vk.com/id446425943

Gold Fields – SELL

Renaissance Capital

14 January 2019

Metals & Mining

Figure 104: Gold Fields, $mn (unless otherwise stated)

|

|

|

|

Gold Fields |

GFIJ.J |

Target price, ZAR: |

43 |

Market capitalisation, $mn: |

2,982 |

Share price, ZAR: |

51 |

Enterprise value, $mn: |

4,412 |

Potential 12-month return: |

-11.6% |

Dec-YE |

|

|

2016 |

2017 |

2018E |

2019E |

2020E |

Income statement |

|

|

|

|

|

||

Revenue |

|

|

2,749 |

2,811 |

2,552 |

2,988 |

3,051 |

EBITDA |

|

|

1,361 |

1,407 |

1,274 |

1,622 |

1,570 |

EBIT |

|

|

690 |

635 |

574 |

817 |

695 |

Other items |

|

|

-247 |

-251 |

-257 |

-241 |

-231 |

Net interest |

|

|

-51 |

-31 |

-4 |

-88 |

-84 |

Taxation |

|

|

-192 |

-172 |

81 |

-175 |

-143 |

Minority interest in profit |

11 |

11 |

-3 |

-19 |

-18 |

||

Net profit for the year |

185 |

-13 |

-294 |

319 |

241 |

||

Headline earnings |

208 |

194 |

139 |

319 |

241 |

||

Headline EPS, USc |

26 |

24 |

16 |

40 |

29 |

||

Thomson Reuters consensus HEPS, USc |

|

|

11 |

19 |

22 |

||

DPS declared, USc |

8 |

7 |

4 |

13 |

10 |

||

Underlying EBIT |

15 |

-25 |

-58 |

33 |

24 |

||

South Africa Region |

|||||||

EBIT margin |

|

4% |

-7% |

-28% |

10% |

7% |

|

West Africa Region |

227 |

221 |

204 |

263 |

245 |

||

EBIT margin |

|

25% |

25% |

23% |

26% |

24% |

|

South America Region |

67 |

108 |

97 |

89 |

58 |

||

EBIT margin |

|

21% |

27% |

27% |

23% |

19% |

|

Australia Region |

382 |

332 |

331 |

432 |

368 |

||

EBIT margin |

|

32% |

28% |

30% |

34% |

27% |

|

Adjusted EBIT |

690 |

635 |

574 |

817 |

695 |

||

Income statement ratios |

|

|

|

|

|

||

EBITDA margin |

49% |

50% |

50% |

54% |

51% |

||

EBIT margin |

|

25% |

23% |

22% |

27% |

23% |

|

HEPS Growth |

|

750% |

-8% |

-33% |

150% |

-28% |

|

Dividend payout ratio |

29% |

28% |

26% |

33% |

33% |

||

Input assumptions |

|

|

|

|

|

||

Gold, $/oz |

|

|

1,248 |

1,258 |

1,269 |

1,350 |

1,338 |

Copper, $/t |

|

|

4,867 |

6,170 |

6,532 |

6,000 |

6,367 |

ZAR/$ |

|

|

14.70 |

13.31 |

13.24 |

14.31 |

14.14 |

AUD/$ |

|

|

1.34 |

1.30 |

1.34 |

1.38 |

1.28 |

PEN/$ |

|

|

3.38 |

3.26 |

3.29 |

3.40 |

3.32 |

Gold production volumes, koz |

|

|

|

|

|

||

South Africa |

lumes |

290 |

281 |

155 |

244 |

268 |

|

West Africa |

lumes |

644 |

639 |

673 |

790 |

808 |

|

South America |

lumes |

270 |

307 |

302 |

307 |

252 |

|

Australia |

lumes |

942 |

935 |

865 |

934 |

1,010 |

|

Total lumes |

2,147 |

2,162 |

1,995 |

2,276 |

2,338 |

||

Volume growth |

|

-0.6% |

0.7% |

-7.7% |

14.0% |

2.7% |

|

Calculated breakeven price, $/oz |

|

|

|

|

|

||

South Africa breakeven |

1,192 |

1,342 |

1,763 |

1,126 |

1,155 |

||

West Africa breakeven |

939 |

885 |

852 |

870 |

886 |

||

South America breakeven |

715 |

611 |

777 |

862 |

907 |

||

Australia breakeven |

886 |

902 |

857 |

814 |

892 |

||

Group breakeven |

1,028 |

1,012 |

1,025 |

968 |

1,012 |

||

|

|

|

|

|

|

|

|

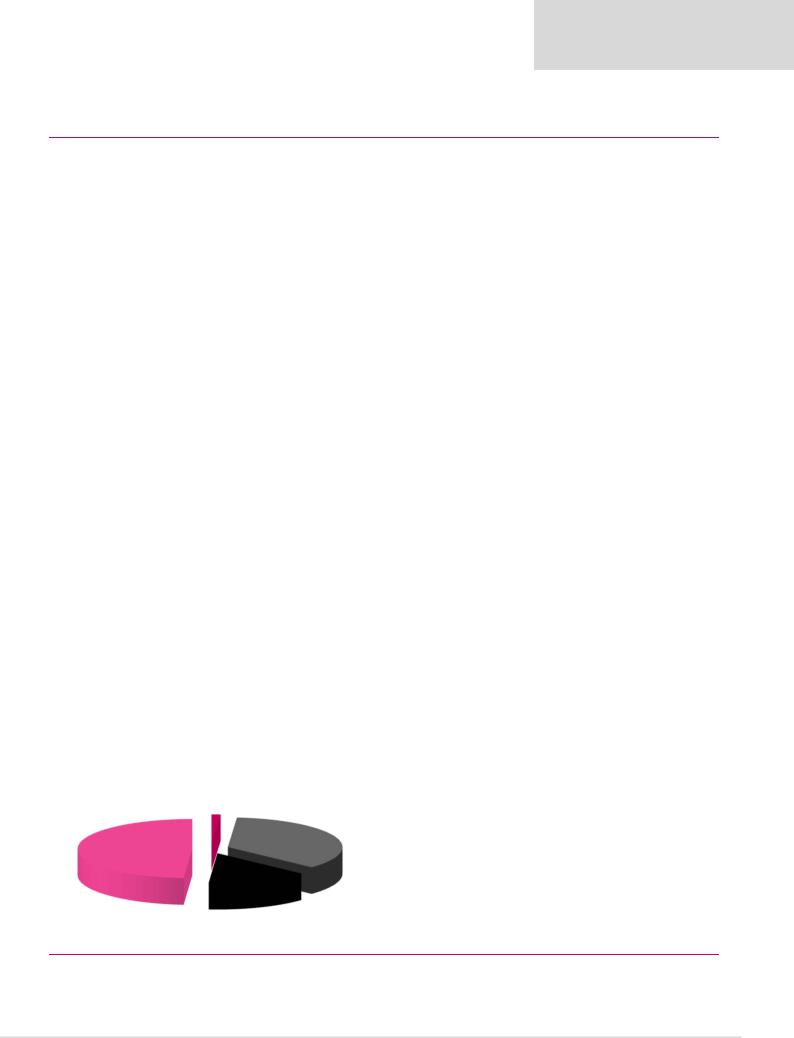

Contribution to FY18E underlying EBITDA

South Africa

-1%

West Africa

Australia 36%

49%

South America

14%

Dec-YE |

|

2016 |

2017 |

|

2018E |

2019E |

2020E |

Balance sheet |

|

|

|

|

|

|

|

Net operating assets |

|

4,449 |

4,711 |

|

4,461 |

4,342 |

4,159 |

Investments, net of rehab provision |

|

-93 |

-6 |

|

-2 |

-2 |

-2 |

Equity |

|

3,067 |

3,276 |

|

2,811 |

3,103 |

3,281 |

Minority interest |

|

123 |

127 |

|

126 |

130 |

133 |

Net debt |

|

1,166 |

1,303 |

|

1,523 |

1,107 |

744 |

Balance sheet ratios |

|

|

|

|

|

|

|

Gearing (net debt/(net debt+equity)) |

|

27.5% |

28.4% |

|

35.1% |

26.3% |

18.5% |

Net debt to EBITDA |

|

0.9x |

0.9x |

|

1.2x |

0.7x |

0.5x |

RoCE |

|

14.4% |

12.7% |

|

11.7% |

17.7% |

15.5% |

RoIC (after tax) |

|

11.0% |

9.7% |

|

12.1% |

13.3% |

11.7% |

RoE |

|

7.1% |

6.1% |

|

4.6% |

10.8% |

7.6% |

Cash flow statement |

|

|

|

|

|

|

|

Operating cash flow |

|

1,332 |

1,150 |

|

1,239 |

1,417 |

1,429 |

Capex (net of disposals) |

|

-649 |

-834 |

|

-799 |

-638 |

-698 |

Other cash flows |

|

-492 |

-237 |

|

-602 |

-217 |

-186 |

Free cash flow |

|

191 |

79 |

|

-162 |

563 |

545 |

Equity shareholders' cash |

|

113 |

-36 |

|

-173 |

486 |

472 |

Dividends and share buy-backs |

|

101 |

-100 |

|

-48 |

-70 |

-108 |

Surplus (deficit) cash |

|

214 |

-136 |

|

-220 |

416 |

364 |

Cash flow ratios |

|

-23 |

-8 |

|

-2 |

-1 |

-4 |

Working capital turnover, days |

|

|

|||||

FCF yield |

|

4.0% |

1.7% |

|

-3.6% |

13.3% |

14.1% |

Equity shareholders' yield |

|

3.2% |

-1.2% |

|

-6.1% |

16.2% |

15.7% |

Capex/EBITDA |

|

47.7% |

59.3% |

|

62.7% |

39.3% |

44.5% |

Cash conversion |

|

0.5x |

-0.2x |

|

-1.2x |

1.5x |

2.0x |

Valuation |

|

|

|

|

|

|

|

SoTP DCF fair value and calculation of target price |

|

$mn |

ZAR/sh |

||||

South Africa Region |

|

|

|

|

587 |

10.2 |

|

West Africa Region |

|

|

|

|

1,983 |

34.6 |

|

South America Region |

|

|

|

|

927 |

16.2 |

|

Australia Region |

|

|

|

|

2,364 |

41.2 |

|

Other |

|

|

|

|

-1,953 |

-34.0 |

|

Operating value |

|

|

|

|

3,908 |

68.1 |

|

Financial instruments and rehab provision as at 31 December 2017 |

|

-6 |

-0.1 |

||||

Enterprise value |

|

|

|

|

3,902 |

68.0 |

|

Net debt as at 31 December 2017 |

|

|

|

|

-1,303 |

-22.7 |

|

Minority interest |

|

|

|

|

-127 |

-2.2 |

|

Cash used in share buy-backs during 2018E |

|

|

|

|

0 |

0.0 |

|

Equity value |

|

|

|

|

2,472 |

43.1 |

|

Rounded to |

|

|

|

|

|

43.0 |

|

Share price on 7/1/2019 |

|

|

|

|

|

50.7 |

|

Expected share price return |

|

|

|

|

|

-15.1% |

|

Plus: expected dividend yield |

|

|

|

|

|

3.5% |

|

Total implied one-year return |

|

|

|

|

|

-11.6% |

|

Share price range, ZAR: |

|

|

|

|

|

|

|

12-month high on 15-1-2018 |

56 |

12-month low on 11-9-2018 |

33 |

||||

Price move since high |

-10.3% Price move since low |

|

54.0% |

||||

Calculation of WACC |

|

|

|

|

|

|

|

WACC |

7.4% |

Cost of debt |

|

|

5.0% |

||

Risk-free rate |

4.0% |

Tax rate |

|

|

30% |

||

Equity risk premium |

5.0% After-tax cost of debt |

|

1.1% |

||||

Beta |

1.00 |

Debt weighting |

|

30% |

|||

Cost of equity |

9.0% |

Terminal growth rate |

|

2.0% |

|||

Valuation ratios |

|

|

|

|

|

|

|

Dec-YE, $mn |

|

2016 |

2017 |

|

2018E |

2019E |

2020E |

P/E multiple |

|

16.5x |

15.8x |

|

21.4x |

9.1x |

12.6x |

Dividend yield |

|

1.8% |

1.8% |

|

1.2% |

3.6% |

2.6% |

EV/EBITDA |

|

3.5x |

3.2x |

|

3.5x |

2.6x |

2.5x |

P/B |

|

1.1x |

0.9x |

|

1.0x |

1.0x |

0.9x |

NAV per share, $ |

|

3.7 |

4.0 |

|

3.4 |

3.8 |

4.0 |

NAV per share, ZAR |

|

55 |

53 |

|

45 |

54 |

57 |

Source: Bloomberg, Thomson Reuters, Renaissance Capital estimates

69

vk.com/id446425943

Harmony Gold – SELL

Renaissance Capital

14 January 2019

Metals & Mining

Figure 105: Harmony Gold, ZARmn (unless otherwise stated) |

|

|

|

|

|

|

|

|

|

|

|||||

Harmony |

|

|

|

HARJ.J |

|

|

|

|

|

Target price, ZAR: |

|

|

21 |

||

Market capitalisation, ZARmn: |

|

13,893 |

|

|

|

|

|

Share price, ZAR: |

|

|

27 |

||||

Enterprise value, ZARmn: |

|

18,801 |

|

|

|

|

|

Potential 12-month return: |

|

-18.9% |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Jun-YE |

|

|

|

2017 |

2018 |

2019E |

2020E |

2021E |

Jun-YE |

2017 |

2018 |

2019E |

2020E |

2021E |

|

Income statement |

|

|

|

|

|

|

|

Balance sheet |

|

|

|

|

|

||

Revenue |

|

|

19,264 |

20,358 |

26,675 |

27,616 |

25,701 |

|

Net operating assets |

28,225 |

29,794 |

31,772 |

32,825 |

33,118 |

|

Underlying EBITDA |

|

4,452 |

5,356 |

8,641 |

9,646 |

7,543 |

|

Investments, net of rehab provision |

1,953 |

496 |

496 |

496 |

496 |

||

Underlying EBIT |

|

1,933 |

2,786 |

5,618 |

6,667 |

4,571 |

|

Equity |

29,291 |

25,382 |

28,286 |

31,493 |

33,436 |

||

Other items |

|

|

-2,292 |

-6,862 |

-1,271 |

-1,383 |

-1,363 |

|

Minority interest |

0 |

0 |

0 |

0 |

0 |

|

Net interest |

|

|

233 |

-669 |

-468 |

-335 |

-147 |

|

Net debt |

887 |

4,908 |

3,982 |

1,827 |

178 |

|

Taxation |

|

|

|

510 |

234 |

-1,018 |

-1,443 |

-918 |

|

|

|

|

|

|

|

Net profit for the year |

362 |

-4,473 |

2,861 |

3,506 |

2,143 |

|

Balance sheet ratios |

|

|

|

|

|

|||

Headline earnings |

|

1,306 |

763 |

2,861 |

3,506 |

2,143 |

|

Gearing (net debt/(net debt+equity)) |

2.9% |

16.2% |

12.3% |

5.5% |

0.5% |

||

Headline EPS, ZAR |

|

2.98 |

1.71 |

5.72 |

7.01 |

4.28 |

|

Net debt to EBITDA |

0.2x |

0.9x |

0.5x |

0.2x |

0.0x |

||

|

|

RoCE |

6.3% |

8.9% |

17.0% |

19.2% |

12.8% |

||||||||

Thomson Reuters consensus HEPS, ZAR |

|

|

3.06 |

3.87 |

2.97 |

|

RoIC (after tax) |

8.8% |

7.3% |

14.3% |

15.5% |

10.5% |

|||

DPS declared, ZAR |

|

0.85 |

0.35 |

0.82 |

1.05 |

0.65 |

|

RoE |

4.5% |

2.8% |

10.7% |

11.7% |

6.6% |

||

Production EBIT |

|

|

|

|

|

|

|

Cash flow statement |

|

|

|

|

|

||

South Africa underground |

1,768 |

2,432 |

3,585 |

4,866 |

2,995 |

|

Operating cash flow |

5,224 |

4,811 |

7,637 |

8,382 |

6,803 |

|||

EBIT margin |

|

|

11% |

14% |

18% |

22% |

15% |

|

Capex (net of disposals) |

-3,887 |

-4,571 |

-5,146 |

-4,304 |

-3,485 |

|

South Africa Surface |

|

174 |

235 |

284 |

347 |

200 |

|

Other cash flows |

317 |

-5,930 |

-1,053 |

-1,165 |

-1,144 |

||

EBIT margin |

|

|

10% |

12% |

13% |

18% |

11% |

|

Free cash flow |

1,654 |

-5,690 |

1,438 |

2,913 |

2,174 |

|

Hidden Valley |

|

-9 |

119 |

1,288 |

1,442 |

1,377 |

|

Equity shareholders' cash |

635 |

-4,714 |

1,101 |

2,671 |

2,068 |

||

EBIT margin |

|

|

-1% |

29% |

35% |

41% |

41% |

|

Dividends and share buy-backs |

-439 |

693 |

-175 |

-516 |

-419 |

|

Group production EBIT |

1,933 |

2,786 |

5,618 |

6,667 |

4,571 |

|

Surplus (deficit) cash |

196 |

-4,021 |

926 |

2,155 |

1,649 |

|||

Income statement ratios |

|

|

|

|

|

|

Cash flow ratios |

|

|

|

|

|

|||

EBITDA margin |

|

23% |

26% |

32% |

35% |

29% |

|

Working capital turnover, days |

3 |

4 |

5 |

4 |

3 |

||

EBIT margin |

|

|

10% |

14% |

21% |

24% |

18% |

|

FCF yield |

9.3% |

-34.1% |

8.2% |

19.0% |

15.9% |

|

HEPS Growth |

|

35% |

-43% |

235% |

23% |

-39% |

|

Equity shareholders' yield |

3.7% |

-40.0% |

8.1% |

19.7% |

15.3% |

||

Dividend payout ratio |

29% |

20% |

14% |

15% |

15% |

|

Capex/EBITDA |

87.3% |

85.3% |

59.6% |

44.6% |

46.2% |

|||

Input assumptions |

|

|

|

|

|

|

|

Cash conversion |

0.5x |

-6.2x |

0.4x |

0.8x |

1.0x |

||

|

|

|

|

|

|

|

Valuation |

|

|

|

|

|

|||

Gold, $/oz |

|

|

1,257 |

1,298 |

1,273 |

1,369 |

1,309 |

|

|

|

|

|

|

||

$/ZAR |

|

|

|

13.60 |

12.85 |

14.25 |

14.25 |

14.09 |

|

SoTP DCF fair value and calculation of target price |

|

|

ZARmn |

ZAR/sh |

|

Calculated breakeven price, $/oz |

|

|

|

|

|

|

Kusasalethu |

|

|

|

540 |

1.1 |

|||

|

|

|

|

|

|

Doornkop |

|

|

|

720 |

1.4 |

||||

South Africa breakeven |

1,097 |

1,117 |

1,061 |

1,086 |

1,111 |

|

Tshepong/Phakisa |

|

|

|

4,263 |

8.5 |

|||

International breakeven |

1,168 |

1,105 |

897 |

828 |

667 |

|

Masimong |

|

|

|

444 |

0.9 |

|||

Group breakeven |

|

1,193 |

1,208 |

1,084 |

1,120 |

1,123 |

|

Target 1 |

|

|

|

327 |

0.7 |

||

Gold production volumes, koz |

|

|

|

|

|

|

Bambanani |

|

|

|

1,659 |

3.3 |

|||

|

|

|

|

|

|

Joel |

|

|

|

379 |

0.8 |

||||

Kusasalethu |

lumes |

141 |

142 |

156 |

156 |

156 |

|

Unisel |

|

|

|

73 |

0.1 |

||

Doornkop |

lumes |

|

86 |

110 |

107 |

88 |

88 |

|

Moab |

|

|

|

5,645 |

11.3 |

|

Tshepong/Phakisa lumes |

284 |

302 |

287 |

290 |

290 |

|

Surface |

|

|

|

2,203 |

4.4 |

|||

Masimong |

lumes |

|

82 |

84 |

73 |

74 |

74 |

|

Hidden Valley |

|

|

|

2,247 |

4.5 |

|

Target 1 |

lumes |

|

86 |

92 |

87 |

100 |

100 |

|

Other |

|

|

|

-6,467 |

-12.9 |

|

Bambanani |

lumes |

|

88 |

91 |

82 |

84 |

84 |

|

Operating value |

|

|

|

12,033 |

24.1 |

|

Joel lumes |

|

72 |

53 |

50 |

72 |

72 |

|

Financial instruments and rehab provision as at 30 June 2018 |

|

496 |

1.0 |

||||

Unisel |

lumes |

|

51 |

41 |

32 |

21 |

0 |

|

Enterprise value |

|

|

|

12,529 |

25.0 |

|

Moab |

lumes |

|

0 |

106 |

248 |

250 |

250 |

|

Net debt as at 30 June 2018 |

|

|

|

-4,908 |

-9.8 |

|

Surface |

lumes |

|

102 |

115 |

124 |

100 |

100 |

|

Minority interest |

|

|

|

0 |

0.0 |

|

South Africa Total |

lumes |

993 |

1,136 |

1,244 |

1,235 |

1,214 |

|

50% Golpu value assuming it trades at avg. replacement cost |

|

2,814 |

5.6 |

||||

Hidden Valley lumes |

84 |

26 |

202 |

180 |

180 |

|

Cash used in share buy-backs during 2019E |

|

|

0 |

0.0 |

||||

International total |

lumes |

84 |

26 |

202 |

180 |

180 |

|

Equity value |

|

|

|

10,435 |

20.9 |

||

Total production |

lumes |

1,076 |

1,161 |

1,445 |

1,415 |

1,394 |

|

|

|

|

|

|

|

||

Rounded to |

|

|

|

|

21.0 |

||||||||||

Attributable Cu eq volumes, kt |

214 |

230 |

287 |

281 |

277 |

|

Share price on 7/1/2019 |

|

|

|

|

27.1 |

|||

Volume growth |

|

-0.5% |

7.9% |

24.5% |

-2.1% |

-1.5% |

|

Expected share price return |

|

|

|

|

-22.4% |

||

|

|

|

|

|

|

|

|

|

|

Plus: expected dividend yield |

|

|

|

|

3.5% |

Contribution to FY19E mining EBITDA |

|

|

|

|

|

|

Total implied one-year return |

|

|

|

|

-18.9% |

|||

Share price range, ZAR:

|

Kusasalethu |

|

||

Hidden Valley |

|

7% |

Doornkop |

|

|

|

6% |

|

|

22% |

|

|

|

|

|

|

|

Tshepong/Phakisa |

|

|

|

|

|

|

|

|

|

|

18% |

Surface |

|

|

|

|

6% |

|

|

|

Masimong |

|

|

|

|

|

|

|

|

|

4% |

Moab |

|

|

Bambanani |

Target 1 |

Unisel |

Joel |

3% |

||

25% |

8% |

|

||

|

1% |

0% |

|

|

12-month high on 16-10-2018 |

32 |

12-month low on 30-1-2018 |

19 |

|||

Price move since high |

-14.1% |

Price move since low |

|

42.4% |

||

Calculation of WACC |

|

|

|

|

|

|

WACC |

13.0% |

Cost of debt |

|

|

10.0% |

|

Risk-free rate |

9.0% |

Tax rate |

|

|

28% |

|

Equity risk premium |

5.0% |

After-tax cost of debt |

|

1.1% |

||

Beta |

1.00 |

Debt weighting |

|

15% |

||

Cost of equity |

14.0% |

Terminal growth rate |

|

6.0% |

||

Valuation ratios |

|

|

|

|

|

|

Dec-YE, $mn |

2017 |

2018 |

|

2019E |

2020E |

2021E |

P/E multiple |

12.9x |

13.8x |

|

4.7x |

3.9x |

6.3x |

Dividend yield |

2.2% |

1.5% |

|

3.0% |

3.9% |

2.4% |

EV/EBITDA |

4.0x |

3.1x |

|

2.0x |

1.6x |

1.8x |

P/B |

0.6x |

0.5x |

|

0.5x |

0.4x |

0.4x |

NAV per share, ZAR |

66.6 |

50.7 |

|

56.5 |

63.0 |

66.8 |

Source: Bloomberg, Thomson Reuters, Renaissance Capital estimates

70

vk.com/id446425943

Polymetal – HOLD

Renaissance Capital

14 January 2019

Metals & Mining

Figure 106: Polymetal, $mn (unless otherwise stated) |

|

|

|

|

|

|

|

|

|

|

|

|||||||

Polymetal |

|

|

|

|

POLYP.L |

|

|

|

|

|

Target price, GBP: |

|

|

8.60 |

||||

Market capitalisation, $mn: |

|

|

|

5,175 |

|

|

|

|

|

|

Share price, GBP: |

|

|

8.66 |

||||

Enterprise value, $mn: |

|

|

|

6,595 |

|

|

|

|

|

|

Potential 12-month return: |

|

5.9% |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dec-YE |

|

|

|

|

2016 |

2017 |

|

2018E |

2019E |

2020E |

Dec-YE |

2016 |

2017 |

|

2018E |

2019E |

2020E |

|

Income statement |

|

|

|

|

|

|

|

|

|

|

Balance sheet |

|

|

|

|

|

|

|

Revenue |

|

|

|

1,583 |

1,815 |

|

1,914 |

2,148 |

2,181 |

|

Net operating assets |

2,424 |

2,828 |

|

3,085 |

3,214 |

3,445 |

|

EBITDA |

|

|

|

|

759 |

745 |

|

788 |

1,094 |

1,105 |

|

Investments, net of rehab provision |

-113 |

-101 |

|

-99 |

-99 |

-99 |

EBIT |

|

|

|

|

604 |

531 |

|

601 |

920 |

925 |

|

Equity |

981 |

1,307 |

|

1,545 |

1,956 |

2,270 |

Net interest |

|

|

|

-17 |

-67 |

|

-60 |

-60 |

-51 |

|

Minority interest |

0 |

0 |

|

0 |

0 |

0 |

|

Taxation |

|

|

|

|

-169 |

-89 |

|

-103 |

-172 |

-175 |

|

Net debt |

1,330 |

1,420 |

|

1,442 |

1,159 |

1,076 |

Minority interest in profit |

|

|

0 |

0 |

|

0 |

0 |

0 |

|

|

|

|

|

|

|

|

||

Net profit for the year |

|

|

395 |

354 |

|

446 |

688 |

699 |

|

Balance sheet ratios |

|

|

|

|

|

|

||

Underlying earnings |

|

|

382 |

376 |

|

426 |

688 |

699 |

|

Gearing (net debt/(net debt+equity)) |

57.6% |

52.1% |

|

48.3% |

37.2% |

32.2% |

||

Underlying EPS, USc |

|

|

90 |

88 |

|

94 |

147 |

149 |

|

Net debt to EBITDA |

1.8x |

1.9x |

|

1.8x |

1.1x |

1.0x |

||

|

|

|

|

RoCE |

28.1% |

20.0% |

|

20.1% |

28.7% |

27.3% |

||||||||

Consensus EPS, USc |

|

|

|

|

|

90 |

108 |

120 |

|

RoIC (after tax) |

21.2% |

15.9% |

|

17.5% |

23.0% |

22.0% |

||

DPS declared, USc |

|

|

|

42 |

44 |

|

47 |

74 |

75 |

|

RoE |

52.1% |

32.9% |

|

29.9% |

39.3% |

33.1% |

|

Consensus DPS, USc |

|

|

|

|

|

44 |

52 |

61 |

|

Cash flow statement |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Adjusted EBIT |

|

|

|

|

|

|

|

|

|

|

Operating cash flow |

490 |

574 |

|

687 |

927 |

929 |

|

Voro |

|

|

|

|

102 |

85 |

|

73 |

64 |

62 |

|

Capex (net of disposals) |

-288 |

-432 |

|

-365 |

-380 |

-420 |

EBIT margin |

|

|

|

65% |

55% |

|

57% |

59% |

58% |

|

Other cash flows |

-116 |

-29 |

|

-87 |

60 |

0 |

|

Okhotsk operations |

|

|

|

78 |

138 |

|

152 |

118 |

114 |

|

Free cash flow |

86 |

114 |

|

236 |

607 |

509 |

|

EBIT margin |

|

|

|

44% |

49% |

|

55% |

58% |

56% |

|

Equity shareholders' cash |

126 |

48 |

|

184 |

560 |

468 |

|

Dukat |

|

|

|

|

246 |

141 |

|

112 |

149 |

166 |

|

Dividends and share buy-backs |

-158 |

-138 |

|

-206 |

-277 |

-385 |

EBIT margin |

|

|

|

49% |

35% |

|

31% |

39% |

41% |

|

Surplus (deficit) cash |

-32 |

-90 |

|

-22 |

283 |

83 |

|

Omolon |

|

|

|

|

96 |

93 |

|

75 |

109 |

107 |

|

Cash flow ratios |

|

|

|

|

|

|

EBIT margin |

|

|

|

46% |

35% |

|

35% |

42% |

41% |

|

115 |

109 |

|

108 |

94 |

92 |

||

Varvara |

|

|

|

|

25 |

39 |

|

62 |

87 |

78 |

|

Working capital turnover, days |

|

|||||

EBIT margin |

|

|

|

25% |

25% |

|

34% |

42% |

37% |

|

FCF yield |

1.4% |

1.7% |

|

3.9% |

9.6% |

8.1% |

|

Amursk-Albazino |

|

|

|

130 |

113 |

|

156 |

157 |

148 |

|

Equity shareholders' yield |

2.6% |

0.9% |

|

4.1% |

10.8% |

9.0% |

|

EBIT margin |

|

|

|

44% |

32% |

|

37% |

42% |

40% |

|

Capex/EBITDA |

37.9% |

58.0% |

|

46.3% |

34.7% |

38.0% |

|

Other |

|

|

|

|

-73 |

-77 |

|

-29 |

235 |

251 |

|

Cash conversion |

0.3x |

0.1x |

|

0.4x |

0.8x |

0.7x |

Adjusted EBIT |

|

|

|

604 |

531 |

|

601 |

920 |

925 |

|

Valuation |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Income statement ratios |

|

|

|

|

|

|

|

|

|

SoTP DCF fair value and calculation of target price |

|

|

|

$mn |

GBP/sh |

|||

EBITDA margin |

|

|

|

48% |

41% |

|

41% |

51% |

51% |

|

Voro |

|

|

|

|

331 |

0.55 |

|

EBIT margin |

|

|

|

38% |

29% |

|

31% |

43% |

42% |

|

Okhotsk operations |

|

|

|

|

612 |

1.01 |

|

Underlying EPS Growth |

|

|

28% |

-2% |

|

7% |

56% |

1% |

|

Dukat |

|

|

|

|

998 |

1.65 |

||

Dividend payout ratio |

|

|

47% |

50% |

|

50% |

50% |

50% |

|

Omolon |

|

|

|

|

628 |

1.04 |

||

Input assumptions |

|

|

|

|

|

|

|

|

|

|

Varvara |

|

|

|

|

900 |

1.49 |

|

|

|

|

|

|

|

|

|

|

|

Amursk-Albazino |

|

|

|

|

705 |

1.17 |

||

Gold, $/oz |

|

|

|

1,248 |

1,258 |

|

1,269 |

1,350 |

1,338 |

|

Armenia |

|

|

|

|

-4 |

-0.01 |

|

Silver, $/oz |

|

|

|

17.1 |

17.1 |

|

15.7 |

16.7 |

17.8 |

|

Mayskoye |

|

|

|

|

237 |

0.39 |

|

$/RUB |

|

|

|

|

67.0 |

58.3 |

|

62.8 |

67.0 |

68.0 |

|

Kyzyl |

|

|

|

|

2,094 |

3.47 |

$/KZT |

|

|

|

|

342 |

326 |

|

345 |

363 |

353 |

|

Nezhda |

|

|

|

|

828 |

1.37 |

Gold breakeven price, $/oz |

|

|

748 |

861 |

|

861 |

780 |

762 |

|

Corporate and other |

|

|

|

|

-771 |

-1.28 |

||

Gold equivalent production volumes, koz |

|

|

|

|

|

|

|

|

Operating value |

|

|

|

|

6,556 |

10.85 |

|||

|

|

|

|

|

|

|

|

Financial instruments and rehab provision as at 31 December 2017 |

|

-101 |

-0.17 |

|||||||

Voro lumes |

|

|

|

129 |

120 |

|

101 |

80 |

80 |

|

Enterprise value |

|

|

|

|

6,455 |

10.69 |

|

Okhotsk operations |

lumes |

|

|

131 |

186 |

|

229 |

152 |

152 |

|

Net debt as at 31 December 2017 |

|

|

|

|

-1,420 |

-2.35 |

|

Dukat |

lumes |

|

|

|

369 |

322 |

|

310 |

304 |

304 |

|

Minority interest |

|

|

|

|

0 |

0.00 |

Omolon |

lumes |

|

|

|

170 |

202 |

|

182 |

195 |

195 |

|

Prognoz valued at 70% of acquisition price |

|

|

|

|

151 |

0.25 |

Varvara |

lumes |

|

|

|

85 |

130 |

|

143 |

157 |

157 |

|

Cash raised in rights issue during 2018E |

|

|

|

|

0 |

0.00 |

Amursk-Albazino |

lumes |

|

|

244 |

268 |

|

322 |

278 |

278 |

|

Equity value |

|

|

|

|

5,186 |

8.59 |

|

Armenia lumes |

|

|

|

26 |

50 |

|

54 |

8 |

0 |

|

|

|

|

|

|

|

|

|

|

|

|

Rounded to |

|

|

|

|

|

8.60 |

|||||||||

Mayskoye lumes |

|

|

|

116 |

124 |

|

136 |

135 |

135 |

|

Share price on 7/1/2019 |

|

|

|

|

|

8.66 |

|

Kyzyl lumes |

|

|

|

0 |

0 |

|

80 |

300 |

330 |

|

Expected share price return |

|

|

|

|

|

-0.7% |

|

Total volumes |

|

|

|

1,268 |

1,402 |

|

1,556 |

1,610 |

1,631 |

|

Plus: expected dividend yield |

|

|

|

|

|

6.7% |

|

Volume growth |

|

|

|

0% |

11% |

|

11% |

3% |

1% |

|

Total implied one-year return |

|

|

|

|

|

5.9% |

|

Contribution to FY18E adjusted EBITDA |

|

|

|

|

|

|

|

|

Share price range, GBP: |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

12-month high on 15-1-2018 |

9.45 12-month low on 10-4-2018 |

5.78 |

||||

|

|

|

Mayskoye |

Kyzyl |

Voro |

|

|

|

|

Price move since high |

-8.3% Price move since low |

|

49.9% |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Armenia |

6% |

|

2% |

10% |

|

|

|

|

Calculation of WACC |

|

|

|

|

|

|

||

|

|

2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Amursk-Albazino |

|

|

|

|

|

|

|

|

Okhotsk |

WACC |

8.2% |

Cost of debt |

|

|

5.0% |

|||

|

|

|

|

|

|

|

|

Risk-free rate |

4.0% |

Tax rate |

|

|

20% |

|||||

23% |

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

20% |

|

Equity risk premium |

6.0% After-tax cost of debt |

|

1.2% |

|||

|

|

|

|

|

|

|

|

|

|

|

|

Beta |

1.00 |

Debt weighting |

|

30% |

||

|

|

|

|

|

|

|

|

|

|

|

|

Cost of equity |

10.0% |

Terminal growth rate |

|

2.0% |

||

|

Varvara |

|

|

|

|

|

|

|

|

|

Valuation ratios |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dec-YE, $mn |

2016 |

2017 |

|

2018E |

2019E |

2020E |

||

|

9% |

|

|

|

|

|

|

|

Dukat |

|

|

|

||||||

|

|

Omolon |

|

|

|

|

|

|

P/E multiple |

12.5x |

13.6x |

|

10.3x |

7.5x |

7.4x |

|||

|

|

|

|

|

|

|

17% |

|

|

|

||||||||

|

|

|

11% |

|

|

|

|

|

|

|

|

Dividend yield |

3.7% |

3.7% |

|

4.9% |

6.7% |

6.8% |

|

|

|

|

|

|

|

|

|

|

|

|

EV/EBITDA |

8.1x |

8.8x |

|

7.6x |

5.8x |

5.7x |

|

|

|

|

|

|

|

|

|

|

|

|

P/B |

4.9x |

3.9x |

|

2.9x |

2.7x |

2.3x |

|

|

|

|

|

|

|

|

|

|

|

|

NAV per share, $ |

2.3 |

3.0 |

|

3.3 |

4.2 |

4.8 |

Source: Bloomberg, Thomson Reuters, Renaissance Capital estimates

71

vk.com/id446425943

PJSC Polyus – BUY

Renaissance Capital

14 January 2019

Metals & Mining

Figure 107: Polyus Gold, $mn (unless otherwise stated)

|

|

|

|

PJSC Polyus (MOEX) |

PLZL.MM |

Target price, RUB: |

6,300 |

Market capitalisation, $mn: |

10,279 |

Share price, RUB: |

5,287 |

Enterprise value, $mn: |

13,448 |

Potential 12-month return: |

25.5% |

Dec-YE |

|

|

2016 |

2017 |

2018E |

2019E |

2020E |

Income statement |

|

|

|

|

|

||

Revenue |

|

|

2,458 |

2,721 |

2,829 |

3,749 |

3,707 |

Adjusted EBITDA |

1,536 |

1,702 |

1,831 |

2,514 |

2,457 |

||

Adjusted EBIT |

1,363 |

1,485 |

1,507 |

2,188 |

2,123 |

||

Net interest |

|

410 |

76 |

-676 |

-194 |

-177 |

|

Taxation |

|

|

-326 |

-290 |

-101 |

-399 |

-389 |

Minority interest in profit |

-25 |

-1 |

-10 |

0 |

0 |

||

Net profit for the year |

1,420 |

1,240 |

756 |

1,592 |

1,556 |

||

Adjusted earnings |

952 |

1,015 |

1,298 |

1,595 |

1,556 |

||

Adjusted EPS, USc |

676 |

789 |

981 |

1,205 |

1,176 |

||

Consensus EPS, USc |

|

|

956 |

915 |

1,025 |

||

DPS declared, USc |

0 |

405 |

425 |

495 |

576 |

||

Consensus DPS, USc |

|

|

431 |

469 |

508 |

||

Adjusted EBITDA |

753 |

953 |

1,104 |

1,275 |

1,286 |

||

Olimpiada |

|

|

|||||

EBITDA margin |

63% |

66% |

71% |

73% |

72% |

||

Blagodatnoye |

|

417 |

414 |

365 |

440 |

459 |

|

EBITDA margin |

72% |

71% |

67% |

71% |

69% |

||

Verninskoye |

|

146 |

149 |

184 |

184 |

179 |

|

EBITDA margin |

62% |

57% |

63% |

65% |

64% |

||

Alluvials |

|

|

90 |

54 |

40 |

55 |

49 |

EBITDA margin |

40% |

28% |

24% |

31% |

29% |

||

Kuranakh |

|

|

107 |

109 |

117 |

139 |

134 |

EBITDA margin |

53% |

50% |

52% |

56% |

54% |

||

Natalka |

|

|

0 |

0 |

11 |

419 |

351 |

EBITDA margin |

- |

- |

33% |

62% |

61% |

||

Other |

|

|

-150 |

-194 |

-316 |

-325 |

-334 |

Adjusted EBITDA |

1,363 |

1,485 |

1,507 |

2,188 |

2,123 |

||

Income statement ratios |

|

|

|

|

|

||

EBITDA margin |

62% |

63% |

65% |

67% |

66% |

||

EBIT margin |

|

55% |

55% |

53% |

58% |

57% |

|

Adjusted EPS Growth |

38% |

17% |

24% |

23% |

-2% |

||

Dividend payout ratio |

0% |

51% |

43% |

41% |

49% |

||

Input assumptions |

|

|

|

|

|

||

Gold, $/oz |

|

|

1,248 |

1,258 |

1,269 |

1,350 |

1,338 |

$/RUB |

|

|

67.0 |

58.3 |

62.8 |

67.0 |

68.0 |

Gold breakeven price, $/oz |

715 |

830 |

909 |

931 |

1,021 |

||

Gold production volumes, koz |

|

|

|

|

|

||

Olimpiada lumes |

984 |

1,177 |

1,304 |

1,313 |

1,354 |

||

Blagodatnoye |

lumes |

457 |

457 |

415 |

462 |

493 |

|

Verninskoye lumes |

186 |

206 |

228 |

210 |

210 |

||

Alluvials |

lumes |

169 |

146 |

136 |

132 |

128 |

|

Kuranakh |

lumes |

160 |

171 |

178 |

185 |

185 |

|

Natalka |

lumes |

6 |

3 |

137 |

498 |

429 |

|

Sukhoi Log |

lumes |

0 |

0 |

0 |

0 |

0 |

|

Total volumes |

1,960 |

2,160 |

2,398 |

2,801 |

2,800 |

||

Volume growth |

11% |

10% |

11% |

17% |

0% |

||

Contribution to FY18E adjusted EBITDA

Alluvials |

Kuranakh |

NatalkaOther |

|

2% |

6% |

1% |

1% |

Verninskoye |

|

|

Olimpiada |

10% |

|

|

60% |

Blagodatnoye

20%

Dec-YE |

2016 |

2017 |

|

2018E |

2019E |

2020E |

Balance sheet |

|

|

|

|

|

|

Net operating assets |

3,254 |

4,406 |

|

4,538 |

4,847 |

5,089 |

Investments, net of rehab provision |

-427 |

-673 |

|

-767 |

-767 |

-767 |

Equity |

-508 |

564 |

|

403 |

1,340 |

2,135 |

Minority interest |

94 |

92 |

|

86 |

86 |

86 |

Net debt |

3,241 |

3,077 |

|

3,281 |

2,653 |

2,102 |

Balance sheet ratios |

|

|

|

|

|

|

Gearing (net debt/(net debt+equity)) |

118.6% |

84.5% |

|

89.1% |

66.4% |

49.6% |

Net debt to EBITDA |

2.1x |

1.8x |

|

1.8x |

1.1x |

0.9x |

RoCE |

47.1% |

37.5% |

|

32.8% |

45.8% |

42.0% |

RoIC (after tax) |

40.6% |

31.0% |

|

24.7% |

36.8% |

33.7% |

RoE |

129.7% |

3625.0% |

|

268.4% |

183.0% |

89.6% |

Cash flow statement |

|

|

|

|

|

|

Operating cash flow |

1,386 |

1,483 |

|

1,440 |

2,037 |

2,021 |

Capex (net of disposals) |

-466 |

-804 |

|

-814 |

-596 |

-565 |

Other cash flows |

-1,036 |

-245 |

|

192 |

-3 |

0 |

Free cash flow |

-116 |

434 |

|

818 |

1,439 |

1,456 |

Equity shareholders' cash |

714 |

738 |

|

371 |

1,283 |

1,314 |

Dividends and share buy-backs |

-3,591 |

-574 |

|

-575 |

-655 |

-762 |

Surplus (deficit) cash |

-2,877 |

164 |

|

-204 |

628 |

552 |

Cash flow ratios |

23 |

20 |

|

29 |

26 |

28 |

Working capital turnover, days |

|

|||||

FCF yield |

-1.0% |

3.3% |

|

6.0% |

11.0% |

11.6% |

Equity shareholders' yield |

8.7% |

7.3% |

|

3.6% |

12.4% |

12.7% |

Capex/EBITDA |

30.3% |

47.2% |

|

44.4% |

23.7% |

23.0% |

Cash conversion |

0.8x |

0.7x |

|

0.3x |

0.8x |

0.8x |

Valuation |

|

|

|

|

LSE |

MOEX |

|

|

|

|

|||

SoTP DCF fair value and calculation of target price |

$mn |

$/share |

RUB/sh |

|||

Olimpiada |

|

|

|

9,306 |

35.2 |

4,712 |

Blagodatnoye |

|

|

|

3,140 |

11.9 |

1,590 |

Verninskoye |

|

|

|

1,297 |

4.9 |

657 |

Alluvials |

|

|

|

110 |

0.4 |

56 |

Kuranakh |

|

|

|

868 |

3.3 |

439 |

Natalka |

|

|

|

2,985 |

11.3 |

1,511 |

Sukhoi Log |

|

|

|

-40 |

-0.2 |

-20 |

Other |

|

|

|

-1,282 |

-4.8 |

-649 |

Operating value |

|

|

|

16,384 |

61.9 |

8,295 |

Financial instruments and rehab provision as at 31 December 20 |

-673 |

-2.5 |

-341 |

|||

Enterprise value |

|

|

|

15,711 |

59.4 |

7,954 |

Net debt as at 31 December 2017 |

|

|

|

-3,077 |

-11.6 |

-1,558 |

Minority interest |

|

|

|

-92 |

-0.3 |

-47 |

Convertible debt cost at conversion price |

|

|

|

-58 |

-0.2 |

-29 |

Cash raised in rights issue during 2018E |

|

|

|

0 |

0.0 |

0 |

Equity value |

|

|

|

12,485 |

47.2 |

6,321 |

Rounded to |

|

|

|

|

47.0 |

6,300 |

Share price on 7/1/2019 |

|

|

|

|

38.0 |

5,287 |

Expected share price return |

|

|

|

|

23.7% |

19.2% |

Plus: expected dividend yield |

|

|

|

|

6.4% |

6.4% |

Total implied one-year return |

|

|

|

|

30.0% |

25.5% |

Share price range, RUB |

|

|

|

|

|

|

12-month high on 3-1-2019 |

5,468 12-month low on 9-4-2018 |

3,208 |

||||

Price move since high |

-3.3% |

Price move since low |

|

64.8% |

||

Calculation of WACC |

|

|

|

|

|

|

WACC |

8.7% |

Cost of debt |

|

|

7.0% |

|

Risk-free rate |

4.0% |

Tax rate |

|

|

20% |

|

Equity risk premium |

6.0% After-tax cost of debt |

|

1.7% |

|||

Beta |

1.00 |

Debt weighting |

|

30% |

||

Cost of equity |

10.0% |

Terminal growth rate |

|

2.0% |

||

Valuation ratios |

|

|

|

|

|

|

Dec-YE, $mn |

2016 |

2017 |

|

2018E |

2019E |

2020E |

P/E multiple |

9.4x |

9.7x |

|

8.0x |

6.5x |

6.6x |

Dividend yield |

0.0% |

5.3% |

|

5.4% |

6.3% |

7.4% |

EV/EBITDA |

7.5x |

7.8x |

|

7.5x |

5.2x |

5.1x |

P/B |

-16.2x |

17.9x |

|

25.7x |

7.7x |

4.8x |

NAV per share, $ |

-3.9 |

4.3 |

|

3.0 |

10.1 |

16.1 |

Source: Bloomberg, Thomson Reuters, Renaissance Capital estimates

72