322 CHAPTER 10. TARGET-ZONE MODELS

the event that it loses a dollar on a particular intervention.8 In the Þrst round, the probability that f hits f¯ is 12 . That is, P(Gc) = 12 . By implication, P(G) = 1 − P(Gc) = 12 . It follows that before the Þrst round starts, the probability that reserves eventually get driven to zero

is |

1 |

|

1 |

|

|

|

|

|

|||

Pr(L) = |

|

Pr(L|G) + |

|

Pr(L|Gc). |

(10.47) |

2 |

2 |

||||

(10.47) true before the Þrst round and is true for any round as long as the authorities still have at least one dollar in reserves.

Let pj be the conditional probability that reserves eventually become 0 given that the current level of reserves is j-dollars. For any j ≥ 1,

(10.47) can be expressed as the di erence equation |

|

|||||||||

p |

= |

1 |

p |

|

+ |

1 |

p |

|

, |

(10.48) |

2 |

|

|

j−1 |

|||||||

j |

|

|

j+1 |

|

2 |

|

|

|||

with p0 = 1.9 Backward substitution gives p2 = 2p1 − 1, p3 = 3p1 − 2, pk = kp1 − (k − 1), . . ., or equivalently, for k ≥ 2,

pk = 1 − k(1 − p1). |

(10.49) |

Since pk is a probability, it cannot exceed 1. Upon rearrangement you get

|

pk |

1 |

|

|

|

p1 = 1 + |

|

− |

|

→ 1, as k → ∞. |

(10.50) |

k |

k |

||||

but if p1 = 1, the recursion in (10.49) says that for any j ≥ 1, pj = 1. Translation? It is a sure thing that any Þnite amount of reserves will eventually be exhausted.

10.6Imperfect Target-Zone Credibility

The discrete intervention rule is more realistic than the inÞnitesimal marginal intervention rule. But if reserves run out with probability 1,

8G is the event that f hits f, and Gc is the event that f hits f¯.

9Clearly, p0 = 1 since if j = 0, reserves have been exhausted. If j = 1, there is a probability of 12 that reserves are exhausted on the next intervention and a probability of 12 that the central bank gains a dollar and survives to play again at which time there will be a probability of p2 that reserves will eventually be exhausted. That is, for j = 1, p1 = 12 p0 + 12 p2. Continuing on in this way, you get (10.48).

10.6. IMPERFECT TARGET-ZONE CREDIBILITY |

323 |

there will come a time in any target-zone arrangement when it is no |

|

longer worthwhile for the authorities to continue to defend the zone. |

|

This means that the target-zone bands cannot always be completely |

|

credible. In fact, during the twelve years or so that the Exchange Rate |

|

Mechanism of the European Monetary System operated reasonably well |

|

(1979—1992), there were eleven realignments of the bands. It would be |

|

strange to think that a zone would be completely credible given that |

|

there is already a history of realignments. |

|

We now modify the target-zone analysis to allow for imperfect cred- |

|

ibility along the lines of Bertola and Caballero [8]. Let the bands for the |

|

fundamentals be [f, f¯] and let β = f¯− f be the width of the band. If |

|

the fundamentals reach the lower band, there is a probability p that the |

|

authorities re-align and a probability 1 − p that the authorities defend |

|

the zone. |

|

If re-alignment occurs, what used to be the lower band of the old |

|

zone f, becomes the upper band of the new zone [f −β, f]. The realign- |

|

ment is a discrete intervention that sets f = f − β/2 at the midpoint |

|

of the new band. If a defense is mounted, the fundamentals are re- |

|

turned to the midpoint, f = f + β/2. An analogous set of possibilities |

|

describe the intervention choices if the fundamentals reach the upper |

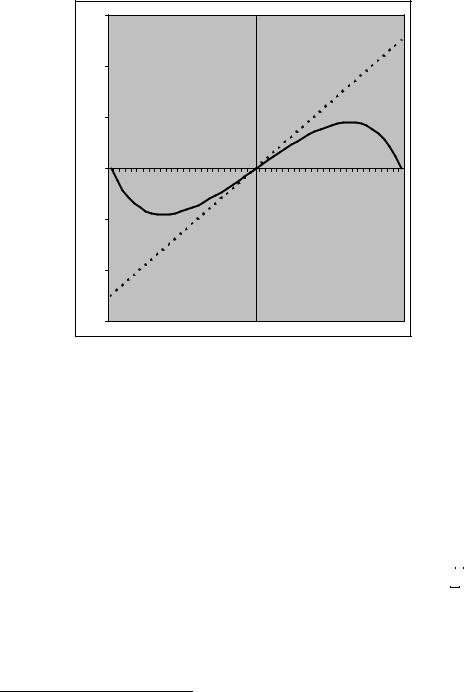

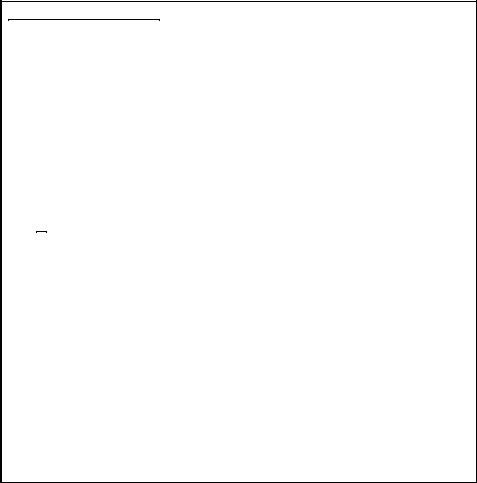

(217) |

band. Figure 10.3 illustrates the intervention possibilities. |

Realign |

Defend |

f |

- b |

f |

- b/2 |

f |

|

f |

+ b/2 |

f |

+ b |

|

|

|

Figure 10.3: Bertola-Caballero realignment and defense possibilities.

We begin with the symmetric exchange rate solution (10.44) with η = 0 and an initial symmetric target zone about 0 where f = −f¯,

10.6. IMPERFECT TARGET-ZONE CREDIBILITY |

325 |

Target-zone Summary

1.The theory covered in this chapter was based on the monetary model where today’s exchange rate depends in part on market participant’s expectations of the future exchange rate. Under a target zone, these expectations depend on the position of the exchange rate within the zone. As the exchange rate moves farther away from the central parity, intervention that manipulates the exchange rate becomes increasingly likely and the expectation

of this intervention feeds back into the current value of s(t).

2. When the fundamentals follows a di usion process for f < f < f¯and the target zone is perfectly credible, the exchange rate exhibits mean reversion within the zone. The exchange rate is less responsive to a given change in the fundamentals under a target zone than under a free ßoat. The target zone can be said to have a volatility reducing e ect on the exchange rate.

3.Any target zone–and therefore any Þxed exchange rate regime–operating under a discrete intervention rule will eventually break down because the central bank will ultimately exhaust its foreign exchange reserves. But if the target zone must ultimately collapse, it cannot always be fully credible.

4.When the target zone lacks su cient credibility, the zone itself can be a source of exchange rate volatility in the sense that the exchange rate is even more sensitive to a given change in the fundamentals than it would be under a free ßoat.

326 |

CHAPTER 10. TARGET-ZONE MODELS |