vk.com/id446425943

Anglo American – HOLD

Renaissance Capital

6 February 2019

Metals & Mining

Figure 79: Anglo American, $mn (unless otherwise noted) |

|

|

|

|

|

|

|

|

|

|

|

|||

Anglo American |

|

AGLJ.J |

|

|

|

|

|

Target price, ZAR: |

|

|

340 |

|||

Market capitalisation, $mn: |

|

36,489 |

|

|

|

|

|

|

Share price, ZAR: |

|

|

345 |

||

Enterprise value, $mn: |

|

51,574 |

|

|

|

|

|

|

Potential 12-month return: |

|

4.5% |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dec-YE |

2016 |

2017 |

|

2018E |

2019E |

2020E |

Dec-YE |

2016 |

2017 |

|

2018E |

2019E |

2020E |

|

Income statement |

|

|

|

|

|

|

|

Balance sheet |

|

|

|

|

|

|

Revenue |

23,142 |

28,650 |

|

29,833 |

28,499 |

28,130 |

|

Net operating assets |

32,315 |

33,172 |

|

32,171 |

31,897 |

32,800 |

Underlying EBITDA |

6,104 |

8,823 |

|

9,593 |

9,916 |

8,645 |

|

Financial instruments |

497 |

211 |

|

172 |

199 |

208 |

Underlying EBIT |

3,822 |

6,247 |

|

6,818 |

7,017 |

5,696 |

|

Equity |

19,016 |

22,972 |

|

23,517 |

25,343 |

25,973 |

Net interest |

-567 |

-635 |

|

-473 |

-313 |

-245 |

|

Minority interest |

5,309 |

5,910 |

|

5,736 |

6,020 |

6,256 |

Taxation |

-821 |

-1,770 |

|

-2,136 |

-2,125 |

-1,728 |

|

Net debt |

8,487 |

4,501 |

|

3,090 |

732 |

779 |

Minority interest in profit |

-329 |

-891 |

|

-969 |

-1,138 |

-944 |

|

|

|

|

|

|

|

|

Net profit for the year |

1,594 |

3,166 |

|

3,044 |

3,441 |

2,779 |

|

Balance sheet ratios |

|

|

|

|

|

|

Underlying earnings |

2,210 |

3,272 |

|

3,319 |

3,441 |

2,779 |

|

Gearing* |

30.9% |

16.4% |

|

11.6% |

2.8% |

2.9% |

Underlying EPS, USc |

172 |

257 |

|

261 |

271 |

219 |

|

Net debt to EBITDA |

1.4x |

0.5x |

|

0.3x |

0.1x |

0.1x |

|

|

RoCE |

10.8% |

17.8% |

|

19.8% |

20.7% |

16.3% |

||||||

Thomson Reuters consensus EPS, USc |

|

|

|

240 |

258 |

230 |

|

RoIC (after tax) |

6.0% |

15.1% |

|

10.9% |

15.8% |

11.0% |

DPS declared, USc |

0 |

102 |

|

104 |

135 |

207 |

|

RoE |

12.4% |

15.6% |

|

14.3% |

14.1% |

10.8% |

Underlying EBIT |

|

|

|

|

|

|

|

Cash flow statement |

|

|

|

|

|

|

Platinum |

185 |

512 |

|

791 |

1,089 |

1,289 |

|

Operating cash flow |

4,573 |

8,101 |

|

6,210 |

8,916 |

6,748 |

EBIT margin |

4% |

10% |

|

14% |

22% |

26% |

|

Capex (net of disposals) |

-2,388 |

-2,150 |

|

-2,268 |

-3,950 |

-3,867 |

Diamonds |

1,019 |

873 |

|

738 |

775 |

789 |

|

Other cash flows |

2,045 |

-688 |

|

-182 |

0 |

0 |

EBIT margin |

17% |

15% |

|

12% |

13% |

13% |

|

FCF |

4,230 |

5,263 |

|

3,760 |

4,966 |

2,881 |

Copper |

261 |

923 |

|

1,228 |

1,074 |

1,004 |

|

Equity shareholders' cash |

4,423 |

4,607 |

|

2,722 |

3,973 |

2,102 |

EBIT margin |

9% |

22% |

|

25% |

25% |

23% |

|

Dividends and share buy-backs |

0 |

-621 |

|

-1,311 |

-1,615 |

-2,149 |

Nickel |

-15 |

0 |

|

94 |

37 |

113 |

|

Surplus (deficit) cash |

4,423 |

3,986 |

|

1,411 |

2,358 |

-48 |

EBIT margin |

-4% |

0% |

|

17% |

7% |

18% |

|

Cash flow ratios |

|

|

|

|

|

|

Iron ore and manganese |

1,275 |

1,978 |

|

1,391 |

2,331 |

1,666 |

|

|

|

|

|

|

|

|

EBIT margin |

46% |

57% |

|

40% |

63% |

51% |

|

Working capital days |

52 |

33 |

|

33 |

20 |

22 |

Coal |

1,112 |

2,274 |

|

2,866 |

2,025 |

1,145 |

|

Capex/EBITDA |

43.4% |

28.0% |

|

27.7% |

45.7% |

51.0% |

EBIT margin |

21% |

32% |

|

36% |

30% |

19% |

|

FCF yield |

15.9% |

16.9% |

|

10.0% |

12.5% |

7.2% |

Other |

-15 |

-313 |

|

-289 |

-314 |

-311 |

|

Equity shareholders' yield |

34.7% |

22.1% |

|

9.5% |

12.1% |

6.4% |

Underlying EBIT |

3,822 |

6,247 |

|

6,818 |

7,017 |

5,696 |

|

Cash conversion |

2.0x |

1.4x |

|

0.8x |

1.2x |

0.8x |

Income statement ratios |

|

|

|

|

|

|

|

Valuation |

|

|

|

|

$mn |

|

EBITDA margin |

26% |

31% |

|

32% |

35% |

31% |

|

SoTP DCF fair value and calculation of target price |

|

|

|

ZAR/sh |

||

EBIT margin |

17% |

22% |

|

23% |

25% |

20% |

|

Platinum |

|

|

|

|

8,224 |

91.3 |

EPS Growth |

169% |

49% |

|

2% |

4% |

-19% |

|

Diamonds |

|

|

|

|

7,262 |

80.6 |

Dividend payout ratio |

0% |

40% |

|

40% |

50% |

95% |

|

Coal |

|

|

|

|

6,535 |

72.5 |

Input assumptions |

|

|

|

|

|

|

|

Copper |

|

|

|

|

5,891 |

65.4 |

|

|

|

|

|

|

|

Nickel |

|

|

|

|

980 |

10.9 |

|

ZAR/$ |

14.70 |

13.31 |

|

13.24 |

14.31 |

14.14 |

|

Kumba Iron Ore |

|

|

|

|

4,197 |

46.6 |

Platinum, $/oz |

988 |

950 |

|

880 |

870 |

1,070 |

|

Samancor manganese |

|

|

|

|

3,560 |

39.5 |

Diamond realisations, $/ct |

188 |

162 |

|

171 |

171 |

181 |

|

Anglo Ferrous Brazil |

|

|

|

|

2,014 |

22.3 |

Copper, USc/lb |

221 |

280 |

|

296 |

272 |

289 |

|

Corporate & other |

|

|

|

|

-3,999 |

-44.4 |

Hard coking coal, $/t |

144 |

188 |

|

206 |

178 |

161 |

|

Total enterprise value excluding minority interests |

|

|

|

34,664 |

384.7 |

|

Iron ore fines (62%Fe, CIF China), $/t |

58 |

71 |

|

66 |

75 |

67 |

|

Attributable net debt as at 31 December 2017 |

|

|

|

-4,489 |

-49.8 |

|

|

|

|

|

|

|

|

|

Investments as at 31 December 2017 |

|

|

|

|

211 |

2.3 |

Required breakeven price |

|

|

|

|

|

|

|

Equity value as at 4/2/2019 |

|

|

|

|

30,386 |

337.2 |

Breakeven price - 3PGM, $/oz |

754 |

774 |

|

815 |

752 |

701 |

|

|

|

|

|

|

|

|

Rounded to |

|

|

|

|

|

340.0 |

||||||||

Breakeven price - copper, USc/lb |

198 |

216 |

|

203 |

208 |

228 |

|

Share price on 1/2/2019 |

|

|

|

|

|

345.2 |

Breakeven price - coking coal, $/t |

115 |

107 |

|

118 |

118 |

121 |

|

Expected share price return |

|

|

|

|

|

-1.5% |

Breakeven price - Export thermal coal, $/t |

46 |

59 |

|

61 |

64 |

74 |

|

Plus: expected dividend yield |

|

|

|

|

|

6.0% |

Sales volumes |

|

|

|

|

|

|

|

Total implied one-year return |

|

|

|

|

|

4.5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Platinum, koz |

2,416 |

2,505 |

|

2,424 |

2,050 |

2,000 |

|

Share price range, ZAR: |

|

|

|

|

|

|

Diamonds (consolidated sales), mn ct |

30.0 |

33.1 |

|

31.7 |

30.3 |

30.3 |

|

12-month high on 1/2/2019 |

347 |

12-month low on 4/4/2018 |

262 |

|||

Total iron ore, mnt |

59 |

61 |

|

46 |

62 |

65 |

|

Price move since high |

-0.5% |

Price move since low |

|

32.0% |

||

Total copper segment, kt |

577 |

579 |

|

668 |

663 |

653 |

|

|

|

|

|

|

|

|

Metallurgical coal, mnt |

20.7 |

19.8 |

|

22.0 |

22.0 |

22.0 |

|

Calculation of discount rate |

|

|

|

|

|

|

Export thermal coal, mnt |

34.1 |

31.0 |

|

30.0 |

28.3 |

30.1 |

|

|

|

|

|

|

|

|

Attributable Cu eq volumes, kt |

2,974 |

2,923 |

|

2,749 |

2,812 |

2,841 |

|

WACC |

9.5% |

Cost of debt |

|

|

5.0% |

|

Volume growth |

0.1% |

-1.7% |

|

-5.9% |

2.3% |

1.0% |

|

Risk-free rate |

4.0% |

Tax rate |

|

|

30% |

|

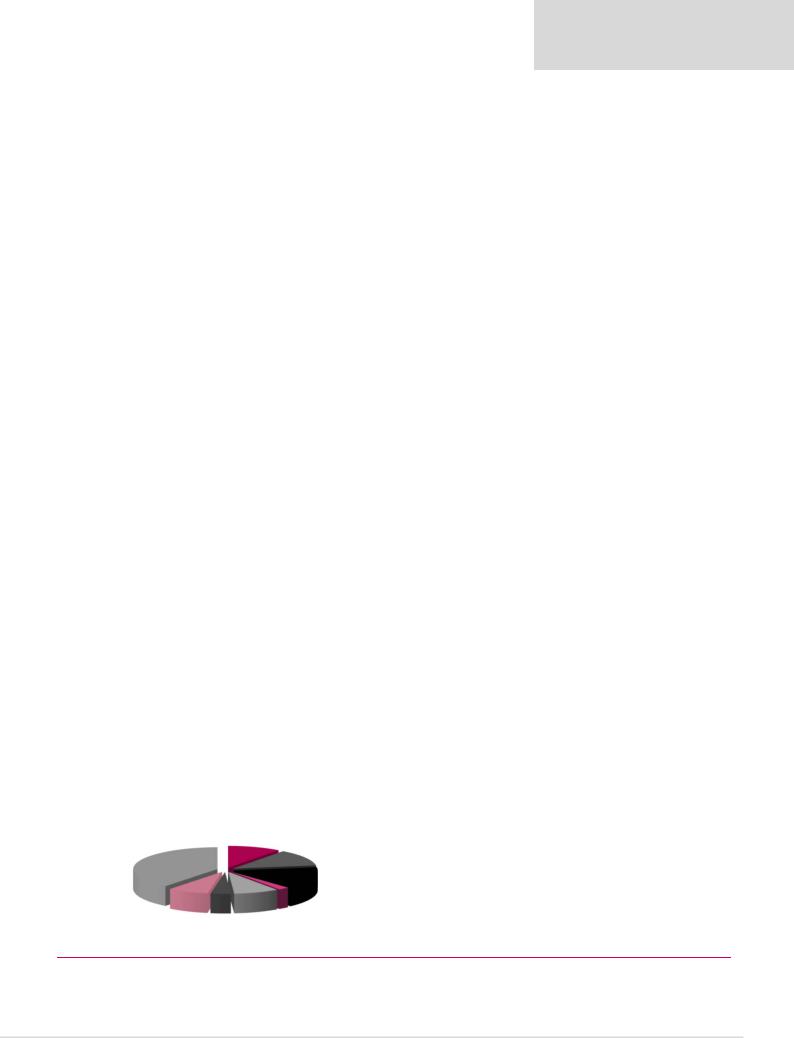

Contribution to FY18E attributable underlying EBITDA |

|

|

|

|

Equity risk premium |

5.0% |

After-tax cost of debt |

|

3.5% |

|||||

|

|

|

|

Beta |

1.30 |

Debt weighting |

|

15% |

||||||

|

|

Platinum (80% of |

|

|

|

|

Cost of equity |

10.5% |

Terminal growth rate |

|

3.0% |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

AMS) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10% |

|

|

Diamonds (85% of |

|

|

|

|

|

|

|

||

Coal |

|

|

|

|

De Beers) |

|

|

Valuation ratios |

|

|

|

|

|

|

39% |

|

|

|

|

12% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dec-YE |

2016 |

2017 |

|

2018E |

2019E |

2020E |

||

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

P/E multiple |

5.8x |

6.4x |

|

8.7x |

9.6x |

11.9x |

|

|

|

|

|

|

|

|

Dividend yield |

0.0% |

6.2% |

|

4.6% |

5.2% |

8.0% |

|

|

|

|

|

Copper |

|

|

EV/EBITDA |

4.8x |

4.1x |

|

4.6x |

4.6x |

5.3x |

|

|

|

|

Nickel |

16% |

|

|

P/B |

0.7x |

0.9x |

|

1.2x |

1.3x |

1.3x |

Samancor |

Minas Rio Kumba Iron Ore |

|

|

|

NAV per share, $ |

14.8 |

18.0 |

|

18.5 |

20.0 |

20.5 |

|||

Manganese |

2% |

|

|

|

NAV per share, ZAR |

217 |

240 |

|

245 |

285 |

289 |

|||

8% |

-4% |

(51%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9% |

|

|

|

|

|

|

|

|

|

|

|

|

* Gearing defined as net debt/(net debt +equity)

Source: Bloomberg, Thomson Reuters, Company data, Renaissance Capital estimates

46