vk.com/id446425943 |

Lukoil |

Russia |

|

Energy: Integrated Oil & Gas |

|

Disclosures

Production and Distribution of VTB Capital Research Reports outside the United States

The information and opinions contained within VTB Capital research reports are prepared by research analysts associated with JSC VTB Capital, VTB Capital PLC and their non-U.S. affiliates (each such entity, a “VTB Group entity,” and all such entities collectively, the “VTB Group”), as indicated on the front page of this VTB Capital research report. Research reports produced by VTB Group entities are distributed under the VTB Capital logo (each such research report, a “VTB Capital research report”). This VTB Capital research report is distributed outside the United States by VTB Group entities.

Distribution of VTB Capital Research Reports to Investors within the United States

This VTB Capital research report is distributed to investors located within the United States by Xtellus Capital Partners Inc. (“Xtellus”), a broker-dealer registered with the U.S. Securities and Exchange Commission (the “SEC”) and a member of the Financial Industry Regulatory Authority (“FINRA”). Xtellus had no involvement in the preparation of this VTB Capital research report, and is distributing this VTB Capital research report to investors located within the United States as a “third-party research report” as defined in Rule 2241(a)(14). Xtellus has accepted responsibility for the content of this VTB Capital research report to the extent required by SEC guidance under Rule 15a-6.6 under the U.S. Securities Exchange Act of 1934 (the “Exchange Act”). Transactions in securities discussed in this VTB Capital research report must be effected by VTB Group entities with U.S. investors through Xtellus in accordance with Rule 15a-6. If you are an investor located within the United States, you should contact Xtellus if you wish to communicate with the VTB Capital research analysts who wrote this report, or you wish to conduct any transactions in securities described in this report.

Relationship between VTB and Xtellus

Xtellus is the successor entity of VTB Capital Inc, which was an SEC-registered broker dealer and affiliate of the VTB Group. The VTB Group sold its interest in VTB Capital Inc. with effect from August 31st 2018 to a newly formed holding company, Khepri Capital, LLC, an entity established and owned by certain VTB Capital Inc. personnel. In connection with the sale, VTB Capital Inc. was re-named Xtellus. While the VTB Group no longer has any ownership interest in Xtellus, Xtellus continues to provide certain services to VTB Group entities. Specifically, Xtellus (i) acts as agent for VTB Group entities pursuant to Rule 15a-6 under the Exchange Act in connection with securities transactions effected by VTB Group entities with U.S. investors, and (ii) is the exclusive distributor of VTB Capital research reports into the United States. Xtellus receives fees for research and Rule 15a-6 intermediation services it provides to VTB Capital Group entities, including fees for the right to distribute Xtellus research reports outside the United States. While the VTB Group no longer has any ownership interest in Xtellus, in light of the research and Rule 15a-6 service arrangements between the VTB Group and Xtellus, this VTB Capital research report includes disclosures pursuant to FINRA Rule 2241(h)(4) and FINRA Rule 2242(g)(3) applicable to VTB Group entities as if such VTB Group entities were affiliates of Xtellus. The inclusion of these affiliate disclosures should not be construed as implying that any VTB Group entity is affiliated with Xtellus for any other purpose.

Conflict of Interest Disclosures.

VTB Group entities do and seek to do business with companies covered in their research reports. Thus, investors should be aware that the VTB Group may have a conflict of interest that could affect the objectivity of this research report. Investors should consider this research report as only a single factor in making their investment decision. Where an issuer referred to in this report is not included in the disclosure table, the issuer is either considered not to be covered by VTB Capital Research, or the reference is considered to be incidental and therefore the issuer is not a subject company within this report.

Certain disclosures on the companies covered by this VTB Capital research report are set forth below. Additional disclosures on the companies covered by this report can be obtained by accessing the following webpages:

Research disclosures webpage - http://research.vtbcapital.com/ServicePages/Disclosures.aspx.

Investment Recommendations disclosures webpage – https://www.vtbcapital.com/about/information-disclosure/investment- recommendations/

Additional disclosures on the companies covered by this report can be obtained by writing to the offices listed on the back page. In order to receive i) a summary of any basis of the valuation or methodology and the underlying assumptions used to either evaluate a financial instrument or an issuer, or to set a price target for a financial instrument, as well as an indication and a summary of any changes in the valuation, methodology or underlying assumptions; ii) detailed information about the valuation or methodology and the underlying assumptions in any non-proprietary models; or iii) material information about the proprietary models used; please consult the VTB Capital Research web-site at https://research.vtbcapital.com or contact the authors of this document.

15 March 2019 |

20 |

vk.com/id446425943 |

Lukoil |

|

|

|

|

Russia |

|

|

|

|

Energy: Integrated Oil & Gas |

|

|

|

|

Issuer Specific Disclosures |

|

|

|

|

Disclosure checklist |

|

|

|

|

Company |

Ticker |

Recent price |

Disclosure |

|

Lukoil |

LKOH RX |

5,677 (RUB) |

4a, 12a |

4a. VTB Capital or an affiliated company is a provider of liquidity and/or a market maker in the securities of the relevant issuer at the time this research report was published. VTB Capital or an affiliated company will buy and sell securities of the relevant issuer on a principal basis.

12a. VTB Capital or an affiliated company has a long shareholding position exceeding 0.5% of the total issued share capital in the relevant issuer.

Analysts Certification

The research analyst(s) whose name(s) appear on this VTB Capital research report certify pursuant to SEC Regulation AC that: i) all of the views expressed in this research report accurately reflect their personal views about the subject security or issuer, and ii) no part of the research analysts’ compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed by the research analysts in this VTB Capital research report.

The research analysts whose names appear on VTB Capital research reports received compensation that is based upon various factors including VTB Capital Group’s total revenues, a portion of which are generated by VTB Capital Group’s investment banking activities.

Investment Ratings

VTB Capital uses a three-tiered Investment Rating system for stocks under coverage: Buy, Hold, or Sell.

The three main ratings correspond to the next 12-month Expected Total Return (ETR), defined as the difference between the Target Price and the Last Price as indicated by Bloomberg divided by that Last Price plus the expected Dividend Yield over the next 12 months. Under this Investment Ratings system, Buy, Hold, and Sell have the following meanings: (as of the publishing date):

BUY: ETR exceeds plus 20% or more HOLD: ETR is between zero and plus 20% SELL: ETR is less than zero

VTB Capital Research confirms that published Buy, Hold or Sell ratings conform to these definitions at the time a Target Price is established or an Investment Rating is revised. Between such revisions, day-to-day movements in the prices of financial instruments could result in a temporary discrepancy between the Investment Rating and the aforementioned definition. Analysts address such discrepancies based on their scale and duration.

UNDER REVIEW: In the event that significant information about an issuer is due to be announced or is expected to become public in the foreseeable future, or the analyst needs time to evaluate such information, which was announced recently, s/he might choose to place that issuer Under Review. This means that the analyst is suspending the previously published financial forecasts, Target Price and investment rating in order to review them while waiting for the impending information. As such, they are no longer valid and should not be relied upon.

RESTRICTED: In certain circumstances, VTB Capital is not able to communicate issuer ratings due to internal policy and/or law and regulations. In this case, any revision of the financial forecasts, Target Prices and Investment Ratings will be carried out only after the Restricted status is removed.

Notwithstanding the above, VTB Capital may from time to time issue investment recommendations predicated on a different time horizon (such as short-term trading recommendations) to that which is described above. Where VTB Capital issues such an investment recommendation, the use of an alternative time horizon for the purpose of formulating such investment recommendation might result in differences between such investment recommendation and any investment rating published in accordance with the Investment Rating system described above. In addition, short-term trading recommendations may result in short-term price movements contrary to the recommendations in this research report.

15 March 2019 |

21 |

vk.com/id446425943 |

Lukoil |

Russia |

|

Energy: Integrated Oil & Gas |

|

The below table details the distribution of VTB Capital’s Investment Ratings on the basis of the three-tier recommendation system described above.

VTB Capital Ratings Distribution

Investment Ratings Distribution

Buy |

58 |

49% |

Hold |

37 |

31% |

Sell |

16 |

13% |

Restricted |

0 |

0% |

Not Rated |

0 |

0% |

Under Review |

8 |

7% |

|

119 |

|

Source: VTB Capital Research as at 28 February 2019

Ratings Distribution for Investment Banking Relationships

Buy |

8 |

47% |

Hold |

3 |

18% |

Sell |

2 |

12% |

Restricted |

0 |

0% |

Not Rated |

0 |

0% |

Under Review |

4 |

23% |

|

17 |

|

The VTB Capital Ratings Distribution tables above account for the recommendations on all instruments covered, rather than the number of companies covered. In instances where we provide a recommendation for more than one instrument issued by a company, these are counted separately. A list of those companies for which we cover more than one instrument can be found at DoubleRecPLC20190228.pdf.

12-month Target Prices

VTB Capital research analysts employ a variety of methods for estimating the fair value of financial instruments covered by them. These may include, but are not limited to, a Discount Cash Flow (DCF) model, a Dividend Discount Model (DDM), Net Asset Value (NAV) valuation, financial or asset-based multiples of analogous companies and a sum-of-the-parts (SOTP) valuation. The research analyst’s choice of methods used in each particular instance is based on the specifics of the investment case in question. The Target Price reflects the research analyst’s informed opinion on the price which is likely to be attained by the financial instrument in 12 months, subsequent to the date of the Target Price determination. The Target Price is underpinned by the aforementioned fair value estimates, and will belong to the range established by them.

Conflicts Management Arrangements

VTB Capital Research has been published in accordance with our conflict management arrangements, which are available at http://research.vtbcapital.com/ServicePages/Files/CoI+Arrangements+Research.pdf.

15 March 2019 |

22 |

vk.com/id446425943

VTB Capital Research

|

Moscow Research |

London Research |

|

Phone: +7 495 660 4253 |

Phone: +44 (0) 20 3334 8557 |

|

research@vtbcapital.com |

research@vtbcapital.com |

VTB Capital Offices

|

JSC VTB Capital |

VTB Capital plc |

VTB Capital plc |

|

Federation Tower West |

14 Cornhill |

9 Battery Road #27-01 |

|

12, Presnenskaya emb. |

London EC3V 3ND |

Straits Trading Building |

|

Moscow, 123100, Russia |

Phone: +44 (0) 20 3334 8000 |

Singapore 049910 |

|

Phone: +7 495 960 9999 |

Fax: +44 (0) 20 3334 8900 |

Phone: +65 6220 9422 |

|

www.vtbcapital.com |

www.vtbcapital.com |

Fax: +65 6225 0140 |

|

|

|

www.vtbcapital.com |

|

|

|

|

|

VTB Capital Hong Kong Limited |

|

|

|

Unit 2301, 23/F |

|

|

|

Cheung Kong Center |

|

|

|

2 Queen’s Road Central |

|

|

|

Hong Kong |

|

|

|

Phone: +852 3195 3688 |

|

|

|

Fax: +852 3195 3699 |

|

|

|

www.vtbcapital.com |

|

|

Xtellus Capital Partners Inc. (Sales and Research queries for US clients)

Xtellus Capital Partners Inc. Sales

452 Fifth Avenue, 23rd Floor

New York, NY 10018

Phone: +1646 527 6400

Sales@XtellusCapital.com

VTB Group entities do and seek to do business with companies covered in their research reports. Thus, investors should be aware that the VTB Group may have a conflict of interest that could affect the objectivity of this research report. Investors should consider this research report as only a single factor in making their investment decision.

This research report is for information purposes only and does not constitute nor is it intended as an offer or solicitation for the purchase or sale of securities or other financial instruments. Neither the information contained in this research report nor any future information made available with the subject matter contained herein will form the basis of any contract. Information and opinions contained herein have been compiled or arrived at by VTB Group from publicly available information and sources that VTB Group believes to be reliable. Whilst every care has been taken in preparing this research report, no research analyst, director, officer, employee, agent or adviser of any member of the VTB Group gives or makes any representation, warranty or undertaking, whether express or implied, and accepts no responsibility or liability as to the reliability, accuracy or completeness of the information set out in this research report. Any responsibility or liability for any information contained herein is expressly disclaimed. All information contained herein is subject to change at any time without notice. No member of the VTB Group has an obligation to update, modify or amend this research report or to otherwise notify a reader thereof in the event that any matter stated herein, or any opinion, projection, forecast or estimate set forth herein, changes or subsequently becomes inaccurate, or if research on the subject company is withdrawn. Furthermore, past performance is not indicative of future results.

The investments and strategies discussed herein may not be suitable for all investors or any particular class of investor. Investors should make their own investment decisions using their own independent advisors as they believe necessary and based upon their specific financial situations and investment objectives when investing. Investors should consult their independent advisors if they have any doubts as to the applicability to their business or investment objectives of the information and the strategies discussed herein. This research report is being furnished to certain persons as permitted by applicable law, and accordingly may not be reproduced or circulated to any other person without the prior written consent of a member of the VTB Group. This research report may not be relied upon by any retail customers or persons to whom this research report may not be provided by law. Unauthorised use or disclosure of this research report is strictly prohibited. Members of the VTB Group and/or their respective principals, directors, officers and employees (including, but not limited to, persons involved with the preparation or issuance of this research report) may own, have positions or effect transactions in the securities or financial instruments referred to herein or in the investments of any issuers discussed herein, may engage in securities transactions in a manner inconsistent with the research contained in this research report and with respect to securities or financial instruments covered by this research report, may sell to or buy from customers on a principal basis and may serve or act as director, placement agent, advisor or lender, or make a market in, or may have been a manager or a co-manager of the most recent public offering in respect of any investments or issuers of such securities or financial instruments referenced in this research report or may perform any other investment banking or other services for, or solicit investment banking or other business from, any company mentioned in this research report. Disclosures of conflicts of interest, if any, are found at the end of the text of this research report. Members of the VTB Group may have acted upon or used the information or conclusions contained in this research report, or the research or analysis on which they are based, before publication of this research report. Investing in the Russian Federation, its markets and in Russian securities and financial instruments involves a high degree of risk, and many persons, physical and legal, may be restricted from dealing in the securities markets of the Russian Federation. Investors should perform their own due diligence before investing. It is particularly important to note that securities and financial instruments denominated in foreign currencies and ADRs and other investments discussed herein are subject to exchange rate fluctuations that may adversely affect the value of the investment. The value of investments may fall as well as rise and investors may not get back the amount invested. Prices and availability of securities, financial instruments or investments are also subject to change without notice. The views and opinions expressed in this research report accurately reflect the personal views of the authors of this research report about the subject investments, securities and financial instruments and issuers and do not necessarily reflect the views of any member of the VTB Group. No part of the compensation of the authors of this research report was, is or will be directly or indirectly related to the specific recommendations or views contained in the research report. By accepting this research report, you agree to be bound by the foregoing limitations. This material is not intended for the use of private investors.

In Russia, this report is approved and/or communicated by JSC VTB Capital, a professional securities market participant regulated by the Central Bank of Russia.

In the United Kingdom this report is approved and/or communicated by VTB Capital plc London, a member of the London Stock Exchange and authorized by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. This report is intended for those persons that would be classified as Eligible Counterparties or Professional Clients under the Financial Conduct Authority’s Conduct of Business rules.”

This research report is distributed in Singapore by VTB Capital plc to accredited investors, expert investors or institutional investors only (as defined in the applicable Singapore laws and regulations and is not intended to be distributed directly or indirectly to any other class of person). Recipients of this report in Singapore are to contact VTB Capital plc, Singapore branch in respect of any matters arising from, or in connection with, this report. VTB Capital plc, Singapore branch is regulated by the Monetary Authority of Singapore.

This research report is distributed in Hong Kong by VTB Capital Hong Kong Limited, a licensed corporation (CE Ref: AXF967) licensed by the Hong Kong Securities and Futures Commission to “professional investors” (as defined in the Hong Kong Securities and Futures Ordinance and its subsidiary legislation) only.

For important disclosures and equity rating histories regarding companies that are the subject of this report, please see the VTB Capital Research Website: http://research.vtbcapital.com/ServicePages/Disclosures.aspx, or contact your research representative.

Copyright © 2019 by VTB Capital. All rights reserved. Please cite source when quoting.

vk.com/id446425943Capital Market Outlook

Chief Investment Office

The opinions are those of the author(s) and subject to change. |

MARCH 11, 2019 |

IN THIS ISSUE

MACRO STRATEGY

Early signs that the global slowdown currently ending are propelling equity markets higher. Expectations for a slowdown in capital spending (capex) seem misplaced given the new U.S. tax structure and the developing shortage of available workers. Higher U.S. productivity was the big surprise in 2018. Fundamentals suggest it should continue to move higher this year, helping to contain inflation and prolong the expansion.

GLOBAL MARKET VIEW

Student loan debt in the U.S. has more than doubled in the past ten years to reach $1.5 trillion, driven by rapidly growing tuition costs, higher enrollment and the 2008 financial crisis. In a six-question Q&A, we outline some of the critical concepts on student loan debt and its economic impact.

THOUGHT OF THE WEEK

Beijing recently announced its 2019 defense budget with spending set to grow by 7.5% to 1.19 trillion yuan ($178 billion). The data on defense spending comes as China’s National Party Congress reduced its economic growth target for 2019 to a range of 6% to 6.5%. The government is in “whatever-it-takes” mode, supporting the global reflationary trade in global equities this year.

PORTFOLIO CONSIDERATIONS

Given our expectation of elevated volatility, we suggest higher-quality exposure, largeover small-caps, companies with pricing power, cash on their balance sheets, the ability to grow dividends, and less leverage.

MACRO STRATEGY

A MIRROR IMAGE

Chief Investment Office Macro Strategy Team

2019 is shaping up to be a mirror image of 2018, which began with widespread euphoria about a continuing synchronized global expansion. By the spring, however, aggressive Federal Reserve (Fed) rate-hike plans and trade-war concerns had sparked a global slowdown. In sharp contrast, this year has begun with widespread expectations of continued global slowing. Instead, with the Fed and trade concerns now becoming tailwinds, in our view, the global economy is on the cusp of a new upcycle, which should become apparent, likely by the second half.

Early signs of the turnaround are apparent in long-lead-time leading indicators, like stock prices, credit spreads, interest rates and general financial conditions. The U.S. was least impacted by the trade and rate-hike headwinds in 2018, although by the end of the year it also began to show signs of fatigue. China, on the other hand, got hit hardest, as was evident in its much more severe bear market in equities. Once the U.S. began to slow, the Fed stepped back to give growth

Data as of 03/11/2019 and subject to change.

a chance. Signs of the impending return to synchronized global growth in 2019 have been flashing from the relative outperformance and earlier bottoming process in emergingmarket (EM) currencies and equities, especially the Chinese yuan and equities since late last year.

As we wrote last spring, the early victims of the Fed rate hikes were those EMs, like Turkey and Argentina, that had leveraged up during the zero-rate era of plentiful dollar liquidity. Developed economies outside the U.S were also more impacted, not least because they were more vulnerable to China’s disproportionate weakening, especially Germany, which has the biggest structural trade surplus in the world and is overly reliant therefore on global trade.

The lack of a coordinated pro-growth policy response and political limbo add to European woes. As George Soros—Hungarian- American investor and philanthropist—put it recently, “Europe

is sleepwalking into oblivion…” While lagging behind the Fed’s normalization path, the European Central Bank (ECB) still managed to hurt domestic growth by prematurely beginning its ill-timed quantitative tightening program even as inflation falls far short of

Merrill Lynch Wealth Management makes available products and services offered by Merrill Lynch, Pierce, Fenner & Smith Incorporated (MLPF&S), a registered broker-dealer and Member SIPC, and other subsidiaries of Bank of America Corporation (BofA Corp.). Investment products:

Are Not FDIC Insured |

Are Not Bank Guaranteed |

May Lose Value |

|

|

|

vk.com/id446425943

MACRO STRATEGY (Continued)

its target. A stubborn refusal to acknowledge this has widened the gap between a now chastened, pro-growth Fed and a still dawdling ECB. Nevertheless, a turnaround in China and other EMs, together with a still strong U.S. economy, will help Europe muddle along as global trade reaccelerates in the wake of an expected U.S. China trade deal, low inflation, lower interest rates and widespread stimulus efforts as other countries follow the lead of the U.S. tax reform and deregulation policies to remain competitive.

WEAK U.S. GROWTH BLIP PASSING

Economic indicators in the U.S. have held up well despite the global slowdown. While sectors tied to global trade and

manufacturing have cooled a bit, they remain more robust than those elsewhere. For example, the February Institute for Supply Management (ISM) manufacturing index has fallen sharply to the lowest level in about two years. Still, according to the ISM, its 54.2 reading has been consistent with 3% gross domestic product (GDP) growth, and the nonmanufacturing sector, which constitutes about 80% of the U.S. economy, remains even stronger, with a big surprise jump in February. All told, the composite measure, which includes both the manufacturing and nonmanufacturing indices, remains at a level only seen near the peak of the past 25 years. Expectations for a return to “secular stagnation” would seem to be misplaced.

The key is the takeoff in capital spending that has surprised economic forecasters despite the clear historical record of tax reforms’ positive impact on corporate investment. The last two comparable reforms to corporate investment incentives were the 1964 and 1986 tax reforms. Both were followed by long periods of near double-digit growth in capex. Likewise, the biggest surprise in the stronger-than-expected U.S. fourth-quarter GDP growth rate that propelled the U.S. to its strongest year-over-year growth since 2005 was strength in capex. In particular, spending on research and development is currently growing at twice its pre-tax reform rate. In the modern information age and servicedominated economy, R&D is a critical component for advancing productivity, especially in a fully employed U.S. economy where finding workers is the biggest problem facing businesses.

According to research by Cornerstone Macro that looked at the S&P1500 companies, the percentage of firms showing positive year-over-year growth comparison in capex is in a strong uptrend since tax reform was passed following a steady downtrend from 2012, when the initial recovery out of the financial crisis ended. The research also notes a broadening out of capital spending to more sectors of the economy. While growth has moderated from its initial burst, it’s still double digit. A follow-up report shows effective tax-rate cuts averaged about nine percentage points.

Of particular interest, the new rules narrowed the gap between domestic and multinational firms with over a ten-point cut on average for the former and only about three points for the latter. As a result, domestic firms’ capex growth has accelerated sharply relative to multinational companies. This helps explain the strong relative growth outperformance in the U.S. over the past year.

Bottom line: A U.S. slowdown in 2019 is largely predicated on a fizzling out of capex. The 1964 and 1986 tax reforms and recent data suggest this is highly unlikely. Furthermore, housing, which got hit hard by higher interest rates last year, should do better this year since rates have reversed and household formation remains very strong. The current turnaround in homebuilder surveys and stocks supports this view, not a slowdown view. Finally, and perhaps most importantly, a robust labor market with strengthening real wages and incomes in a low-inflation environment is the key to another year of surprisingly strong U.S. growth, in our opinion. The new capex boom is fueling higher productivity and rising real incomes, as of December 2018, while containing inflation. It took the Fed a while to catch on to this positive dynamic and stop attacking wage increases.

REST OF THE WORLD FOLLOWS THE STRONG U.S. HIGHER

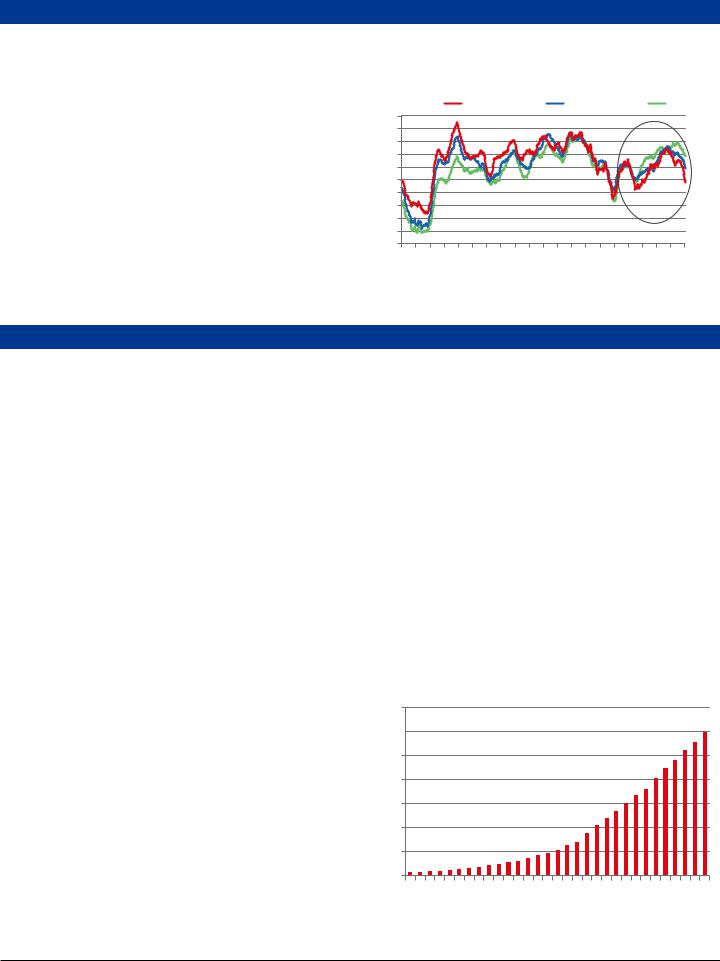

The turn in EM currencies and equity markets suggests global trade will resume a more normal growth pace after the sharp slowing of 2018. Exhibit 1 shows the historical pattern of leading indicators for a composite of economies that account for the bulk of global GDP.

Exhibit 1: Muted Mini Cycles Since the Financial Crisis.

OECD + Major 6 Non-Mem: Total Leading Indicator (2-month %change, annualized, Leading 6 months) OECD + Major 6 Non-Mem: Total Leading Indicator (SA, Amplitude Adjusted)

2-month % change, annualized |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Index |

||||||||||||||||

8% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

104 |

6% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

103 |

4% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

102 |

2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

101 |

0% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

100 |

-2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

99 |

-4% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

98 |

-6% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

97 |

-8% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

96 |

|

|

|

|

n |

|

|

|

n |

|

|

n |

|

|

|

|

n |

|

|

|

|

n |

|

|

n |

|

|

n |

|

n |

|

|

|

Jan |

|

|

n |

|

|

|

Ja |

|

|

Ja |

|

Ja |

|

|

|

Ja |

|

|

|

Ja |

|

Ja |

|

Ja |

Ja |

|

|

|

|

Ja |

||||||||||

|

|

|

- |

|

|

|

- |

|

|

- |

|

|

|

|

- |

|

|

|

|

- |

|

|

- |

|

|

- |

|

- |

|

|

|

|

- |

|

- |

|

|

|

0 |

|

|

3 |

|

6 |

|

|

|

9 |

|

|

|

2 |

|

|

05 |

|

8 |

|

11 |

|

|

|

4 |

7 |

|

||||||||

|

9 |

|

|

9 |

|

|

99 |

|

|

|

9 |

|

|

|

0 |

|

|

|

|

00 |

|

|

|

|

1 |

|

201 |

|

|

|||||||

9 |

|

|

|

19 |

|

|

|

|

|

9 |

|

|

|

0 |

|

|

|

0 |

|

|

|

20 |

|

0 |

|

|

|

|

||||||||

1 |

|

|

|

|

|

|

|

1 |

|

|

1 |

|

|

|

|

2 |

|

|

|

|

2 |

|

|

2 |

|

|

|

2 |

|

|

|

|

|

|||

Sources: Organisation for Economic Co-operation and Development (OECD)/ Haver Analytics, Chief Investment Office. Data as of March 5, 2019.

What’s striking about the chart since 2009 is the muted yet clear pattern of three distinct minicycles, which have tracked globalgrowth momentum since the financial crisis. Unlike the global economy in the 1990s or 2000s, the amplitude of each minicycle is less than half of those of the previous global expansions.

As a result, while world growth has been trend-like, it has not

CIO Capital Market Outlook |

2 |

vk.com/id446425943

MACRO STRATEGY (Continued)

overheated or weakened to the point of recession. The lack of overheating helps explain the relatively well-contained behavior of inflation. Long-leading indicators now suggest a fourth minicycle could likely begin this year. These cycles have each previously lasted about three years, with two years of rising momentum for growth and equity prices followed by about a year of weakening momentum and equity-market corrections.

GLOBAL MARKET VIEW

HOW MUCH OF A BURDEN: Q&A ON STUDENT LOAN DEBT

Kathryn A. Cassavell, CFA®, Vice President and Market Strategy Analyst

The U.S. student debt burden has been described to the American public in countless ways: a bubble about to burst, a systemic risk to the financial system, a threat to U.S. competitiveness, a source of income inequality, a looming burden for the U.S. government, the reason millennials are living in their parents’ basements. The list goes on.

Given the various viewpoints and investor inquiries on the topic, below is a brief Q&A addressing common client questions related to student loan debt.

WHAT IS THE CURRENT STATE OF U.S. STUDENT LOAN DEBT?

According to the latest figures from the Fed, U.S. student debt outstanding totaled $1.5 trillion in the fourth quarter of 2018. That’s more than the amount Americans owe on credit cards and auto loans, but a fraction of America’s total mortgage debt ($9.1 trillion).

Unlike the other consumer credit sectors mentioned above, student debt was largely unaffected by the household deleveraging trend that occurred after the financial crisis. Since 2008, total student loans outstanding grew 128% compared to 61% growth for auto loans, a decline of -1% for mortgages, and just 0.5% growth for credit card debt.

Student loan delinquency rates have also been a concern in recent years. The total amount of student loan balances that are 90+ days delinquent reached $166 billion last year, or 11.4% of the total balance. (The Fed estimates that the true figure could actually be double this stated amount). At

the start of the last financial crisis, the comparable figure for mortgage debt was $267 billion (Q4 2017), peaking at $785 billion in delinquent balances as of Q1 2010.

HOW DID WE GET HERE?

The rise of student loan debt can be traced back to the latter half of the 20th century, as various government initiatives

Chartered Financial Analyst® and CFA® are registered trademarks owned by CFA Institute.

These relatively restrained, self-correcting cycles help account for and support the longevity of this expansion, which is expected to set an all-time U.S. record in July. With the Fed moving to a more robust commitment to a 2% inflation rate, the odds of another two-year upcycle starting in 2019 look pretty good, in our opinion.

encouraged students to pursue higher education. With more Americans attending college, aggregate student debt levels rose. Brookings Institution estimates, “about one-quarter of the aggregate increase in student loans since 1989 is due to more students enrolling in college.”1

Meanwhile, the average cost of a college degree has risen exponentially. Over the past 40 years, the inflation-adjusted cost of tuition and fees per student climbed by almost 300%, while the average median income (adjusted for inflation) increased by just 18% (Exhibit 2).

Exhibit 2: U.S. College Tuition Outpaces Median Income Gains.

Inflation-adjusted average tuition and median income

Indexed to 100 (1978 = 100)

400

Average tuition and fees (public 4-year universities)

350

Median household income

300

250

200

150

100

50

0

1978 |

1982 |

1986 |

1990 |

1994 |

1998 |

2002 |

2006 |

2010 |

2014 |

2018 |

Tuition per student and income levels, adjusted for inflation, and indexed to 1978 price levels. Sources: The College Board, Census Bureau, Center on Budget and Policy Priorities. Data through 2017.

The 2008 recession also played an important role in the recent build-up of student loan debt. As the economy turned, states slashed their budgets, and more of the burden fell on students to fund their education. At the same time, university enrollment picked up, especially among older Americans looking to retrain for the job market after being laid off. This also fueled higher enrollments at for-profit universities, where average student debt levels and defaults tend to be higher.

ARE WE REACHING A TIPPING POINT FOR STUDENT DEBT?

Although leverage has been creeping higher, with delinquency rates for student loans much higher than those for other areas

1 Brookings Institution, “The Looming Student Loan Default Crisis is Worse than We Thought.” January 11, 2018.

CIO Capital Market Outlook |

3 |

vk.com/id446425943

GLOBAL MARKET VIEW (Continued)

of consumer credit, we do not believe the student loan market is a bubble that is about to burst. Various signs point to an improving situation.

First, overall U.S. consumer balance sheets are currently strong. Total consumer debt as a percentage of GDP has come down from a peak of 87% in 2008 to just 65% today. Meanwhile, consumer debt service payments as a percentage of disposable personal income are at record lows. And although interest rates over the past year have shifted higher, we do not believe this is an immediate concern for borrowers since most student debt carries a fixed rate.

Second, delinquencies have been growing at a slower pace since 2014 (Exhibit 3). An overall healthier consumer backdrop combined with an increase in income-driven repayment plans should help keep delinquency and default rates in check.2

Exhibit 3: Student Loans Transitioning into Delinquency at a Slower Pace.

Transition into delinquency

Share of previously up-to-date loan balances becoming 30+ days delinquent

12% |

11% |

10% |

9% |

8% |

7% |

Q2-04 Q4-04 Q2-05 Q4-05 Q2-06 Q4-06 Q2-07 Q4-07 Q2-08 Q4-08 Q2-09 Q4-09 Q2-10 Q4-10 Q2-11 Q4-11 Q2-12 Q4-12 Q2-13 Q4-13 Q2-14 Q4-14 Q2-15 Q4-15 Q2-16 Q4-16 Q2-17 Q4-17 Q2-18 Q4-18 |

Sources: New York Fed Consumer Credit Panel/Equifax. Data as of Q4 2018.

Meanwhile college tuition increases appear to have slowed. Tuition and fees at four-year public colleges rose just 2.5% last year, roughly in line with core inflation and wage gains.3

ARE STUDENT LOANS A LOOMING SYSTEMIC RISK TO THE FINANCIAL SYSTEM?

Fears of an eventual system-wide financial shock caused by student loan debt are overblown, in our opinion.

Most student loans (roughly 90%) are held on the U.S. government balance sheet. So while a wave of student loan defaults would be a burden on the federal budget, we think student debt is less likely to cause a widespread shock to the financial markets.

The student loan system also has mechanisms in place that gradually shift the financial burden to borrowers, which should cause

2The New York Times, “How to Clean Up the Student Loan Mess.” April 6, 2018.

3Tuition measured by The College Board, “Trends in College Pricing 2018.” Comparatively, CPI core inflation was up 2.2% in December 2018 (year-over-year) and average hourly earnings were up 3.3% in December 2018 (year-over-year) according to the Bureau of Labor Statistics.

financial effects to filter through the economy over the course of multiple years. Thus, deteriorating conditions in the student loan market are expected to have a more gradual economic impact.

Another mitigating risk: robust U.S. employment growth and solid income gains, boosting the financial wherewithal, at least in the medium term, of those shouldering the burden of debt.

WHAT ARE THE ECONOMIC CONSEQUENCES OF RISING STUDENT DEBT?

There are mixed views on the overall economic impact of student loan debt. On the one hand, taking on student debt has important benefits for borrowers. Higher levels of educational attainment are generally correlated with lower rates of unemployment, higher wages and greater spending levels.

On the other hand, some research has shown that rising student loan debt has had a negative impact on specific sectors of the economy. For example, a recent study by the Fed finds that 20% of the decline in the homeownership rate for younger Americans since 2005 can be attributed to the rise in student loan debt—translating to roughly 400,000 fewer homeowners.4

Older adults are also starting to feel the burden, as they carry their student loans later in life and take on more debt to support their children and grandchildren. This is a trend we are following closely, since an increasing debt burden can have important implications for the spending patterns of the baby boomers as they enter retirement.

WHAT ARE THE INVESTMENT IMPLICATIONS?

While the aggregate economic effect from student loan debt may be relatively mild and spread out over several years, certain sectors can be negatively impacted in the near term.

As discussed, one such area is the housing market, where rising student debt has contributed to a delay in home purchases by young consumers. We acknowledge that there remains considerable pent-up demand in the housing market as millennials reach their prime home buying years; however, the growing burden of student loans could mean slower progress and/or less runway than previously anticipated.

Buying sentiment among young consumers has also weakened in the auto sector. The latest data from the University of Michigan show that buying conditions for motor vehicles have been deteriorating much more rapidly for younger consumers (Exhibit 4). This contrasts with prior business cycles when younger consumers used to have a more favorable outlook

on auto purchases than older consumers. According to the

4The Federal Reserve, “Can Student Loan Debt Explain Low Homeownership Rates for Young Adults?” January 2019.

CIO Capital Market Outlook |

4 |

vk.com/id446425943

GLOBAL MARKET VIEW (Continued)

survey, “the less favorable views of the young were mirrored in their more frequent concerns about the incurrence of additional debt.”5

These are just two areas of the U.S. economy where a more cautious view is warranted. By contrast, discount retailers could be beneficiaries of more budget-conscious millennials and baby boomers. In terms of credit markets, we do not think that rising student loan balances and delinquencies will pose a challenge to the U.S. government budget just yet. However, we are watching the policy response to this growing concern and will reassess investment implications as the theme evolves.

Exhibit 4: Vehicle Buying Conditions Deteriorating Faster

Among Younger Adults.

Current conditions for buying vehicles |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Index score |

|

|

|

Ages 18-34 |

|

|

|

|

Ages 35-54 |

|

|

|

|

Ages 55+ |

||||||

170 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

160 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

150 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

140 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

130 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

120 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

110 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

100 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

90 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

80 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

70 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1979 |

1981 |

1983 |

1985 |

1987 |

1989 |

1991 |

1993 |

1995 |

1997 |

1999 |

2001 |

2003 |

2005 |

2007 |

2009 |

2011 |

2013 |

2015 |

2017 |

2019 |

5 “Age Reversal in Buying Attitudes,” University of Michigan Surveys of Consumers. |

12 month moving average. Sources: University of Michigan Surveys of Consumers; Haver |

February 22, 2019. |

Analytics. Data as of February 2019. |

THOUGHT OF THE WEEK

EVIDENCE OF “WHATEVER-IT-TAKES” IN CHINA

Lauren J. Sanfilippo, Vice President and Market Strategy Analyst

China has long maintained a strong penchant for building things—whether high-speed railroads, world-class suspension bridges, mile-long tunnels, massive airports and, of course, high-rise buildings. To wit, China completed 88 buildings of at least 200 meters in height last year, which is a record number of completions for the nation, and a staggering 61.5% of the global total. In the U.S., comparatively, 13 completions were recorded. In terms of new supertall skyscrapers (300 meters or more), China completed 11 out of a global total of 18 for the year.6 While skyscrapers are a lagging economic indicator (given it takes years to plan, design and construct a building), we suspect the pace of building will remain relatively robust in the next few years as the government implements more reflationary measures to sustain growth in the 6% to 7% range. Infrastructure investment, a key element of the Chinese government’s economic stimulus plan, will not only include skyscrapers and high-speed railways but a 5G rollout and modernization of its military.

Beijing recently announced its 2019 defense budget that (1) fuels global concerns over China’s growing military prowess and

(2) continues the 25-year run of annual increases in defense spending. Overall spending is set to grow by 7.5% to 1.19 trillion yuan ($178 billion) (Exhibit 5), with the aim of modernizing the nation’s weapons capabilities, including more spending on aircraft carriers, stealth fighters, cruise missiles and submarines.

The data on defense spending comes as China’s National Party Congress reduced its economic growth target for 2019

6The Council on Tall Buildings and Urban Habitat, Year in Review: Tall Trends of 2018, March 2019.

to a range of 6% to 6.5%. In our view, that level of growth is achievable but the inconvenient truth is that China is diving deeper in debt and each stimulus package is taking longer to take effect. In 2008, it took China’s economy only three months to bounce back, while more recently in 2012, it was six months. Especially given other challenging factors such as its reliance on special purpose bonds to finance many infrastructure projects, China’s spending comes at a great cost as companies and consumers are choking on debt, driven by eased credit,

lax regulatory hurdles, and state subsidies over the previous decade. Despite currently rising vacancy rates, expanding levels of debt, excess inventory—all key metrics to monitor over the near term—China’s building and spending mania rolls on. The government is in “whatever-it-takes” mode, supporting the reflationary trade in global equities this year.

Exhibit 5: China’s Defense Budget.

(In Billions of Yuan)

1,400

1,200 |

1,190 |

|

|

|

|

1,000

800

600

400

200

0

1989199019911992199319941995199619971998199920002001200220032004200520062007200820092010201120122013201420152016201720182019

Figures for 2018 and 2019 do not include funds from provincial governments. Source: China National Statistics Yearbook. Data as of March 2019.

CIO Capital Market Outlook |

5 |

vk.com/id446425943

INDEX DEFINITIONS

Securities indexes assume reinvestment of all distributions and interest payments. Indexes are unmanaged and do not take into account fees or expenses. It is not possible to invest directly in an index.

Indexes are all based in dollars.

Dow Jones Industrial Average is a price-weighted measure of 30 U.S. blue-chip U.S. companies. The index covers all industries except transportation and utilities.

NASDAQ Composite Index is a broad-based capitalization-weighted index of stocks in all three NASDAQ tiers: Global Select, Global Market and Capital Market. The index was developed with a base level of 100 as of February 5, 1971.

S&P 500 Index includes a representative sample of 500 leading companies in leading industries of the U.S. economy. Although the index focuses on the large-cap segment of the market, with approximately 75% coverage of U.S. equities, it is also an ideal proxy for the total market.

Purchasing Manager’s Index (PMI) is based on a survey of purchasing managers at more than 300 manufacturing firms by the Institute for Supply Management (ISM), the index monitors changes in production levels from month to month.

IMPORTANT DISCLOSURES

This material was prepared by the Chief Investment Office (CIO) and is not a publication of BofA Merrill Lynch Global Research. The views expressed are those of the CIO only and are subject to change. This information should not be construed as investment advice. It is presented for information purposes only and is not intended to be either a specific offer by any Merrill Lynch or U.S. Trust entity to sell or provide, or a specific invitation for a consumer to apply for, any particular retail financial product or service that may be available.

Global Wealth & Investment Management (GWIM) is a division of Bank of America Corporation. Merrill Lynch Wealth Management, Merrill Edge®, U.S. Trust, and Bank of America Merrill Lynch are affiliated sub-divisions within GWIM. The Chief Investment Office, which provides investment strategies, due diligence, portfolio construction guidance and wealth management solutions for GWIM clients, is part of the Investment Solutions Group (ISG) of GWIM.

Investing involves risk, including the possible loss of principal. No investment program is risk-free, and a systematic investing plan does not ensure a profit or protect against a loss in declining markets. Any investment plan should be subject to periodic review for changes in your individual circumstances, including changes in market conditions and your financial ability to continue purchases.

Economic or financial forecasts are inherently limited and should not be relied on as indicators of future investment performance. It is not possible to invest directly in an index.

Asset allocation, diversification, dollar cost averaging and rebalancing do not ensure a profit or protect against loss in declining markets. Dollar cost averaging involves continual investment in securities regardless of fluctuating price levels; you should consider your willingness to continue purchasing during periods of high or low price levels.

Past performance is no guarantee of future results.

Stocks of small-cap companies pose special risks, including possible illiquidity and greater price volatility than stocks of larger, more established companies. Companies may reduce or eliminate dividend payment to shareholders. Historically, dividends make up a large percentage of stocks’ total return.

Investing in fixed-income securities may involve certain risks, including the credit quality of individual issuers, possible prepayments, market or economic developments and yields and share price fluctuations due to changes in interest rates. When interest rates go up, bond prices typically drop, and vice versa. Income from investing in municipal bonds is generally exempt from Federal and state taxes for residents of the issuing state. While the interest income is tax-exempt, any capital gains distributed are taxable to the investor. Income for some investors may be subject to the Federal Alternative Minimum Tax (AMT).

Investments focused in a certain industry may pose additional risks due to lack of diversification, industry volatility, economic turmoil, susceptibility to economic, political or regulatory risks and other sector concentration risks.

Investments in real estate securities can be subject to fluctuations in the value of the underlying properties, the effect of economic conditions on real estate values, changes in interest rates, and risks related to renting properties, such as rental defaults.

Nonfinancial assets, such as closely-held businesses, real estate, oil, gas and mineral properties, and timber, farm and ranch land, are complex in nature and involve risks including total loss of value. Special risk considerations include natural events (for example, earthquakes or fires), complex tax considerations, and lack of liquidity. Nonfinancial assets are not suitable for all investors. Always consult with your independent attorney, tax advisor, investment manager, and insurance agent for final recommendations and before changing or implementing any financial, tax, or estate planning strategy.

Investments in tangible assets are highly volatile and are speculative. There are special risks associated with an investment in commodities, including market price fluctuations, regulatory changes, interest rate changes, credit risk, economic changes, and the impact of adverse political or financial factors.

Alternative Investments such as private equity funds, can result in higher return potential but also higher loss potential. Changes in economic conditions or other circumstances may adversely affect your investments. Before you invest in alternative investments, you should consider your overall financial situation, how much money you have to invest, your need for liquidity, and your tolerance for risk.

Neither Merrill Lynch, U.S. Trust nor any of their affiliates or advisors provide legal, tax or accounting advice. You should consult your legal and/or tax advisors before making any financial decisions.

The investments discussed have varying degrees of risk. Some of the risks involved with equities include the possibility that the value of the stocks may fluctuate in response to events specific to the companies or markets, as well as economic, political or social events in the U.S. or abroad. Bonds are subject to interest rate, inflation and credit risks. Investments in high-yield bonds may be subject to greater market fluctuations and risk of loss of income and principal than securities in higher rated categories. Investments in foreign securities involve special risks, including foreign currency risk and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are magnified for investments made in emerging markets. Investments in a certain industry or sector may pose additional risk due to lack of diversification and sector concentration. Investments in real estate securities can be subject to fluctuations in the value of the underlying properties, the effect of economic conditions on real estate values, changes in interest rates, and risk related to renting properties, such as rental defaults. There are special risks associated with an investment in commodities, including market price fluctuations, regulatory changes, interest rate changes, credit risk, economic changes and the impact of adverse political or financial factors. Income from investing in municipal bonds is generally exempt from federal and state taxes for residents of the issuing state. While the interest income is tax exempt, any capital gains distributed are taxable to the investor. Income for some investors may be subject to the federal alternative minimum tax (AMT).

Investing directly in Master Limited Partnerships (MLP’s), foreign equities, commodities or other investment strategies discussed here, may not be available to, or appropriate for, Merrill Edge clients. However, these investments may exist as part of an underlying investment strategy within exchange-traded funds (ETF’s) and mutual funds, which are available to Merrill Edge clients.

© 2019 Bank of America Corporation. All rights reserved. |

AR7L6RNH |