vk.com/id446425943

Gold Fields – SELL

Renaissance Capital

6 February 2019

Metals & Mining

Figure 92: Gold Fields, $mn (unless otherwise noted) |

|

|

|

|

|

|

|

|

|

|

|

|

||||

Gold Fields |

|

|

|

GFIJ.J |

|

|

|

|

|

Target price, ZAR: |

|

|

43 |

|||

Market capitalisation, $mn: |

|

3,334 |

|

|

|

|

|

Share price, ZAR: |

|

|

54 |

|||||

Enterprise value, $mn: |

|

4,764 |

|

|

|

|

|

Potential 12-month return: |

|

-16.8% |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dec-YE |

|

|

|

2016 |

2017 |

2018E |

2019E |

2020E |

Dec-YE |

2016 |

2017 |

|

2018E |

2019E |

2020E |

|

Income statement |

|

|

|

|

|

|

|

Balance sheet |

|

|

|

|

|

|

||

Revenue |

|

|

|

2,749 |

2,811 |

2,552 |

2,988 |

3,051 |

|

Net operating assets |

4,449 |

4,711 |

|

4,461 |

4,342 |

4,159 |

EBITDA |

|

|

|

1,361 |

1,407 |

1,274 |

1,622 |

1,570 |

|

Investments, net of rehab provision |

-93 |

-6 |

|

-2 |

-2 |

-2 |

EBIT |

|

|

|

690 |

635 |

574 |

817 |

695 |

|

Equity |

3,067 |

3,276 |

|

2,811 |

3,103 |

3,281 |

Other items |

|

|

|

-247 |

-251 |

-257 |

-241 |

-231 |

|

Minority interest |

123 |

127 |

|

126 |

130 |

133 |

Net interest |

|

|

|

-51 |

-31 |

-4 |

-88 |

-84 |

|

Net debt |

1,166 |

1,303 |

|

1,523 |

1,107 |

744 |

Taxation |

|

|

|

-192 |

-172 |

81 |

-175 |

-143 |

|

Balance sheet ratios |

|

|

|

|

|

|

Minority interest in profit |

|

11 |

11 |

-3 |

-19 |

-18 |

|

|

|

|

|

|

|

|||

Net profit for the year |

|

185 |

-13 |

-294 |

319 |

241 |

|

Gearing (net debt/(net debt+equity)) |

27.5% |

28.4% |

|

35.1% |

26.3% |

18.5% |

||

Headline earnings |

|

208 |

194 |

139 |

319 |

241 |

|

Net debt to EBITDA |

0.9x |

0.9x |

|

1.2x |

0.7x |

0.5x |

||

Headline EPS, USc |

|

26 |

24 |

16 |

40 |

29 |

|

RoCE |

14.4% |

12.7% |

|

11.7% |

17.7% |

15.5% |

||

|

|

RoIC (after tax) |

11.0% |

9.7% |

|

12.1% |

13.3% |

11.7% |

||||||||

Thomson Reuters consensus HEPS, USc |

|

|

|

11 |

22 |

26 |

|

RoE |

7.1% |

6.1% |

|

4.6% |

10.8% |

7.6% |

||

DPS declared, USc |

|

8 |

7 |

4 |

13 |

10 |

|

Cash flow statement |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Underlying EBIT |

|

|

|

|

|

|

|

Operating cash flow |

1,332 |

1,150 |

|

1,239 |

1,417 |

1,429 |

||

South Africa Region |

|

15 |

-25 |

-58 |

33 |

24 |

|

Capex (net of disposals) |

-649 |

-834 |

|

-799 |

-638 |

-698 |

||

EBIT margin |

|

|

4% |

-7% |

-28% |

10% |

7% |

|

Other cash flows |

-492 |

-237 |

|

-602 |

-217 |

-186 |

|

West Africa Region |

|

227 |

221 |

204 |

263 |

245 |

|

Free cash flow |

191 |

79 |

|

-162 |

563 |

545 |

||

EBIT margin |

|

|

25% |

25% |

23% |

26% |

24% |

|

Equity shareholders' cash |

113 |

-36 |

|

-173 |

486 |

472 |

|

South America Region |

|

67 |

108 |

97 |

89 |

58 |

|

Dividends and share buy-backs |

101 |

-100 |

|

-48 |

-70 |

-108 |

||

EBIT margin |

|

|

21% |

27% |

27% |

23% |

19% |

|

Surplus (deficit) cash |

214 |

-136 |

|

-220 |

416 |

364 |

|

Australia Region |

|

382 |

332 |

331 |

432 |

368 |

|

Cash flow ratios |

|

|

|

|

|

|

||

EBIT margin |

|

|

32% |

28% |

30% |

34% |

27% |

|

|

|

|

|

|

|

||

Adjusted EBIT |

|

|

690 |

635 |

574 |

817 |

695 |

|

Working capital turnover, days |

-23 |

-8 |

|

-2 |

-1 |

-4 |

|

Income statement ratios |

|

|

|

|

|

|

|

FCF yield |

4.0% |

1.7% |

|

-3.6% |

12.4% |

13.0% |

||

|

|

|

|

|

|

|

Equity shareholders' yield |

3.2% |

-1.2% |

|

-6.1% |

14.7% |

14.2% |

|||

EBITDA margin |

|

49% |

50% |

50% |

54% |

51% |

|

Capex/EBITDA |

47.7% |

59.3% |

|

62.7% |

39.3% |

44.5% |

||

EBIT margin |

|

|

25% |

23% |

22% |

27% |

23% |

|

Cash conversion |

0.5x |

-0.2x |

|

-1.2x |

1.5x |

2.0x |

|

HEPS Growth |

|

|

750% |

-8% |

-33% |

150% |

-28% |

|

Valuation |

|

|

|

|

|

|

|

Dividend payout ratio |

|

29% |

28% |

26% |

33% |

33% |

|

|

|

|

|

$mn |

ZAR/sh |

|||

Input assumptions |

|

|

|

|

|

|

|

SoTP DCF fair value and calculation of target price |

|

|

|

|||||

|

|

|

|

|

|

|

South Africa Region |

|

|

|

|

591 |

10.3 |

|||

Gold, $/oz |

|

|

|

1,248 |

1,258 |

1,269 |

1,350 |

1,338 |

|

West Africa Region |

|

|

|

|

1,996 |

34.8 |

Copper, $/t |

|

|

|

4,867 |

6,170 |

6,532 |

6,000 |

6,367 |

|

South America Region |

|

|

|

|

933 |

16.3 |

ZAR/$ |

|

|

|

14.70 |

13.31 |

13.24 |

14.31 |

14.14 |

|

Australia Region |

|

|

|

|

2,379 |

41.5 |

AUD/$ |

|

|

|

1.34 |

1.30 |

1.34 |

1.38 |

1.28 |

|

Other |

|

|

|

|

-1,966 |

-34.3 |

PEN/$ |

|

|

|

3.38 |

3.26 |

3.29 |

3.40 |

3.32 |

|

Operating value |

|

|

|

|

3,932 |

68.5 |

|

|

|

|

|

|

|

|

|

|

Financial instruments and rehab provision as at 31 December 2017 |

|

-6 |

-0.1 |

|||

Gold production volumes, koz |

|

|

|

|

|

|

|

Enterprise value |

|

|

|

|

3,927 |

68.5 |

||

South Africa |

lumes |

|

290 |

281 |

155 |

244 |

268 |

|

Net debt as at 31 December 2017 |

|

|

|

|

-1,303 |

-22.7 |

|

West Africa |

lumes |

|

644 |

639 |

673 |

790 |

808 |

|

Minority interest |

|

|

|

|

-127 |

-2.4 |

|

South America |

lumes |

|

270 |

307 |

302 |

307 |

252 |

|

Cash used in share buy-backs during 2018E |

|

|

|

0 |

0.0 |

||

Australia |

lumes |

|

942 |

935 |

865 |

934 |

1,010 |

|

Equity value |

|

|

|

|

2,497 |

43.3 |

|

Total lumes |

|

|

2,147 |

2,162 |

1,995 |

2,276 |

2,338 |

|

|

|

|

|

|

|

|

|

|

|

Rounded to |

|

|

|

|

|

43.0 |

||||||||

Volume growth |

|

|

-0.6% |

0.7% |

-7.7% |

14.0% |

2.7% |

|

Share price on 1/2/2019 |

|

|

|

|

|

53.8 |

|

Calculated breakeven price, $/oz |

|

|

|

|

|

|

|

Expected share price return |

|

|

|

|

|

-20.0% |

||

|

|

|

|

|

|

|

Plus: expected dividend yield |

|

|

|

|

|

3.2% |

|||

South Africa breakeven |

|

1,192 |

1,342 |

1,763 |

1,126 |

1,155 |

|

Total implied one-year return |

|

|

|

|

|

-16.8% |

||

West Africa breakeven |

|

939 |

885 |

852 |

870 |

886 |

|

|

|

|

|

|

|

|

||

South America breakeven |

|

715 |

611 |

777 |

862 |

907 |

|

Share price range, ZAR: |

|

|

|

|

|

|

||

Australia breakeven |

|

886 |

902 |

857 |

814 |

892 |

|

12-month high on 30-1-2019 |

55 |

12-month low on 11-9-2018 |

33 |

|||||

Group breakeven |

|

1,028 |

1,012 |

1,025 |

968 |

1,012 |

|

Price move since high |

-1.7% |

Price move since low |

|

63.4% |

||||

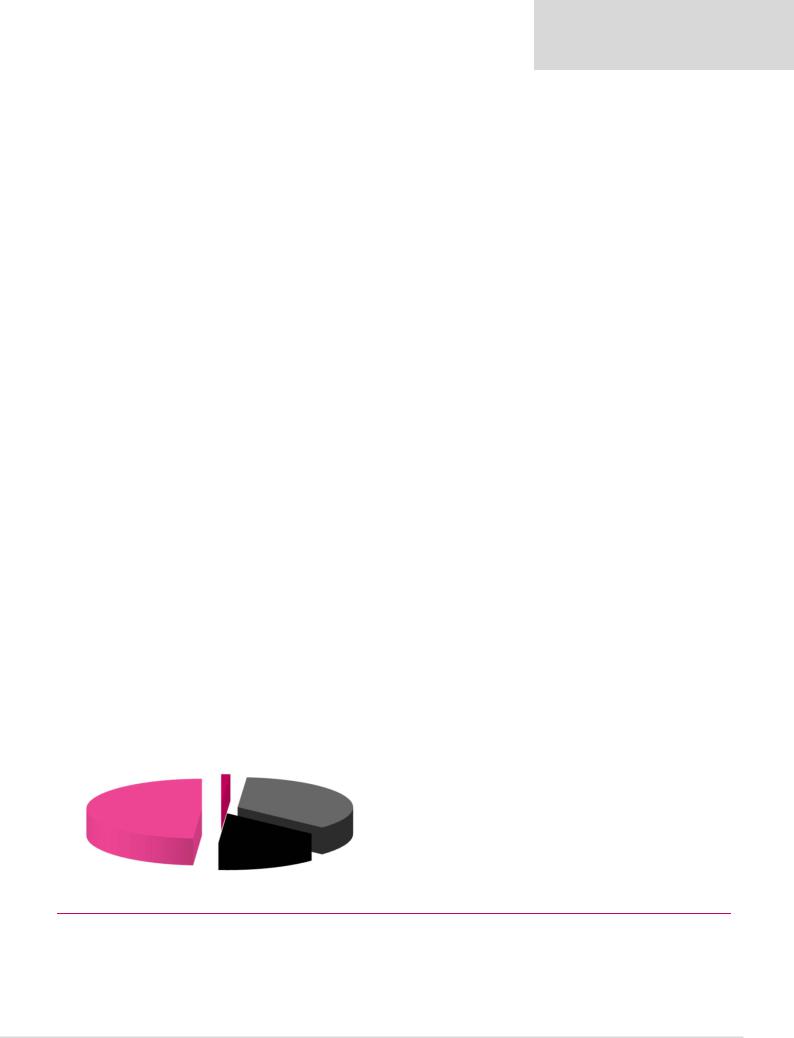

Contribution to FY18E underlying EBITDA |

|

|

|

|

|

|

Calculation of WACC |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

WACC |

7.4% |

Cost of debt |

|

|

5.0% |

|

|

|

|

|

South Africa |

|

|

|

|

Risk-free rate |

4.0% |

Tax rate |

|

|

30% |

||

|

|

|

|

-1% |

|

|

|

|

|

Equity risk premium |

5.0% |

After-tax cost of debt |

|

1.1% |

||

|

|

|

|

|

|

|

|

|

|

Beta |

1.00 |

Debt weighting |

|

30% |

||

|

|

|

|

|

|

|

|

West Africa |

Cost of equity |

9.0% |

Terminal growth rate |

|

2.0% |

|||

Australia |

|

|

|

|

|

|

|

36% |

|

Valuation ratios |

|

|

|

|

|

|

49% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dec-YE, $mn |

2016 |

2017 |

|

2018E |

2019E |

2020E |

|

|

|

|

|

|

|

|

|

|

P/E multiple |

16.5x |

15.8x |

|

21.4x |

10.1x |

13.9x |

|

|

|

|

|

|

|

|

|

|

Dividend yield |

1.8% |

1.8% |

|

1.2% |

3.3% |

2.4% |

|

|

|

|

|

|

|

|

|

|

EV/EBITDA |

3.5x |

3.2x |

|

3.5x |

2.8x |

2.7x |

|

|

|

|

|

|

|

|

|

|

P/B |

1.1x |

0.9x |

|

1.0x |

1.1x |

1.0x |

|

|

|

|

|

|

South America |

|

|

|

NAV per share, $ |

3.7 |

4.0 |

|

3.4 |

3.8 |

4.0 |

|

|

|

|

|

|

14% |

|

|

|

NAV per share, ZAR |

55 |

53 |

|

45 |

54 |

57 |

Source: Bloomberg, Thomson Reuters, Renaissance Capital estimates

59