JPM_Europe Year Ahead 2019_watermark

.pdfvk.com/id446425943

vk.com/id446425943

vk.com/id446425943

vk.com/id446425943

vk.com/id446425943

vk.com/id446425943

Mislav Matejka, CFA |

Europe Equity Research |

(44-20) 7134-9741 |

03 December 2018 |

mislav.matejka@jpmorgan.com |

|

Global FX Outlook 2019

Late-cycle Dollar Divergence

Paul MeggyesiAC and Team

(44-20) 7134-2714 paul.meggyesi@jpmorgan.com

This is an extract taken from ‘Global FX Strategy 2019: Late-cycle Dollar Divergence’, published on 21 November 2018

The most notable (and unexpected) phenomenon for global FX markets this past year was the 8.9% resurgent bounce in the broad dollar from February lows, undoing the bulk of 2017’s bear market.

But credit for dollar strength this year does not rest solely with US fiscal largesse and exceptional US growth; an unexpected slowdown in the rest- of-world - particularly the pillar economies of the Eurozone and China - as well as EM stress contributed as much as US strength.

The biggest change we expect in 2019 will be the fading of US economic exceptionalism, as diminishing fiscal impulse and a tightening Fed takes US growth below 2% by 2H. But this does not translate into a broad bear market for the dollar more generally.

The other key differentiating factor for FX next year could be the move by the Fed into outright restrictive territory, overlaid with the symbolic reversal of the decade-long tailwind of expanding central bank balance sheets.

So whereas USD could eventually slip vs reserve currencies due to a narrowing in this year’s artificially wide growth gaps, the dollar could nevertheless make further headway against deficit currencies as the era of QE gives way to QT.

This looming end of financial repression will also drive outperformance of creditor countries vs deficit and debtor countries, especially this late in the business cycle when investors would in any case be paring exposure to high-beta currencies vulnerable to the next downturn.

This year-ahead outlook also discusses end-of- cycle dynamics and other themes & risks that will likely occupy the mindset of markets in 2019, including implications of quantitative tightening, risk if the Fed pauses, threats to the dollar’s reserve currency status, trade war and other geopolitcal risks.

Top macro trades: A restrictive Fed (long USD/JPY, short NZD/USD, -3M/+6M AUD/JPY OT downside), risk of Fed pause (short USD/SEK), US-China trade war (short CNH TWI), Global political risks (short EUR/GBP)

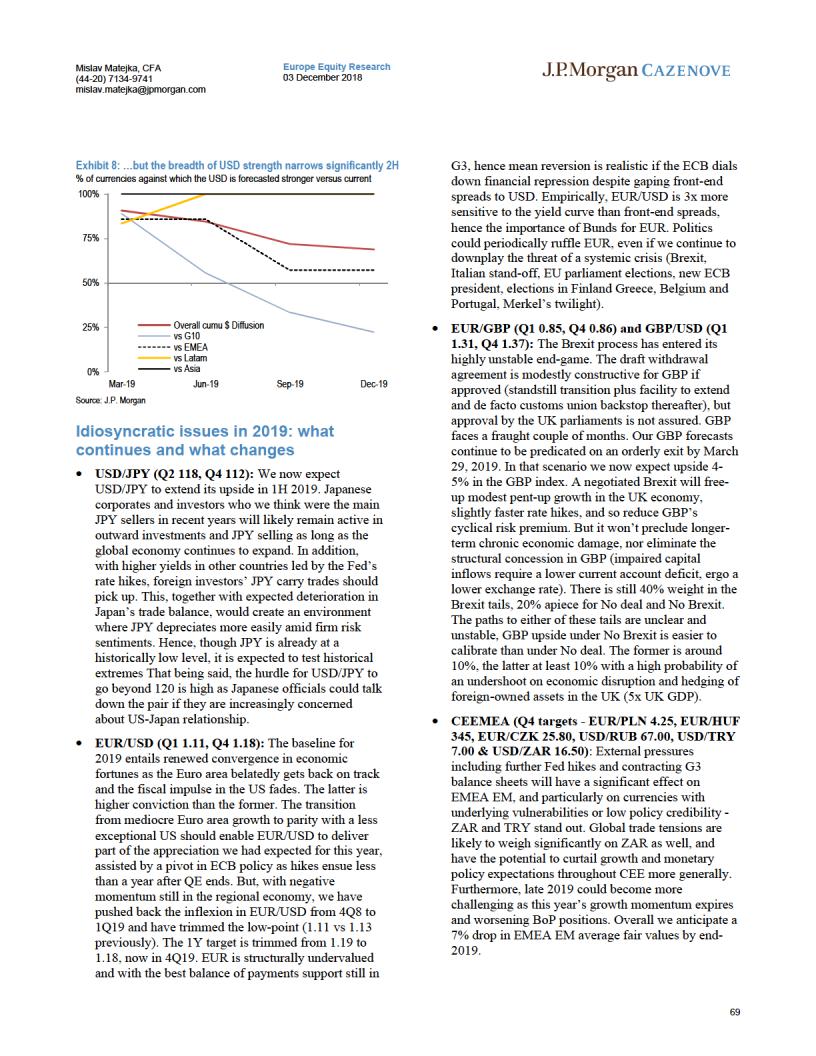

Exhibit 1: Relative growth impulses explain the dollar’s rebound well this year…

%6m change in USD TWI: Actual vs model based on change in the Global FRI and US-Global FRI spread

14 |

|

USD Index, %6m |

12 |

|

|

10 |

|

Model |

|

|

|

8 |

|

|

6 |

|

|

4 |

|

|

2 |

|

|

0 |

|

|

-2 |

|

|

-4 |

|

|

-6 |

|

|

-8 |

|

|

2014 |

2016 |

2018 |

Source: J.P. Morgan

Exhibit 2: … although global mediocrity contributed as much if not more to dollar strength than US exceptionalism

%6m change in USD TWI: Model based on change in the Global FRI and US-Global FRI spread, contributions from each component

8 |

|

|

|

Contribution of widening US-Global FRI spd |

|

|

|

||

|

|

|

|

|

6 |

|

|

|

Contribtuion of lower Global FRI |

|

|

|

||

|

|

|

|

4

2

0

-2

-4

-6

2014 |

2016 |

2018 |

Source: J.P. Morgan

A less exceptional US is mixed for the dollar rather than outright bearish

The most notable (and unexpected) phenomenon for global FX markets this past year was no doubt the 8.9% resurgent bounce in the broad dollar from February lows, undoing the bulk of 2017’s dollar bear market. This came as Trumponomics ended up delivering in the US President’s second, rather than first year, with fiscal policy fueling the acceleration of US growth to 4% by mid-year. But credit for dollar strength this year does not rest solely with US fiscal largesse; an

66

vk.com/id446425943

vk.com/id446425943

vk.com/id446425943

vk.com/id446425943