B E Y O N D D E M A N D : C O N S U M E R S I N T H E E C O N O M I C S Y S T E M |

83 |

A: Total utility per bar

|

|

|

|

|

|

80 |

|

|

|

|

|

|

60 |

|

|

|

|

|

|

40 |

|

|

|

|

|

|

20 |

|

|

|

|

|

|

0 |

1 |

2 |

3 |

4 |

5 |

6 |

7 |

B: Marginal utility per bar

|

|

|

|

|

|

35 |

|

|

|

|

|

|

30 |

|

|

|

|

|

|

25 |

|

|

|

|

|

|

20 |

|

|

|

|

|

|

15 |

|

|

|

|

|

|

10 |

|

|

|

|

|

|

5 |

|

|

|

|

|

|

0 |

|

|

|

|

|

|

–5 |

1 |

2 |

3 |

4 |

5 |

6 |

7 |

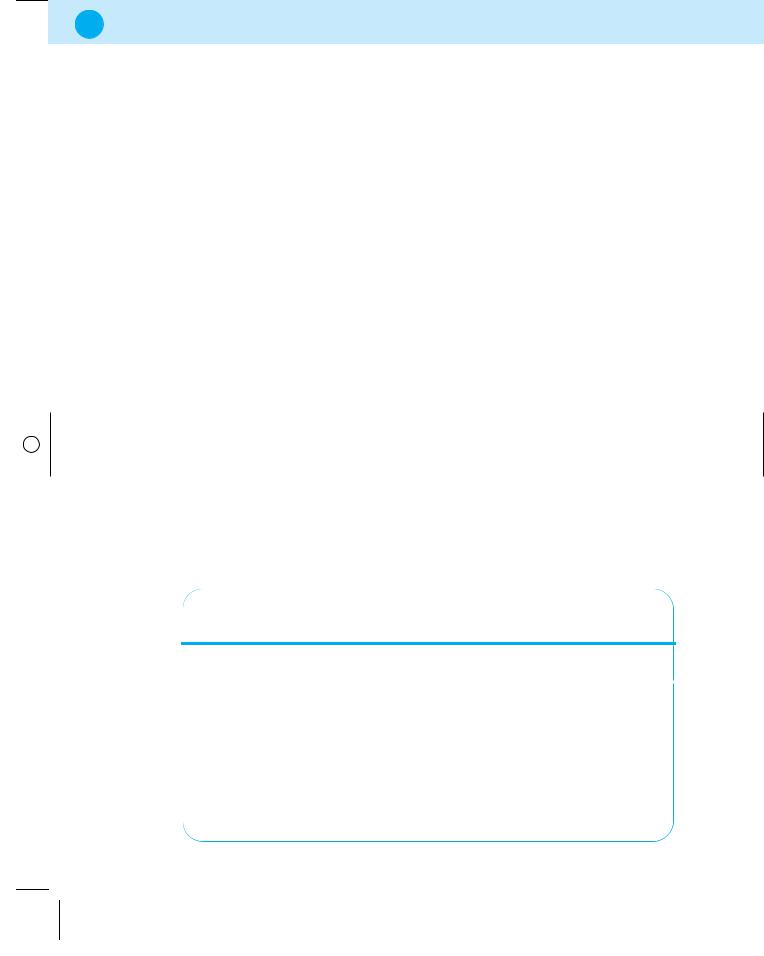

F I G U R E 3 . 1 T O T A L A N D M A R G I N A L U T I L I T Y : C H O C O L A T E

Consuming a sixth bar makes little sense because it leads to a decline in overall satisfaction, reflected in negative marginal utility. This information is also presented in Figure 3.1, with total utility in panel A and marginal utility in panel B.

When using the concept of utility, economists analyse consumption as if people can rank and quantify their preferences and can establish how much satisfaction they acquire from consuming different quantities of goods or services. In practice if you were asked to explain your satisfaction from consuming various quantities of chocolate, you might find it difficult and even more so if a number of different goods and cross-rankings were involved.

Economists do not assume that people engage in this process every time they consume something. However, economists do consider that rational people reveal their preferences by what they purchase and that they know what they like, what provides them with consumer satisfaction and that the utility generated from total and marginal consumption follow the general patterns as shown above; initially increasing and eventually falling total utility and declining marginal utility.

3.3.1THE ASSUMPTION OF RATIONALITY IN ECONOMICS

When economists use the term ‘rational’ in relation to consumers, the implications are that consumers are capable of estimating the satisfaction they derive from consuming goods or services, they can rank their preferences (e.g. if they prefer chocolate to cheese and cheese to sausages, they prefer chocolate to sausages) and that they act generally to maximize their own utility. Rationality assumes that consumers use all available information in making their decisions. It must be acknowledged that consumers do not have full information at all times to support their decisions, hence they are bounded by their knowledge and the

84 |

T H E E C O N O M I C S Y S T E M |

available information, or, people possess, as Herbert Simon put it, bounded rationality.

This means that people do not always make the choices that would objectively maximize their utility – if they had more complete information their choice might be different. It is relevant in complex decisions where receiving, storing, retrieving, transmitting (i.e. processing) relevant information can be complicated and timeconsuming. In many economic models people are assumed to display approximately rational behaviour.

If a choice arose between consuming a chocolate bar or a packet of crisps, the rational consumer would compare the utility they would derive from each product and make their preferred and subjective choice. They would also take an additional piece of information into account in this decision – the prices of the goods. Why? Because consumption preferences are limited by individuals’ income and they rationally make decisions about what to buy with this in mind, taking prices into consideration.

3 . 4 M A R G I N A L U T I L I T Y, P R I C E S A N D T H E L A W O F D E M A N D

Consider a person trying to decide how to spend money she has received and who knows her top preferences are either nights out (including taxi fare, entrance to a night club and food/drinks) which cost on average £50 or call credit for her mobile phone, at the same price. Analysis of marginal utility for both goods is provided in Table 3.3.

Her prime choice is a night out because the extra utility generated from one night out is greater than the extra utility generated by £50 call credit. After spending one night out, the next best choice for consumption would be a second night out because 19 units of utility is greater than 16 units generated from the first unit of call credit consumed. The next preferred option is call credit and so on. If she has received £200, it is possible to list what her preferred purchases will be because she will be rational and consume the goods that provide her with the greatest utility.

The preferences can be estimated simply as the marginal utility per pound generated by the goods. The marginal utility per pound for both goods is shown in Table 3.4 with the ranked preferences for consumption shown in parentheses.

With £200 to spend, the top four choices are a night out, followed by a second night out, followed by £50 call credit, followed by a third night out. With more money to spend, the remaining choices would come into play. After making six

B E Y O N D D E M A N D : C O N S U M E R S I N T H E E C O N O M I C S Y S T E M |

85 |

T A B L E 3 . 3 M A R G I N A L U T I L I T Y : C A L L C R E D I T A N D N I G H T S O U T

|

Marginal utility |

Marginal utility |

Quantity |

call credit (£50) |

nights out (£50) |

|

|

|

1 |

16 |

21 |

2 |

14 |

19 |

3 |

12 |

15 |

4 |

10 |

13 |

5 |

9 |

12 |

6 |

7 |

11 |

T A B L E 3 . 4 M A R G I N A L U T I L I T Y A N D

P R I C E R A T I O S

Quantity |

MU call credit |

MU/P (P = £50) |

MU nights out |

MU/P (P = £50) |

|

|

|

|

|

|

|

1 |

16 |

0.32 |

(3) |

21 |

0.42 (1) |

2 |

14 |

0.28 |

(5) |

19 |

0.38 (2) |

3 |

12 |

0.24 |

(7) |

15 |

0.30 (4) |

4 |

10 |

0.20 (10) |

13 |

0.26 (6) |

|

5 |

9 |

0.18 (11) |

12 |

0.24 (7) |

|

6 |

7 |

0.14 (12) |

11 |

0.22 (9) |

|

choices, the consumer is indifferent between either a night out or call credit because they yield the same marginal utility/price ratio.

Such analysis indicates what the individual’s demand for nights out and call credit are, given prices, income and preferences. All consumers’ demand decisions summed together give rise to the demand curve. From the information here, when the price of call credit or a night out is £50, and this individual has £200 to spend, one unit of call credit and three nights out are demanded.

86 |

T H E E C O N O M I C S Y S T E M |

Since demand decisions result from the marginal utility/price ratio, demand decisions would be different if prices changed. Consider what happens if the cost of a night out increased to £60. This changes the ranking of preferences since the marginal utility per pound changes, as shown in Table 3.5. The result is that with £200 to spend, two nights out and two units of call credit would be demanded. Consumers change their mind about what to consume in response to the changes in the marginal utility/price ratio. In other words the quantity demanded changes in response to price changes.

Although the price of call credit is unchanged in Table 3.5, the relative price of call credit decreased as the price of a night out increased and so the quantity demanded of call credit increased. It is in terms of relative prices that economists conduct their analysis. Another way of stating the same idea in terms of the concepts already introduced is to say that following the price rise, the opportunity cost of a night out has increased. More call credit must to be foregone to release the money for a night out. When prices change the consumer rearranges their consumption choices, always preferring goods with the highest possible ratio of marginal utility to price.

We can go further than this to say that the rational consumer will make their consumption choices so that the marginal utility/price is equal for all goods consumed. This is logical since consumers would always prefer to allocate their money to goods that yield the highest marginal utility per pound but each time they consume one more of any good, the marginal utility from that good declines while the marginal utility of another good which they buy one unit less of increases. In equilibrium, consumers make their consumption choices so that they end up

T A B L E 3 . 5 M A R G I N A L U T I L I T Y A N D P R I C E

R A T I O S – N E W P R I C E S

Q |

MU call credit |

MU/P (P = £50) |

MU nights out |

MU/P (P = £60) |

||

|

|

|

|

|

|

|

1 |

16 |

0.32 |

(2) |

21 |

0.35 |

(1) |

2 |

14 |

0.28 |

(4) |

19 |

0.32 |

(2) |

3 |

12 |

0.24 |

(6) |

15 |

0.25 |

(5) |

4 |

10 |

0.20 |

(8) |

13 |

0.22 |

(7) |

5 |

9 |

0.18 (10) |

12 |

0.20 |

(8) |

|

6 |

7 |

0.14 (12) |

11 |

0.18 (10) |

||