vk.com/id446425943 |

|

|

106 |

Citi GPS: Global Perspectives & Solutions |

March 2018 |

Ripple has partnered with 75 banking clients to test the Ripple RTXP technology (disclosed on company website) including global banks like MUFG, RBC, Santander, Standard Chartered, Westpac, Credit Agricole and Axis Bank to name a few. Most banks are however still internally testing the system, before moving to commercial production. MoneyGram (a U.S.-based money transfer company) also recently teamed up with Ripple to use XRP in its payment flows, enabling faster international transfers at reduced costs (Bloomberg).

We believe RTXP is unlikely to be a huge benefit to Tier 1 banks and large value payments. This is because the system would still have to rely on large banks to be connectors for high value payments, as they are the only players with liquidity. Having said that, it could benefit Tier 3 banks, which have smaller transaction sizes, as it reduces longer settlement times in today’s system, especially through low volume corridors, where there may be additional hops. The biggest hurdle these banks face is the need to send funds through central banks to the correspondent’s for payment. ILP essentially converts those central bank settlements to sequential book entry transfers, which will be much faster.

We believe the toughest hurdle Ripple faces is getting banks to adopt their technology and consequently build a network, which existing players (SWIFT) already have.

How Are Central Bank Cryptocurrencies Different

While privately issued virtual currencies remain potentially risky and unstable, we have seen increased interest from central banks globally around the concept of central bank issued virtual currencies or Central Bank Crypto-Currencies (CBCC). CBCCs could enable entities (individuals/businesses) to make real time payments and store value in electronic central bank money form – which could be denominated in the national currency. However, the very concept raises more questions than it answers, including – How is monetary policy transmission impacted? Would banks lose client deposit funding? Will it increase risks to financial stability? Should these transactions be anonymous or routed through some central clearing?

IMF Managing Director Christine Lagarde spoke at a BoE event on how virtual currencies are among the top three factors that could change central banking over next generation (the other two factors being new models of financial intermediation, and AI). Ms. Lagarde foresees countries with weak institutions and unstable national currencies readily adopting such virtual currencies – which she calls “Dollarization 2.0”. Taken to its logical conclusion, officially issued digital currencies could allow non-bank entities to hold an account directly with the central bank. Commercial banks could face the ultimate disintermediation, at least for client deposits.

© 2018 Citigroup

vk.com/id446425943 |

|

|

|

|

|

107 |

March 2018 |

Citi GPS: Global Perspectives & Solutions |

|

|

|||

|

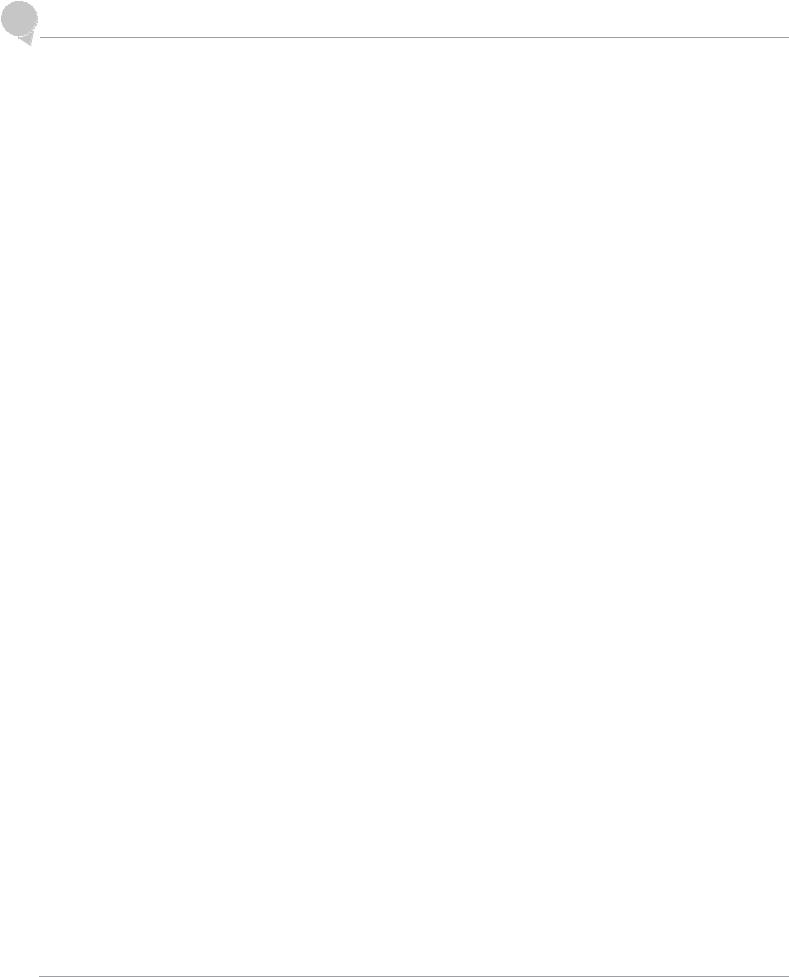

Figure 100. Money Flower: A Taxonomy Of Money |

|

|

|

||

|

|

Electronic |

|

|

Central bank- |

|

|

Universally |

|

|

|

||

|

|

Virtual |

|

|

issued |

|

|

accessible |

|

currency |

|

|

|

|

|

Bank |

|

|

|

|

|

|

deposits, |

|

|

|

|

|

|

mobile |

|

Settlement |

|

|

|

|

money |

|

|

||

|

|

|

|

or reserve |

Peer-to-Peer |

|

|

|

Deposited |

accounts |

|

||

|

|

currency |

|

|

|

|

|

|

accounts |

|

CBCC |

|

|

|

|

|

|

|

Local |

|

|

|

|

|

|

(wholesale) |

|

|

|

|

CBCC |

|

Currency |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

(retail) |

|

|

|

|

|

Cash |

Crypto- |

Crypto-currency |

|

|

|

|

|

|

|||

|

|

|

currency |

(Wholesale) |

|

|

Commodity

money

Source: BIS, Citi Research

A recent BIS paper outlines what CBCCs may look like and provides a taxonomy of money (see Figure 100). The taxonomy distinguishes between two possible forms of CBCC – a widely available, consumer-facing payment instrument targeted at retail transactions; and a restricted-access, digital settlement token for wholesale payment applications. The BIS paper further states that while it seems unlikely that bitcoin or its sisters will displace sovereign currencies, they have demonstrated the viability of the underlying blockchain or distributed ledger technology.

However, it must be noted that CBCCs are differentiated from other forms of central bank money such as cash and reserves as they can be exchanged in a decentralized manner, distinguishing them from other existing forms of electronic central bank money (such as reserves), which are exchanged in a centralized fashion across accounts at the central bank.

What Are Central Bankers Saying on CBCCs?

Canada – Bank of Canada is studying digital currency in a different way. It is actively involved in a research paper on the concept as well as experimenting on it through the projects i.e. Project Jasper.

European Union – In Sep. 2017, the ECB rejected Estonia's plan to launch its own state-run digital currency and indicated that the ECB will not allow any other EU member states to introduce their own currency.

Japan – Yoko Kawai, the head of the FinTech Center at the Bank of Japan said in Dec. 2017 that the central bank doesn’t see a need for issuing a digital currency as there is no demand. (link)

However, Japan banks plan to introduce a J-coin for 2020 Tokyo Olympics and have gained support from central bank / regulators. These coins are expected to be convertible into yen on a one-to-one basis, operating via a smartphone / QR codes that can be scanned in stores (FT).

© 2018 Citigroup

vk.com/id446425943 |

|

|

108 |

Citi GPS: Global Perspectives & Solutions |

March 2018 |

Saudi Arabia – Saudi Arabian Monetary Authority is working with the UAE central bank to issue a digital currency. The two countries would accept it for cross-border transactions.

Singapore – Monetary Authority of Singapore is working on “Project Ubin” to study if central bank money can be transferred real-time. Recently Ravi Menon, Managing Director of MAS said at a UBS Wealth Insights event in Singapore that he would not rule out the possibility of the MAS issuing a cryptocurrency directly to the public; however he was not sure it would be a good idea. (link)

Sweden – Riksbank published a report on “E-krona project – First interim report” in Sept. The central bank is studying if E-krona can be issued in place of cash and if a safe and efficient payment system can be developed.

United Kingdom –.Bank of England has no plans to issue a central bank issued cryptocurrency, however it does research on the topic. Recently BOE’s Governor Mark Carney said he sees fundamental issues with central bank backed cryptocurrencies.

© 2018 Citigroup