’s ability to reach an absolute majority on its own. The performance of the European Coalition in the European Parliament election may offer an indication of the viability of collaboration between Polish opposition parties.

Base case:

We think the ruling Law and Justice is likely to remain in power. Another outright majority is in the realm of possibility if smaller parties fail to cross the electoral threshold. Polls show a PiS vote share of slightly below 40%, but with roughly five months to the election, these are still early indications. Strong economic growth, low unemployment, and past and planned social spending provide a supportive backdrop for campaigning.

A potential weakness may be the government’s ongoing disputes with the European Commission around the rule of law and judicial reform, especially if the opposition can link these disputes with Poland’s standing in the EU. The Polish population is highly supportive of EU membership, also given its large economic benefits in the form of EU structural funds.

In the case of another PiS (or PiS-led) government, we don’t expect a change in the current policy direction. Catering to the party’s base in terms social and socially conservative fiscal priorities will likely persist, as will clashes with European institutions over the rule of law. Over a multiyear horizon, the new government may have to find a way to finance fiscally expansive measures amid moderating economic growth.

Alternative scenarios:

We think it is unlikely that any of the opposition parties can overpower PiS and become the strongest force in the Sejm. However, the formation of a coalition for the European Parliament elections by several opposition parties may serve as a blueprint for the Polish parliamentary election. Should the main parties cooperate, the election may become quite contested. From a market perspective, a change in power may be greeted with some enthusiasm, as the deterioration in institutional quality will come to an end. However, different views and ideologies within the coalition may also lead to frictions.

market Emerging |

com/id446425943.vk |

monitor electoral |

|

15 2019 June GWM CIO UBS

Google search trends |

Polling trends |

Social media following |

|

||

|

|

|

|

||

|

|

|

|

likes |

followers |

|

|

|

|

|

|

|

|

|

Mateusz |

- |

112k |

|

|

|

Morawiecki |

||

|

|

|

|

|

|

|

|

|

GrzegorzSchetyna |

36k |

183k |

|

|

|

RobertBiedroń |

530k |

171k |

|

|

|

|

|

|

Source: Sejm (sejm.gov.pl), Wikipedia, Google, UBS, as of May 2019

vk.com/id446425943

Emerging markets publications

Investing in emerging markets

A monthly guide to investing in emerging market financial assets |

29 May 2019 – 4:00 pm GMT |

June 2019 |

Chief Investment Office GWM |

|

Investment Research |

Tweet quakes and their aftershocks

Equities: |

Credit: |

Currencies: |

Focus: |

Economy: |

Stay invested but |

Trade war back in |

Collect carry in a |

Argentina: |

The economics of |

use caution |

focus |

measured way |

Political waters |

US-China trade |

|

|

|

stirred by |

tensions |

|

|

|

Kirchner's |

|

|

|

|

announcement |

|

This report has been prepared by UBS AG, UBS Financial Services Inc. (UBS FS), and UBS Switzerland AG.

Please see important disclaimers and disclosures that begin on page 20.

Monthly flagship

Investing in emerging markets

Including investment views across asset classes and regions

10 October 2018

Chief Investment Office GWM

Investment Research

Thinking strategically about Emerging Markets

Economic, social and financial market changes over the last 20 years and investment implications

A previous version of this report displayed an incorrect version of the table in Figure 42.

White Papers

Thinking strategically about Emerging Markets

Africa

Cradle of Diversity

Russia

Back at Global Center Stage

Latin America

Beyond peak trade

Middle East

Prosperity beyond oil

Asset class publications |

Regional investment themes |

Currencies |

Long term investments (LTIs) |

• EM FX Monthly including currency preferences |

Thematic investments with a 5yr+ investment horizon |

• FX one-pagers (BRL, MXN, RUB, ZAR, TRY, CEE3, APAC) |

|

UBS CIO GWM June 2019 16

vk.com/id446425943

Appendix

Non-Traditional Assets

Non-traditional asset classes are alternative investments that include hedge funds, private equity, real estate, and managed futures (collectively, alternative investments). Interests of alternative investment funds are sold only to qualified investors, and only by means of offering documents that include information about the risks, performance and expenses of alter - native investment funds, and which clients are urged to read carefully before subscribing and retain. An investment in an alternative investment fund is speculative and involves significant risks. Specifically, these investments (1) are not mutual funds and are not subject to the same regulatory requirements as mutual funds; (2) may have performance that is volatile, and investors may lose all or a substantial amount of their investment; (3) may engage in leverage and other speculative investment practices that may increase the risk of investment loss; (4) are long-term, illiquid investments, there is generally no secondary market for the interests of a fund, and none is expected to develop; (5) interests of alternative investment funds typically will be illiquid and subject to restrictions on transfer; (6) may not be required to provide periodic pricing or valuation information to investors; (7) gener - ally involve complex tax strategies and there may be delays in distributing tax information to investors; (8) are subject to high fees, including management fees and other fees and expenses, all of which will reduce profits.

Interests in alternative investment funds are not deposits or obligations of, or guaranteed or endorsed by, any bank or other insured depository institution, and are not federally insured by the Federal Deposit Insurance Corporation, the Federal Reserve Board, or any other governmental agency. Prospective investors should understand these risks and have the financial ability and willingness to accept them for an extended period of time before making an investment in an alternative investment fund and should consider an alternative investment fund as a supplement to an overall investment program.

In addition to the risks that apply to alternative investments generally, the following are additional risks related to an investment in these strategies:

•Hedge Fund Risk: There are risks specifically associated with investing in hedge funds, which may include risks associated with investing in short sales, options, small-cap stocks, “junk bonds,” derivatives, distressed securities, non-U.S. securities and illiquid investments.

•Managed Futures: There are risks specifically associated with investing in managed futures programs. For example, not all managers focus on all strategies at all times, and managed futures strategies may have material directional elements.

•Real Estate: There are risks specifically associated with investing in real estate products and real estate investment trusts. They involve risks associated with debt, adverse changes in general economic or local market conditions, changes in governmental, tax, real estate and zoning laws or regulations, risks associated with capital calls and, for some real estate products, the risks associated with the ability to qualify for favorable treatment under the federal tax laws.

•Private Equity: There are risks specifically associated with investing in private equity. Capital calls can be made on short notice, and the failure to meet capital calls can result in significant adverse consequences including, but not limited to, a total loss of investment.

•Foreign Exchange/Currency Risk: Investors in securities of issuers located outside of the United States should be aware that even for securities denominated in U.S. dollars, changes in the exchange rate between the U.S. dollar and the issuer’s “home” currency can have unexpected effects on the market value and liquidity of those securities. Those securities may also be affected by other risks (such as political, economic or regulatory changes) that may not be readily known to a U.S. investor.

UBS CIO GWM June 2019 17

vk.com/id446425943

Appendix

UBS Chief Investment Office’s (“CIO”) investment views are prepared and published by the Global Wealth Management business of UBS Switzerland AG (regulated by FINMA in Switzerland) or its affiliates (“UBS”).

The investment views have been prepared in accordance with legal requirements designed to promote the independence of investment research.

Generic investment research – Risk information:

This publication is for your information only and is not intended as an offer, or a solicitation of an offer, to buy or sell any investment or other specific product. The analysis contained herein does not constitute a personal recommendation or take into account the particular investment objectives, investment strategies, financial situation and needs of any specific recipient. It is based on numerous assumptions. Different assumptions could result in materially different results. Certain services and products are subject to legal restrictions and cannot be offered worldwide on an unrestricted basis and/or may not be eligible for sale to all investors. All information and opinions expressed in this document were obtained from sources believed to be reliable and in good faith, but no representation or warranty, express or implied, is made as to its accuracy or completeness (other than disclosures relating to UBS). All information and opinions as well as any forecasts, estimates and market prices indicated are current as of the date of this report, and are subject to change without notice. Opinions expressed herein may differ or be contrary to those expressed by other business areas or divisions of UBS as a result of using different assumptions and/or criteria.

In no circumstances may this document or any of the information (including any forecast, value, index or other calculated amount (“Values”)) be used for any of the following purposes (i) valuation or accounting purposes; (ii) to determine the amounts due or payable, the price or the value of any financial instrument or financial contract; or (iii) to measure the performance of any financial instrument including, without limitation, for the purpose of tracking the return or performance of any Value or of defining the asset allocation of portfolio or of computing performance fees. By receiving this document and the information you will be deemed to represent and warrant to UBS that you will not use this document or otherwise rely on any of the information for any of the above purposes. UBS and any of its directors or employees may be entitled at any time to hold long or short positions in investment instruments referred to herein, carry out transactions involving relevant investment instruments in the capacity of principal or agent, or provide any other services or have officers, who serve as directors, either to/for the issuer, the investment instrument itself or to/for any company commercially or financially affiliated to such issuers. At any time, investment decisions (including whether to buy, sell or hold securities) made by UBS and its employees may differ from or be contrary to the opinions expressed in UBS research publications. Some investments may not be readily realizable since the market in the securities is illiquid and therefore valuing the investment and identifying the risk to which you are exposed may be difficult to quantify. UBS relies on information barriers to control the flow of information contained in one or more areas within UBS, into other areas, units, divisions or affiliates of UBS. Futures and options trading is not suitable for every investor as there is a substantial risk of loss, and losses in excess of an initial investment may occur. Past performance of an investment is no guarantee for its future performance. Additional information will be made available upon request. Some investments may be subject to sudden and large falls in value and on realization you may receive back less than you invested or may be required to pay more. Changes in foreign exchange rates may have an adverse effect on the price, value or income of an investment. The analyst(s) responsible for the preparation of this report may interact with trading desk personnel, sales personnel and other constituencies for the purpose of gathering, synthesizing and interpreting market information.

Tax treatment depends on the individual circumstances and may be subject to change in the future. UBS does not provide legal or tax advice and makes no representations as to the tax treatment of assets or the investment returns thereon both in general or with reference to specific client’s circumstances and needs. We are of necessity unable to take into account the particular investment objectives, financial situation and needs of our individual clients and we would recommend that you take financial and/or tax advice as to the implications (including tax) of investing in any of the products mentioned herein.

This material may not be reproduced or copies circulated without prior authority of UBS. Unless otherwise agreed in writing UBS expressly prohibits the distribution and transfer of this material to third parties for any reason. UBS accepts no liability whatsoever for any claims or lawsuits from any third parties arising from the use or distribution of this material. This report is for distribution only under such circumstances as may be permitted by applicable law. For information on the ways in which CIO manages conflicts and maintains independence of its investment views and publication offering, and research and rating methodologies, please visit www.ubs.com/research. Additional information on the relevant authors of this publication and other CIO publication(s) referenced in this report; and copies of any past reports on this topic; are available upon request from your client advisor.

Important Information about Sustainable Investing Strategies: Incorporating environmental, social and governance (ESG) factors or Sustainable Investing considerations may inhibit the portfolio manager’s ability to participate in certain investment opportunities that otherwise would be consistent with its investment objective and other principal investment strategies. The returns on a portfolio consisting primarily of ESG or sustainable investments may be lower than a portfolio where such factors are not considered by the portfolio manager. Because sustainability criteria can exclude some investments, investors may not be able to take advantage of the same opportunities or market trends as investors that do not use such criteria. Companies may not necessarily meet high performance standards on all aspects of ESG or sustainable investing issues; there is also no guarantee that any company will meet expectations in connection with corporate responsibility, sustainability, and/or impact performance.

Distributed to US persons by UBS Financial Services Inc. or UBS Securities LLC, subsidiaries of UBS AG. UBS Switzerland AG, UBS Europe SE, UBS Bank, S.A., UBS Brasil Administradora de Valores Mobiliarios Ltda, UBS Asesores Mexico, S.A. de C.V., UBS Securities Japan Co., Ltd, UBS Wealth Management Israel Ltd and UBS Menkul Degerler AS are affiliates of UBS AG. UBS Financial Services Incorporated of Puerto Rico is a subsidiary of UBS Financial Services Inc. UBS Financial Services Inc. accepts responsibility for the content of a report prepared by a non-US affiliate when it distributes reports to US persons. All transactions by a US person in the securities mentioned in this report should be effected through a US-registered broker dealer affiliated with UBS, and not through a non-US affiliate. The contents of this report have not been and will not be approved by any securities or investment authority in the United States or elsewhere. UBS Financial Services Inc. is not acting as a municipal advisor to any municipal entity or obligated person within the meaning of Section 15B of the Securities Exchange Act (the “Municipal Advisor Rule”) and the opinions or views contained herein are not intended to be, and do not constitute, advice within the meaning of the Municipal Advisor Rule.

External Asset Managers / External Financial Consultants: In case this research or publication is provided to an External Asset Manager or an External Financial Consultant, UBS expressly prohibits that it is redistributed by the External Asset Manager or the External Financial Consultant and is made available to their clients and/or third parties. For country disclosures, click here.

Version 04/2019. CIO82652744

© UBS 2019.The key symbol and UBS are among the registered and unregistered trademarks of UBS. All rights reserved.

UBS CIO GWM June 2019 18