10.3. INFINITESIMAL MARGINAL INTERVENTION |

317 |

0.03 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

s |

|

|

|

|

0.02 |

|

|

|

|

|

|

|

|

|

|

0.01 |

|

|

|

|

|

|

|

|

|

|

0 |

|

|

|

|

|

|

|

|

|

f |

-0.03 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.00 |

0.01 |

0.01 |

0.02 |

0.02 |

0.03 |

-0.01 |

G(f) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

-0.02 |

|

|

|

|

|

|

|

|

|

|

|

s=f |

|

|

|

|

|

|

|

|

|

-0.03 |

|

|

|

|

|

|

|

|

|

|

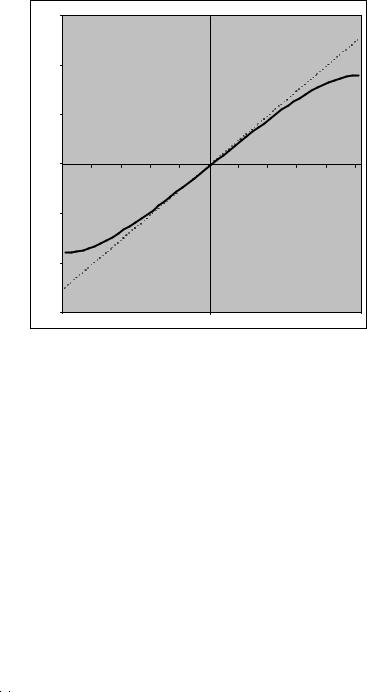

Figure 10.1: Relation between exchange rate and fundamentals under pure ßoat and Krugman interventions

Estimating and Testing the Krugman Model

DeJong [36] estimates the Krugman model by maximum likelihood and by simulated method of moments (SMM) using weekly data from January 1987 to September 1990. He ends his sample in 1990 so that exchange rates a ected by news or expectations about German reuniÞcation, which culminated in the European Monetary System crisis of September 1992, are not included.

We will follow De Jong’s SMM estimation strategy to estimate the basic Krugman model

∆ft |

= |

η + σut, |

Gt |

= αη + ft + Aeλ1ft + Beλ2ft , |

|

¯ iid

where f = −f, the time unit is one day (∆t = 1), and ut N(0, 1). λ1

and λ2 are given in (10.34)-(10.35), and A and B are given in (10.38)