- •Contents

- •Investment stance

- •Fears of an economic slowdown

- •Capital cycle favours rising returns

- •Management remains focused on value-creation

- •Comfortable balance sheets and supportive dividend potential

- •Value relative to other stocks

- •Positive earnings momentum

- •Commodity price revisions

- •Preference for base metals over steelmaking materials

- •Steel

- •Metallurgical coal

- •Iron ore

- •Manganese ore

- •Copper

- •Aluminium

- •Nickel

- •Zinc

- •Diamonds

- •Thermal coal

- •Platinum group metals (13mn oz)

- •Gold

- •Our long-term commodity prices should not incentivise over-supply

- •Earnings revisions

- •Risks and catalysts

- •Peer comp charts

- •Commodity price and exchange rate forecasts

- •Important publications

- •African Rainbow Minerals

- •Alrosa

- •Anglo American

- •Assore

- •Exxaro

- •Glencore

- •Kumba Iron Ore

- •Rio Tinto

- •Vale

- •Gold Fields

- •Harmony

- •Polymetal

- •Anglo American Platinum

- •Lonmin

- •Northam

- •Royal Bafokeng Platinum

- •Merafe Resources

- •Evraz

- •Severstal

- •Disclosures appendix

vk.com/id446425943

Evraz - BUY

Renaissance Capital

14 January 2019

Metals & Mining

Figure 116: Evraz, $mn (unless otherwise stated) |

|

|

|

Evraz |

EVRE.L / EVR LN |

Target price, GBp: |

620 |

Market capitalisation, GBPmn: |

6,834 |

Last price, GBp: |

475 |

Enterprise value, GBPmn: |

10,176 |

Potential 12-month return: |

45.4% |

Dec-YE |

2016 |

2017 |

2018E |

2019E |

2020E |

Income statement |

|

|

|

|

|

Revenue |

7,713 |

10,827 |

12,162 |

10,168 |

9,626 |

Underlying EBITDA |

1,542 |

2,624 |

3,896 |

2,943 |

2,529 |

Underlying EBIT |

1,021 |

2,063 |

3,310 |

2,303 |

1,847 |

Other items |

-629 |

-496 |

96 |

0 |

0 |

Equity accounted income |

-23 |

11 |

13 |

12 |

9 |

Net interest expense |

-461 |

-423 |

-367 |

-373 |

-373 |

Taxation |

-96 |

-396 |

-700 |

-388 |

-297 |

Profit after tax |

-188 |

759 |

2,353 |

1,553 |

1,187 |

Attributable profit |

-215 |

699 |

2,278 |

1,498 |

1,145 |

Basic EPS, USc |

-15 |

53 |

158 |

104 |

79 |

Thomson Reuters consensus EPS, USc |

|

|

146 |

113 |

97 |

DPS declared, USc |

0 |

60 |

109 |

92 |

50 |

Thomson Reuters consensus DPS, USc |

|

|

89 |

60 |

50 |

Underlying EBIT, $mn |

|

|

|

|

|

Coal - EBIT |

503 |

1,059 |

1,375 |

1,246 |

833 |

EBIT margin - Coal |

38% |

48% |

53% |

50% |

36% |

Russian & CIS steel - EBIT |

785 |

1,228 |

2,217 |

1,468 |

1,519 |

EBIT margin - Russian & CIS |

14% |

16% |

26% |

20% |

21% |

North American steel - EBIT |

-127 |

-74 |

-70 |

-133 |

-246 |

EBIT margin - North American steel |

-9% |

-4% |

-3% |

-7% |

-15% |

Other - EBIT |

-140 |

-150 |

-211 |

-279 |

-259 |

Total - EBIT |

1,021 |

2,063 |

3,310 |

2,303 |

1,847 |

EBIT margin |

13% |

19% |

27% |

23% |

19% |

Income statement ratios |

|

|

|

|

|

EBITDA margin |

20% |

24% |

32% |

29% |

26% |

EBIT margin |

13% |

19% |

27% |

23% |

19% |

EPS growth |

66% |

453% |

198% |

-34% |

-24% |

Dividend payout ratio |

0% |

113% |

69% |

88% |

63% |

Input assumptions (steel) |

|

|

|

|

|

Iron ore fines (62% Fe, CIF China), $/t |

58 |

71 |

66 |

62 |

62 |

Semi soft coking coal, $/t |

101 |

131 |

144 |

115 |

104 |

Hard coking coal, $/t |

144 |

188 |

206 |

178 |

160 |

Hot rolled coil - CIS, $/t |

382 |

502 |

552 |

468 |

471 |

RUB/$ |

67 |

58 |

62 |

67 |

68 |

Steel sales realisations, $/t |

517 |

698 |

814 |

676 |

644 |

EBITDA per tonne, $/t |

115 |

191 |

291 |

214 |

184 |

Capex/tonne, $ |

28 |

43 |

47 |

60 |

72 |

FCF/tonne, $ |

71 |

119 |

138 |

121 |

87 |

Sales volumes, kt |

|

|

|

|

|

Coal products |

9,867 |

10,499 |

10,982 |

12,447 |

14,900 |

Iron ore products |

4,222 |

2,937 |

2,026 |

2,024 |

2,024 |

Vanadium products |

20,428 |

22,319 |

18,609 |

19,650 |

19,788 |

Steel products |

|

|

|

|

|

Semi-finished products |

5,601 |

5,742 |

5,381 |

5,730 |

5,730 |

Construction products |

4,416 |

3,991 |

3,780 |

3,722 |

3,722 |

Railway products |

1,455 |

1,657 |

1,765 |

1,853 |

1,853 |

Flat-rolled products |

887 |

1,023 |

1,045 |

910 |

894 |

Tubular products |

534 |

749 |

838 |

968 |

968 |

Other |

571 |

602 |

594 |

557 |

557 |

Total |

13,464 |

13,764 |

13,404 |

13,739 |

13,723 |

Growth |

-7% |

2% |

-3% |

3% |

0% |

Contribution to FY18E underlying EBITDA |

|

|

|

|

|

|

|

|

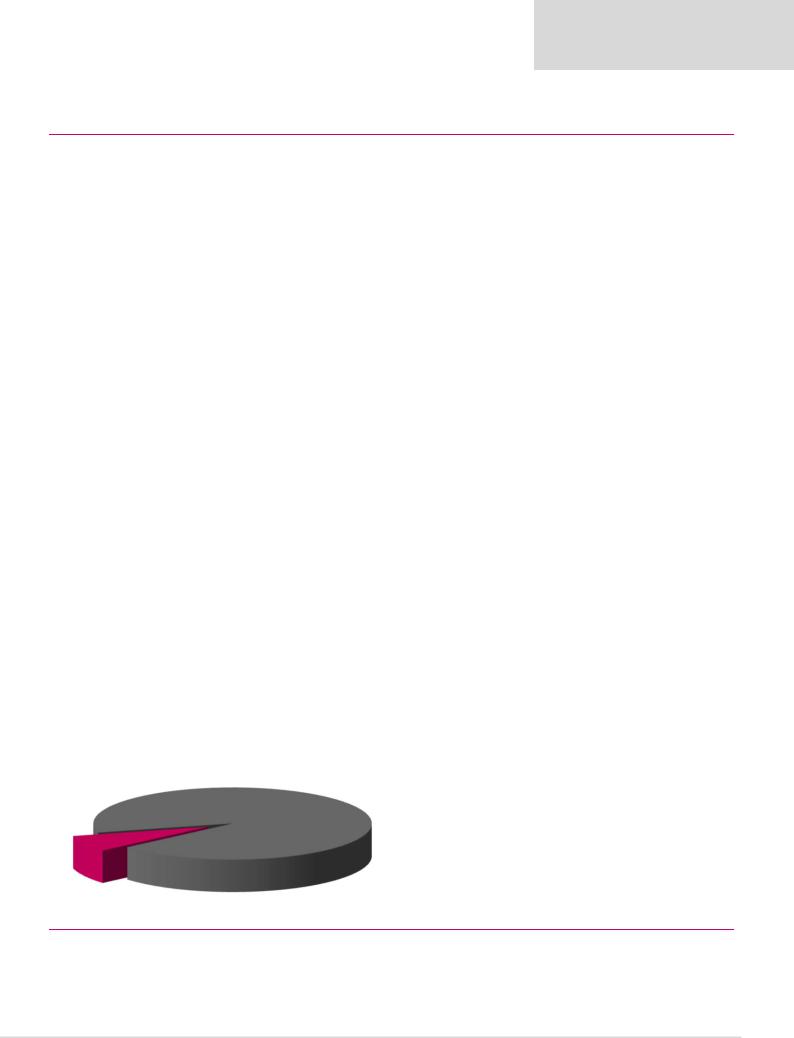

North American |

|

|

Russian & CIS |

|

|

|

steel |

|

steel |

|

|

|

2% |

|

60% |

|

|

|

|

|

Coal 38%

Dec-YE |

2016 |

2017 |

|

2018E |

2019E |

2020E |

|

Balance sheet |

|

|

|

|

|

|

|

Net operating assets |

5,521 |

6,054 |

|

6,476 |

6,674 |

6,973 |

|

Investments less provisions |

-107 |

-103 |

|

-130 |

-134 |

-141 |

|

Equity |

491 |

1,784 |

|

2,266 |

2,438 |

2,867 |

|

Minority interest BS |

186 |

242 |

|

282 |

309 |

330 |

|

Net debt (cash) |

4,737 |

3,925 |

|

3,798 |

3,793 |

3,634 |

|

Balance sheet ratios |

|

|

|

|

|

|

|

Gearing* |

91% |

69% |

|

63% |

61% |

56% |

|

Net debt to EBITDA |

3.07x |

1.50x |

|

0.97x |

1.29x |

1.44x |

|

RoCE |

18% |

35% |

|

51% |

34% |

26% |

|

RoIC (after tax) |

13% |

23% |

|

35% |

22% |

19% |

|

RoE |

-69% |

61% |

|

112% |

64% |

43% |

|

Cash flow statement |

|

|

|

|

|

|

|

Operating cash flow |

1,222 |

2,024 |

|

2,650 |

2,492 |

2,188 |

|

Capex |

-382 |

-595 |

|

-629 |

-829 |

-985 |

|

Other - CF |

111 |

214 |

|

-175 |

-6 |

-9 |

|

FCF |

951 |

1,643 |

|

1,845 |

1,657 |

1,193 |

|

Equity shareholders' cash |

582 |

1,305 |

|

1,531 |

1,331 |

874 |

|

Dividends and share buy backs |

-35 |

-469 |

|

-1,419 |

-1,326 |

-716 |

|

Advances (repayments) of debt |

-765 |

-527 |

|

-646 |

0 |

0 |

|

Increase (decrease) in cash |

-218 |

309 |

|

-534 |

6 |

158 |

|

Cash flow ratios |

|

|

|

|

|

|

|

Capex/EBITDA |

25% |

23% |

|

16% |

28% |

39% |

|

FCF yield |

12.5% |

18.7% |

|

14.9% |

12.9% |

9.4% |

|

Cash conversion ratio |

-2.7x |

1.9x |

|

0.7x |

0.9x |

0.8x |

|

Equity shareholders' yield |

21.8% |

28.2% |

|

18.5% |

15.2% |

10.0% |

|

Working capital days** |

7 |

11 |

|

27 |

26 |

26 |

|

Valuation |

|

|

|

|

|

|

|

Calculation of target price (TP) |

|

|

|

|

$mn |

GBp/share |

|

Coal |

|

|

|

|

7,271 |

380 |

|

Russian & CIS steel |

|

|

|

|

11,768 |

614 |

|

North American steel |

|

|

|

|

-554 |

-29 |

|

Other |

|

|

|

|

-2,399 |

-125 |

|

Enterprise value |

|

|

|

|

16,086 |

840 |

|

Investments less provisions |

|

|

|

|

-103 |

-5 |

|

Net debt as at 31 December 2017 |

|

|

|

|

-3,925 |

-205 |

|

Minority interest as at 31 December 2017 |

|

|

|

|

-242 |

-13 |

|

Equity value |

|

|

|

|

11,816 |

617 |

|

Plus: one-year forward equity shareholders' cash |

|

|

|

|

1 |

|

|

Less: dividends paid |

|

|

|

|

|

-1 |

|

Rounded to |

|

|

|

|

|

620 |

|

Share price on 7/1/2019 |

|

|

|

|

|

475 |

|

Expected share price return |

|

|

|

|

|

30.4% |

|

Plus: expected dividend yield |

|

|

|

|

|

15.0% |

|

Total implied one-year return |

|

|

|

|

|

45.4% |

|

Share price range, GBp: |

|

|

|

|

|

|

|

12-month high on 4-10-2018 |

590 |

12-month low on 9-2-2018 |

331 |

|

|||

Price move since high |

-19.4% |

Price move since low |

|

43.8% |

|

||

Calculation of discount rate |

|

|

|

|

|

|

|

WACC |

11.3% |

Cost of debt |

|

|

5.0% |

|

|

Risk-free rate |

4.0% |

Tax rate |

|

|

20% |

|

|

Equity risk premium |

7.0% |

After-tax cost of debt |

|

0.8% |

|

||

Beta |

1.30 |

Debt weighting |

|

20% |

|

||

Cost of equity |

13.1% |

Terminal growth rate |

|

3.0% |

|

||

Valuation ratios |

|

|

|

|

|

|

|

Dec-YE |

2016 |

2017 |

|

2018E |

2019E |

2020E |

|

P/E multiple |

-12.6x |

6.1x |

|

3.6x |

5.9x |

7.7x |

|

Dividend yield |

0.0% |

18.5% |

|

18.9% |

15.1% |

8.2% |

|

EV/EBITDA |

4.9x |

3.4x |

|

3.2x |

4.4x |

5.0x |

|

P/B |

5.4x |

2.6x |

|

3.7x |

3.6x |

3.1x |

|

NAV per share, $ |

0.35 |

1.25 |

|

1.58 |

1.69 |

1.99 |

|

*Gearing defined as net debt/(net debt +equity)

**Working capital days is defined as (working capital/revenue)*365

Source: Bloomberg, Thomson Reuters, Renaissance Capital estimates

81

vk.com/id446425943

MMK – BUY

Renaissance Capital

14 January 2019

Metals & Mining

Figure 117: MMK, $mn (unless otherwise stated)

|

|

|

|

Magnitogorsk Iron & Steel Works (MMK) |

MAGNq.L / MAGN.MM |

Target price, $: |

9.6 |

Market capitalisation, $mn: |

7,054 |

Last price, $: |

8.4 |

Enterprise value, $mn: |

7,058 |

Potential 12-month return: |

21.9% |

Dec-YE |

|

2016 |

2017 |

2018E |

2019E |

2020E |

Income statement |

|

|

|

|

|

|

Revenue |

|

5,630 |

7,546 |

8,041 |

6,946 |

7,194 |

Underlying EBITDA |

1,956 |

2,032 |

2,217 |

1,388 |

1,664 |

|

Underlying EBIT |

1,477 |

1,488 |

1,666 |

835 |

1,099 |

|

Other items |

|

-32 |

36 |

-73 |

0 |

0 |

Equity accounted income |

1 |

5 |

1 |

4 |

5 |

|

Net interest |

|

-104 |

-34 |

-15 |

-22 |

-32 |

Taxation |

|

-231 |

-306 |

-351 |

-182 |

-239 |

Profit after tax |

1,111 |

1,189 |

1,228 |

636 |

834 |

|

Basic EPS, $/GDR |

1.29 |

1.38 |

1.43 |

0.74 |

0.97 |

|

Thomson Reuters consensus EPS, $ |

|

|

1.61 |

1.28 |

1.19 |

|

DPS declared, $/GDR |

0.21 |

0.72 |

1.18 |

0.60 |

0.46 |

|

Thomson Reuters consensus DPS, $ |

|

|

1.25 |

1.10 |

1.00 |

|

Underlying EBIT, $mn |

|

|

|

|

|

|

Coal segment |

|

49 |

77 |

128 |

127 |

98 |

EBIT margin |

Coal segment |

25% |

24% |

36% |

38% |

33% |

Russian steel |

|

1,451 |

1,431 |

1,599 |

814 |

1,108 |

EBIT margin |

Russian steel |

27% |

20% |

21% |

12% |

16% |

Turkey steel |

EBIT |

-21 |

-11 |

-63 |

-101 |

-102 |

EBIT margin |

Turkey steel |

-4% |

-2% |

-11% |

-25% |

-24% |

Other - EBIT |

|

-2 |

-9 |

3 |

-4 |

-5 |

EBIT margin - Other |

0% |

1% |

-1% |

1% |

1% |

|

Total - EBIT |

|

1,477 |

1,488 |

1,666 |

835 |

1,099 |

EBIT margin |

|

26% |

20% |

21% |

12% |

15% |

Income statement ratios |

|

|

|

|

|

|

EBITDA margin |

35% |

27% |

28% |

20% |

23% |

|

EBIT margin |

|

26% |

20% |

21% |

12% |

15% |

EPS growth |

|

161% |

7% |

4% |

-48% |

31% |

Dividend payout ratio |

16% |

53% |

83% |

81% |

47% |

|

Input assumptions (steel) |

|

|

|

|

|

|

Iron ore fines (62% Fe, CIF China), $/t |

58 |

71 |

66 |

62 |

62 |

|

Hard coking coal, $/t |

144 |

188 |

206 |

178 |

160 |

|

Hot rolled coil - CIS, $/t |

382 |

502 |

552 |

468 |

471 |

|

RUB/$ |

|

67 |

58 |

63 |

67 |

68 |

$/EUR |

|

1.11 |

1.13 |

1.18 |

1.17 |

1.21 |

Steel sales realisations, $/t |

462 |

615 |

659 |

557 |

577 |

|

EBITDA per tonne, $/t |

161 |

166 |

182 |

111 |

133 |

|

Capex/tonne, $ |

-38 |

-54 |

-68 |

-68 |

-68 |

|

FCF/tonne, $ |

|

127 |

57 |

87 |

45 |

47 |

Sales volumes, kt |

|

|

|

|

|

|

Slabs and billets |

104 |

4 |

0 |

0 |

0 |

|

Long products |

|

1,730 |

1,787 |

1,828 |

1,893 |

1,893 |

Flat & plate products |

7,730 |

7,699 |

7,548 |

7,856 |

7,856 |

|

Downstream products |

2,616 |

2,770 |

2,819 |

2,718 |

2,718 |

|

Total sales |

|

12,180 |

12,260 |

12,195 |

12,467 |

12,467 |

Volume growth |

3% |

1% |

-1% |

2% |

0% |

|

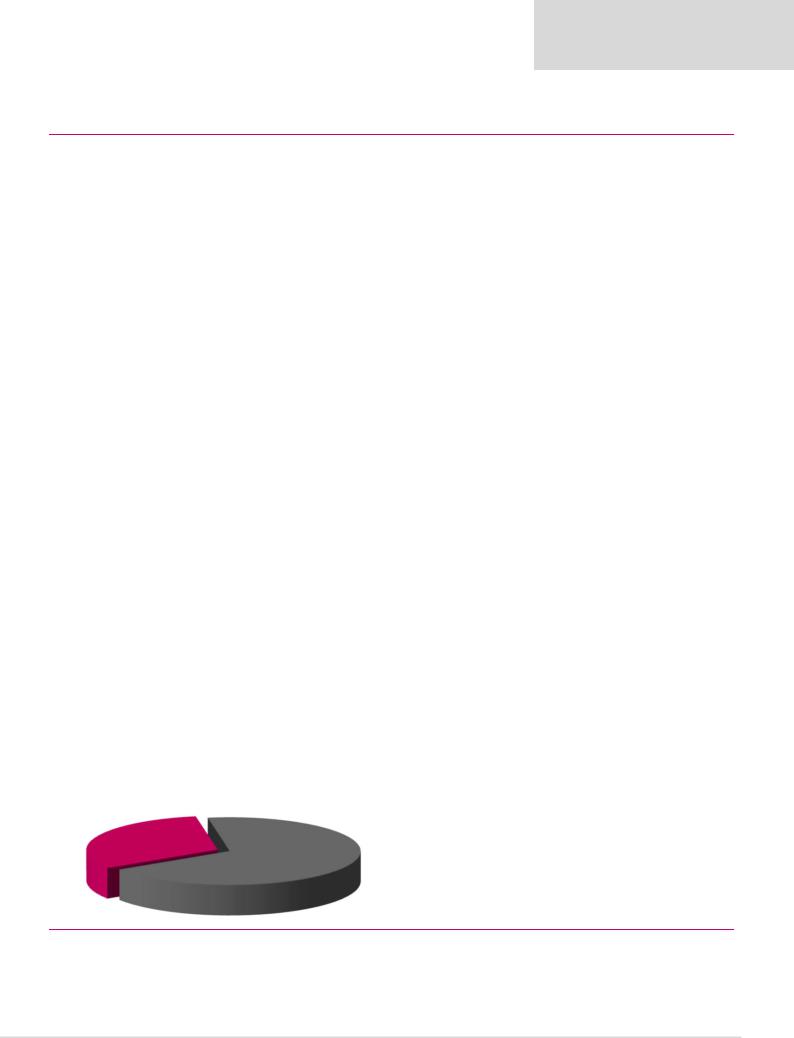

Contribution to FY18E underlying EBITDA

Russian steel 93%

Coal segment 7%

Dec-YE |

2016 |

2017 |

|

2018E |

2019E |

2020E |

Balance sheet |

|

|

|

|

|

|

Net operating assets |

5,356 |

6,188 |

|

5,695 |

5,838 |

6,167 |

Investments less provisions |

53 |

11 |

|

9 |

10 |

10 |

Equity |

4,694 |

5,691 |

|

5,520 |

5,190 |

5,717 |

Minority interest - BS |

18 |

27 |

|

23 |

26 |

30 |

Net debt (cash) |

234 |

-12 |

|

-279 |

160 |

-75 |

Balance sheet ratios |

|

|

|

|

|

|

Gearing* |

5% |

0% |

|

-5% |

3% |

-1% |

Net debt to EBITDA |

0.12x |

-0.01x |

|

-0.13x |

0.11x |

-0.05x |

RoCE |

30% |

26% |

|

28% |

14% |

18% |

RoIC (after tax) |

27% |

20% |

|

22% |

13% |

15% |

RoE |

28% |

23% |

|

22% |

12% |

15% |

Cash flow statement |

|

|

|

|

|

|

Operating cash flow |

1,644 |

1,439 |

|

2,047 |

1,396 |

1,422 |

Capex |

-463 |

-664 |

|

-830 |

-850 |

-850 |

Other - CF |

365 |

-82 |

|

-155 |

10 |

13 |

FCF |

1,546 |

693 |

|

1,062 |

556 |

585 |

Equity shareholders' cash |

1,424 |

652 |

|

1,043 |

530 |

546 |

Dividends and share buy backs |

-180 |

-406 |

|

-776 |

-969 |

-311 |

Advances (repayments) of debt |

-1,347 |

44 |

|

-203 |

353 |

0 |

Increase (decrease) in cash |

-103 |

290 |

|

64 |

-85 |

235 |

Cash flow ratios |

|

|

|

|

|

|

Capex/EBITDA |

24% |

33% |

|

37% |

61% |

51% |

FCF yield |

33% |

9% |

|

13% |

8% |

8% |

Cash conversion ratio |

1.3x |

0.6x |

|

0.8x |

0.8x |

0.7x |

Equity shareholders' yield |

32% |

9% |

|

13% |

7% |

8% |

Working capital days** |

59 |

57 |

|

46 |

48 |

48 |

Valuation |

|

|

|

|

|

|

Calculation of target price (TP) |

|

|

|

|

$mn |

$/GDR |

Coal segment |

|

|

|

|

694 |

0.8 |

Russian steel |

|

|

|

|

8,561 |

10.0 |

Turkey steel |

|

|

|

|

-483 |

-0.6 |

Other |

|

|

|

|

-500 |

-0.6 |

Enterprise value |

|

|

|

|

8,272 |

9.6 |

Investments |

|

|

|

|

11 |

0.0 |

Net cash (debt) as at 31 December 2017 |

|

|

|

|

12 |

0.0 |

Minority interest as at 31 December 2017 |

|

|

|

|

-27 |

0.0 |

Equity value |

|

|

|

|

8,268 |

9.6 |

Plus: one-year forward equity shareholders' cash |

|

|

|

|

0.6 |

|

Less: dividends paid |

|

|

|

|

|

-0.6 |

Rounded to |

|

|

|

|

|

9.6 |

Share price on 7-1-2019 |

|

|

|

|

|

8.4 |

Expected share price return |

|

|

|

|

|

14.7% |

Plus: expected dividend yield |

|

|

|

|

|

7.2% |

Total implied one-year return |

|

|

|

|

|

21.9% |

Share price range, $: |

|

|

|

|

|

|

12-month high on 27-2-2018 |

11.12 |

12-month low on 27-12-2018 |

7.75 |

|||

Price move since high |

-24.7% |

Price move since low |

|

8.0% |

||

Calculation of discount rate |

|

|

|

|

|

|

WACC |

11.3% |

Cost of debt |

|

|

4.0% |

|

Risk-free rate |

4.0% |

Tax rate |

|

|

20% |

|

Equity risk premium |

7.0% |

After-tax cost of debt |

|

11.3% |

||

Beta |

1.30 |

Debt weighting |

|

20% |

||

Cost of equity |

13.1% |

Terminal growth rate |

|

2.0% |

||

Valuation ratios |

|

|

|

|

|

|

Dec-YE, $mn |

2016 |

2017 |

|

2018E |

2019E |

2020E |

PE multiple |

4.0x |

6.2x |

|

6.7x |

11.3x |

8.6x |

Dividend yield |

4% |

9% |

|

12% |

7% |

5% |

EV/EBITDA |

2.4x |

3.6x |

|

3.6x |

5.3x |

4.3x |

P/B |

0.9x |

1.3x |

|

1.5x |

1.4x |

1.3x |

NAV per share, $ |

5.5 |

6.6 |

|

6.4 |

6.0 |

6.7 |

*Gearing defined as net debt/(net debt +equity)

**Working capital days is defined as (working capital/revenue)*365

Source: Bloomberg, Thomson Reuters, Renaissance Capital estimates

82

vk.com/id446425943

NLMK – BUY

Renaissance Capital

14 January 2019

Metals & Mining

Figure 118: NLMK, $mn (unless otherwise stated)

|

|

|

|

Novolipetsk Steel (NLMK) |

NLMKq.L / NLMK.MM |

Target price, $: |

26.4 |

Market capitalisation, $mn: |

13,583 |

Last price, $: |

22.9 |

Enterprise value, $mn: |

14,258 |

Potential 12-month return: |

27.9% |

Dec-YE |

|

2016 |

2017 |

2018E |

2019E |

2020E |

Income statement |

|

|

|

|

|

|

Revenue |

|

7,636 |

10,065 |

11,876 |

10,260 |

10,175 |

Underlying EBITDA |

1,941 |

2,655 |

3,463 |

2,672 |

2,672 |

|

Underlying EBIT |

1,485 |

2,031 |

2,876 |

2,082 |

2,074 |

|

Other items |

|

-185 |

-60 |

-57 |

0 |

0 |

Equity accounted income |

-61 |

-90 |

-65 |

-52 |

-58 |

|

Net interest |

|

-66 |

-58 |

-53 |

-63 |

-67 |

Taxation |

|

-233 |

-371 |

-519 |

-404 |

-401 |

Minority interest |

4 |

2 |

-4 |

1 |

1 |

|

Attributable profit |

943 |

1,454 |

2,177 |

1,563 |

1,549 |

|

Underlying earnings |

1,089 |

1,455 |

2,156 |

1,563 |

1,549 |

|

Underlying EPS, $/GDR |

1.82 |

2.43 |

3.60 |

2.61 |

2.58 |

|

Thomson Reuters consensus EPS, $ |

|

|

3.74 |

2.82 |

2.64 |

|

DPS declared, $/GDR |

1.53 |

2.38 |

3.30 |

2.82 |

2.61 |

|

Thomson Reuters consensus DPS, $ |

|

|

3.40 |

2.72 |

2.45 |

|

Underlying EBIT, $mn |

|

|

|

|

|

|

Mining - EBIT |

|

275 |

524 |

848 |

695 |

680 |

EBIT margin |

g |

46% |

56% |

67% |

62% |

61% |

Flat - EBIT |

|

1,051 |

1,357 |

1,744 |

1,215 |

1,345 |

EBIT margin |

|

19% |

18% |

21% |

18% |

19% |

Long |

|

91 |

77 |

202 |

65 |

54 |

EBIT margin |

g |

7% |

4% |

9% |

3% |

3% |

NLMK USA |

|

117 |

139 |

234 |

183 |

70 |

EBIT margin |

SA |

10% |

8% |

11% |

10% |

4% |

Dansteel |

|

-7 |

-6 |

-20 |

-13 |

-13 |

EBIT margin |

l |

-2% |

-1% |

-4% |

-3% |

-3% |

Other |

|

-42 |

-60 |

-132 |

-63 |

-63 |

EBIT margin |

Other |

2% |

2% |

3% |

2% |

2% |

Total |

|

1,485 |

2,031 |

2,876 |

2,082 |

2,074 |

EBIT margin |

|

19% |

20% |

24% |

20% |

20% |

Income statement ratios |

|

|

|

|

|

|

EBITDA margin |

25% |

26% |

29% |

26% |

26% |

|

EBIT margin |

|

19% |

20% |

24% |

20% |

20% |

EPS growth |

|

-3% |

54% |

50% |

-28% |

-1% |

Dividend payout ratio |

97% |

98% |

91% |

108% |

101% |

|

Input assumptions (steel) |

|

|

|

|

|

|

Iron ore fines (62% Fe, CIF China), $/t |

58 |

71 |

66 |

62 |

62 |

|

Hard coking coal, $/t |

144 |

188 |

206 |

178 |

160 |

|

Hot rolled coil - CIS, $/t |

382 |

502 |

552 |

468 |

471 |

|

Cold rolled coil - CIS, $/t |

434 |

559 |

615 |

573 |

579 |

|

RUB/$ |

|

67 |

58 |

63 |

67 |

68 |

$/EUR |

|

1.11 |

1.13 |

1.18 |

1.17 |

1.21 |

Steel sales realisations, $/t |

479 |

610 |

689 |

592 |

587 |

|

EBITDA per tonne, $/t |

122 |

161 |

201 |

154 |

154 |

|

Capex/tonne, $ |

35 |

37 |

38 |

40 |

40 |

|

FCF/tonne, $ |

|

65 |

71 |

104 |

105 |

91 |

Utilisation rate |

|

91% |

94% |

97% |

97% |

97% |

Sales volumes, kt |

|

|

|

|

|

|

Pig iron |

|

365 |

429 |

762 |

645 |

645 |

Slab |

|

2,697 |

2,605 |

2,428 |

2,198 |

2,198 |

Billets |

|

612 |

686 |

786 |

807 |

807 |

Flat |

|

10,065 |

10,501 |

10,676 |

10,679 |

10,679 |

Long |

|

2,196 |

2,277 |

2,573 |

3,005 |

3,005 |

Total sales |

|

15,935 |

16,498 |

17,225 |

17,334 |

17,334 |

Contribution to FY18E underlying EBITDA

Flat |

Long |

|

58% |

||

7% |

||

|

||

|

USA |

|

|

8% |

|

|

Mining |

|

|

27% |

Dec-YE |

2016 |

2017 |

|

2018E |

2019E |

2020E |

Balance sheet |

|

|

|

|

|

|

Net operating assets |

7,177 |

7,858 |

|

7,431 |

7,217 |

7,229 |

Investments |

255 |

248 |

|

284 |

290 |

295 |

Equity |

6,653 |

7,166 |

|

6,559 |

6,427 |

6,413 |

Minority interest - BS |

18 |

17 |

|

15 |

13 |

12 |

Net debt (cash) |

761 |

923 |

|

1,142 |

1,067 |

1,099 |

Balance sheet ratios |

|

|

|

|

|

|

Gearing* |

10% |

11% |

|

15% |

14% |

15% |

Net debt to EBITDA |

0.39x |

0.35x |

|

0.33x |

0.40x |

0.41x |

RoCE |

21% |

26% |

|

36% |

27% |

28% |

RoIC (after tax) |

19% |

23% |

|

30% |

23% |

24% |

RoE |

14% |

20% |

|

33% |

24% |

24% |

Cash flow statement |

|

|

|

|

|

|

Operating cash flow |

1,674 |

1,860 |

|

2,659 |

2,527 |

2,290 |

Capex |

-559 |

-603 |

|

-650 |

-700 |

-700 |

Other - CF |

-86 |

-87 |

|

-218 |

-6 |

-5 |

FCF |

1,030 |

1,170 |

|

1,791 |

1,821 |

1,584 |

Equity shareholders' cash |

979 |

1,122 |

|

1,746 |

1,770 |

1,531 |

Dividends and share buy backs |

-579 |

-1,284 |

|

-1,965 |

-1,695 |

-1,563 |

Advances (repayments) of debt |

-407 |

12 |

|

-462 |

573 |

6 |

Increase (decrease) in cash |

-7 |

-150 |

|

-681 |

648 |

-27 |

Cash flow ratios |

|

|

|

|

|

|

Capex/EBITDA |

29% |

23% |

|

19% |

26% |

26% |

FCF yield |

11.8% |

8.7% |

|

11.0% |

12.3% |

10.7% |

Cash conversion ratio |

1.0x |

0.8x |

|

0.8x |

1.1x |

1.0x |

Equity shareholders' yield |

12.3% |

9.0% |

|

11.6% |

12.9% |

11.2% |

Working capital days** |

77 |

75 |

|

70 |

71 |

71 |

Valuation |

|

|

|

|

|

|

Calculation of target price (TP) |

|

|

|

|

$mn |

$/share |

Mining |

|

|

|

|

5,882 |

9.8 |

Flat |

|

|

|

|

9,943 |

16.6 |

Long |

|

|

|

|

922 |

1.5 |

USA |

|

|

|

|

992 |

1.7 |

Dansteel |

|

|

|

|

-165 |

-0.3 |

Other |

|

|

|

|

-1,123 |

-1.9 |

Enterprise value |

|

|

|

|

16,452 |

27.5 |

Financial instruments as at 31 December 2017 |

|

|

|

248 |

0.4 |

|

Net debt as at 31 December 2017 |

|

|

|

|

-923 |

-1.5 |

Equity value |

|

|

|

|

15,777 |

26.3 |

Plus: one-year forward equity shareholders' cash |

|

|

|

|

2.9 |

|

Less: dividends paid |

|

|

|

|

|

-2.8 |

Rounded to |

|

|

|

|

|

26.4 |

Share price on 7/1/2019 |

|

|

|

|

|

22.85 |

Expected share price return |

|

|

|

|

|

15.5% |

Plus: expected dividend yield |

|

|

|

|

|

12.3% |

Total implied one-year return |

|

|

|

|

|

27.9% |

Share price range, $ |

|

|

|

|

|

|

12-month high on 6-6-2018 |

28.03 |

12-month low on 17-3-2017 |

21.73 |

|||

Price move since high |

-18.5% |

Price move since low |

|

5.2% |

||

Calculation of discount rate |

|

|

|

|

|

|

WACC |

11.3% |

Cost of debt |

|

|

4.0% |

|

Risk-free rate |

4.0% |

Tax rate |

|

|

20% |

|

Equity risk premium |

7.0% |

After-tax cost of debt |

|

0.8% |

||

Beta |

1.30 |

Debt weighting |

|

20% |

||

Cost of equity |

13.1% |

Terminal growth rate |

|

2.0% |

||

Valuation ratios |

|

|

|

|

|

|

Dec-YE |

2016 |

2017 |

|

2018E |

2019E |

2020E |

P/E multiple |

7.3x |

8.6x |

|

7.0x |

8.8x |

8.8x |

Dividend yield |

11.6% |

11.5% |

|

13.1% |

12.4% |

11.4% |

EV/EBITDA |

4.5x |

5.0x |

|

4.7x |

5.5x |

5.5x |

P/B |

1.2x |

1.7x |

|

2.3x |

2.1x |

2.1x |

NAV per share, $ |

1.11 |

1.20 |

|

1.09 |

1.07 |

1.07 |

*Gearing defined as net debt/(net debt +equity)

**Working capital days is defined as (working capital/revenue)*365

Source: Bloomberg, Thomson Reuters, Renaissance Capital estimates

83

vk.com/id446425943

Severstal - BUY

Renaissance Capital

14 January 2019

Metals & Mining

Figure 119: Severstal, $mn (unless otherwise stated)

|

|

|

|

Severstal |

SVSTq.L / CHMF.MM |

Target price, $: |

17.1 |

Market capitalisation, $mn: |

11,582 |

Last price, $: |

14.3 |

Enterprise value, $mn: |

12,430 |

Potential 12-month return: |

31.4% |

Dec-YE |

2016 |

2017 |

2018E |

2019E |

2020E |

Income statement |

|

|

|

|

|

Revenue |

5,916 |

7,848 |

8,427 |

7,388 |

7,563 |

Underlying EBITDA |

1,911 |

2,577 |

2,985 |

2,290 |

2,384 |

Underlying EBIT |

1,569 |

2,174 |

2,588 |

1,898 |

1,978 |

Other items |

294 |

-266 |

-137 |

0 |

0 |

Equity accounted income |

14 |

10 |

12 |

6 |

6 |

Net interest |

-160 |

-154 |

-108 |

-109 |

-166 |

Taxation |

-97 |

-409 |

-458 |

-359 |

-364 |

Minority interest |

1 |

1 |

0 |

0 |

0 |

To owners of the parent |

1,621 |

1,356 |

1,897 |

1,436 |

1,454 |

Underlying earnings |

1,268 |

1,547 |

1,976 |

1,436 |

1,454 |

Underlying EPS, USc |

156 |

191 |

242 |

175 |

178 |

Thomson Reuters consensus EPS, USc |

|

|

250 |

206 |

186 |

DPS declared, USc |

124 |

187 |

255 |

169 |

178 |

Thomson Reuters consensus DPS, USc |

|

|

208 |

167 |

146 |

Underlying EBIT, $mn |

|

|

|

|

|

Resources - EBIT |

282 |

678 |

821 |

718 |

698 |

EBIT margin - resources |

24% |

39% |

44% |

41% |

40% |

Russian steel - EBIT |

1,315 |

1,493 |

1,817 |

1,200 |

1,299 |

EBIT margin - Russian steel |

24% |

21% |

24% |

18% |

19% |

Other - EBIT |

-28 |

3 |

-50 |

-20 |

-20 |

Underlying EBIT |

1,569 |

2,174 |

2,588 |

1,898 |

1,978 |

EBIT margin |

27% |

28% |

31% |

26% |

26% |

Income statement ratios |

|

|

|

|

|

EBITDA margin |

32% |

33% |

35% |

31% |

32% |

EBIT margin |

27% |

28% |

31% |

26% |

26% |

EPS growth |

167% |

-17% |

39% |

-24% |

1% |

Dividend payout ratio |

79% |

98% |

105% |

96% |

100% |

Input assumptions |

58 |

71 |

66 |

62 |

62 |

Iron ore fines (62% Fe, CIF China), $/t |

|||||

Hard coking coal, $/t |

144 |

188 |

206 |

178 |

160 |

Hot rolled coil - CIS, $/t |

382 |

502 |

552 |

468 |

471 |

Cold rolled coil - CIS, $/t |

434 |

559 |

615 |

573 |

579 |

RUB/$ |

67 |

58 |

63 |

67 |

68 |

Steel sales realisations, $/t |

506 |

655 |

684 |

597 |

607 |

EBITDA per tonne, $/t |

178 |

235 |

266 |

205 |

214 |

Capex/tonne, $ |

51.3 |

53.9 |

68.1 |

125.4 |

89.5 |

FCF/tonne, $ |

1.2 |

1.8 |

2.4 |

0.9 |

1.3 |

Utilisation rate |

86% |

87% |

90% |

90% |

90% |

Sales volumes, kt |

|

|

|

|

|

Coking coal |

827 |

200 |

308 |

152 |

495 |

Steam coal |

2,030 |

1,583 |

1,209 |

1,088 |

1,088 |

Total coal |

2,857 |

1,783 |

1,517 |

1,240 |

1,583 |

Iron ore pellets |

6,028 |

6,514 |

6,363 |

6,914 |

7,115 |

Iron ore concentrate |

120 |

131 |

768 |

723 |

1,213 |

Total iron ore |

6,149 |

6,645 |

7,131 |

7,636 |

8,328 |

Semi-finished products |

724 |

519 |

679 |

566 |

566 |

Rolled products |

8,120 |

8,579 |

8,733 |

8,681 |

8,681 |

Downstream products |

1,871 |

1,862 |

1,818 |

1,921 |

1,921 |

Total steel sales |

10,715 |

10,959 |

11,230 |

11,167 |

11,167 |

Contribution to FY18E underlying EBITDA

Resources |

Russian steel |

31% |

69% |

Dec-YE |

2016 |

2017 |

|

2018E |

2019E |

2020E |

Balance sheet |

|

|

|

|

|

|

Net operating assets |

3,656 |

4,237 |

|

4,003 |

4,815 |

5,346 |

Investments |

250 |

229 |

|

28 |

35 |

40 |

Equity |

3,032 |

3,389 |

|

3,399 |

3,308 |

3,355 |

Minority interest - BS |

15 |

15 |

|

14 |

14 |

14 |

Net debt (cash) |

859 |

1,062 |

|

618 |

1,529 |

2,017 |

Balance sheet ratios |

|

|

|

|

|

|

Gearing* |

22% |

24% |

|

15% |

32% |

38% |

Net debt to EBITDA |

0.45x |

0.41x |

|

0.21x |

0.67x |

0.85x |

RoCE |

46% |

53% |

|

59% |

40% |

36% |

RoIC (after tax) |

28% |

33% |

|

40% |

27% |

24% |

RoE |

48% |

48% |

|

58% |

43% |

44% |

Cash flow statement |

|

|

|

|

|

|

Operating cash flow |

1,578 |

2,107 |

|

2,689 |

2,028 |

2,007 |

Capex |

-550 |

-591 |

|

-765 |

-1,400 |

-1,000 |

Other - CF |

-89 |

-82 |

|

22 |

75 |

44 |

FCF |

939 |

1,434 |

|

1,946 |

703 |

1,051 |

Equity shareholders' cash |

864 |

1,347 |

|

1,870 |

616 |

919 |

Dividends and share buy backs |

-918 |

-1,550 |

|

-1,426 |

-1,527 |

-1,407 |

Advances (repayments) of debt |

-439 |

80 |

|

-325 |

584 |

565 |

Increase (decrease) in cash |

-493 |

-123 |

|

120 |

-327 |

77 |

Cash flow ratios |

|

|

|

|

|

|

Capex/EBITDA |

29% |

23% |

|

26% |

61% |

42% |

Cash conversion ratio |

0.5x |

1.0x |

|

1.0x |

0.4x |

0.6x |

FCF yield |

9.3% |

11.2% |

|

14.5% |

5.3% |

7.7% |

Equity shareholders' yield |

9.4% |

11.4% |

|

14.7% |

5.3% |

7.8% |

Working capital days** |

48 |

46 |

|

38 |

41 |

42 |

Valuation |

|

|

|

|

|

|

Calculation of target price (TP) |

|

|

|

|

$mn |

$/GDR |

Resources |

|

|

|

|

4,911 |

6.0 |

Russian steel |

|

|

|

|

10,652 |

13.0 |

Other |

|

|

|

|

85 |

0.1 |

Enterprise value |

|

|

|

|

15,648 |

19.1 |

Financial instruments as at 31 December 2017 |

|

|

|

229 |

0.3 |

|

Net debt as at 31 December 2017 |

|

|

|

|

-1,062 |

-1.3 |

Minority interest |

|

|

|

|

-15 |

0.0 |

Equity value |

|

|

|

|

14,800 |

18.1 |

Plus: one-year forward equity shareholders' cash |

|

|

|

|

0.8 |

|

Less: dividends paid |

|

|

|

|

|

-1.7 |

Rounded to |

|

|

|

|

|

17.1 |

Share price on 7/1/2019 |

|

|

|

|

|

14.3 |

Expected share price return |

|

|

|

|

|

19.6% |

Plus: expected dividend yield |

|

|

|

|

|

11.8% |

Total implied one-year return |

|

|

|

|

|

31.4% |

Share price range, $ |

|

|

|

|

|

|

12-month high on 15-1-2018 |

27.93 |

12-month low on 17-3-2017 |

17.17 |

|||

Price move since high |

-8.4% |

Price move since low |

|

49.0% |

||

Calculation of discount rate |

|

|

|

|

|

|

WACC |

11.3% |

Cost of debt |

|

|

5.0% |

|

Risk-free rate |

4.0% |

Tax rate |

|

|

20% |

|

Equity risk premium |

7.0% |

After-tax cost of debt |

|

4.0% |

||

Beta |

1.30 |

Debt weighting |

|

20% |

||

Cost of equity |

13.1% |

Terminal growth rate |

|

3.0% |

||

Valuation ratios |

|

|

|

|

|

|

Dec-YE, $mn |

2016 |

2017 |

|

2018E |

2019E |

2020E |

P/E multiple |

7.3x |

7.6x |

|

6.4x |

8.2x |

8.0x |

Dividend yield |

10.8% |

12.9% |

|

16.3% |

11.8% |

12.4% |

EV/EBITDA |

5.3x |

5.0x |

|

4.5x |

5.8x |

5.8x |

P/B |

3.0x |

3.5x |

|

3.8x |

3.5x |

3.5x |

NAV per share, $ |

3.74 |

4.18 |

|

4.15 |

4.04 |

4.10 |

*Gearing defined as net debt/(net debt +equity)

**Working capital days is defined as (working capital/revenue)*365

Source: Bloomberg, Thomson Reuters, Renaissance Capital estimates

84