vk.com/id446425943 |

|

|

78 |

Citi GPS: Global Perspectives & Solutions |

March 2018 |

|

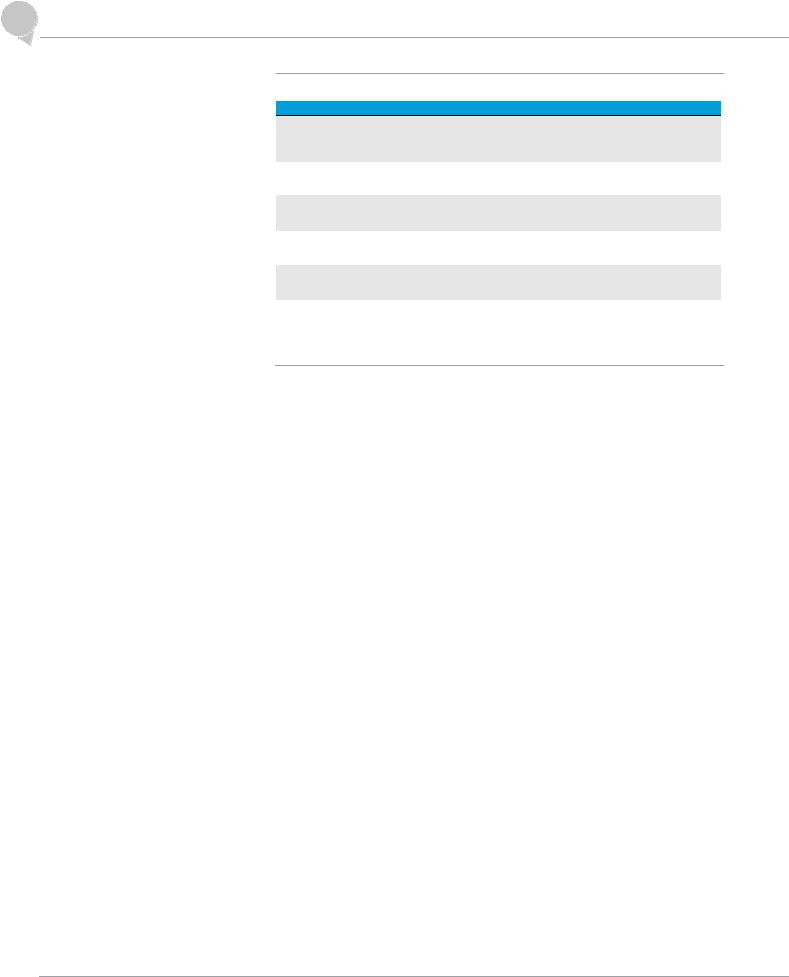

Figure 75. Banks’ Challenges and Leveris Banking Core Solutions |

|

|

Problems |

Solutions |

Scalability

Complexity

Cost

Speed to Market

Data

User Experiences

Source: Leveris, Citi

Banking systems can't keep up with the exponential growth in volumes brought about by the digitization of banking, and soon the Internet of Things

A typical traditional bank runs more than 600 inter-connected software applications which increase risk and complexity

Years of software upgrades and middleware solutions mean banks can spend up to €1bn a year just to maintain the system.

Traditional banks running on legacy systems can take over one year to launch new products and services.

Silo’d data and complex systems make it nearly impossible for banks to use data in any meaningful way.

Banking customers have come to expect great services at their fingertips. Unfortunately, banks cannot deliver.

The Leveris platform is a flexible, adaptable, and scalable technology stack that leverages data to scale to your needs and grows with you.

The Leveris Banking platform delivers all retail products from the same platform; no more complex spaghetti junction systems.

A transparent pay-as-you-grow pricing model ensures costs are closely aligned to desired business outcomes.

Launch financial products that share no issues with any legacy IT infrastructure in weeks not months or years.

Access detailed, real-time customer data through state-of-the-art data warehousing to understand your customers better.

Improve customer relationships across all channels and throughout the customer life cycle. Leveris allows you to create beautifully designed front-end applications.

Journey to the Cloud

We find it amazing how little of tech spend is available for new development and functionality. Two-thirds or more of banks’ IT budgets are spent on maintenance. And even the ‘change-the-bank’ tech spend is often for compliance or regulatory driven change. Thus, the amount spent on real change or innovation is a small fraction of usually large IT budgets. One area of potential real change is the journey to adopting Cloud computing in ever larger parts of the banking ecosystem.

Cloud and more modern architecture offer solutions to legacy IT issues — a promise of efficiency, agility and speed to market. The move to the cloud provides the cost and efficiency play, while the reworking of legacy applications provides the benefit of agility, nimbleness and speed-to-market with product development.

With workloads shifting to the cloud, there should be cost savings. Expense saves will come as the scalability and elasticity create a more efficient environment. Hence, reduced requirements for physical equipment and a physical footprint – allowing banks to reduce server counts and shrink and/or eliminate data centers. Furthermore, public cloud usage could have additional labor cost savings as the infrastructure or software would be managed externally.

While cost savings are one important side-effect of cloud technology, we believe this is not really the key unique selling point. The leveraging of the cloud allows for flexibility and nimbleness. To the extent banks can enhance their speed to market with applications, this is a major benefit particularly relative to the ineffectiveness of legacy IT to deliver changes with speed.

Being innovative and responsive to customer demands (e.g., make updates to an app with no downtime) could be a key differentiator over time. In addition, we see significant benefits from getting data analytics and AI right, particularly for an industry that underwrites risk.

© 2018 Citigroup